PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073297

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073297

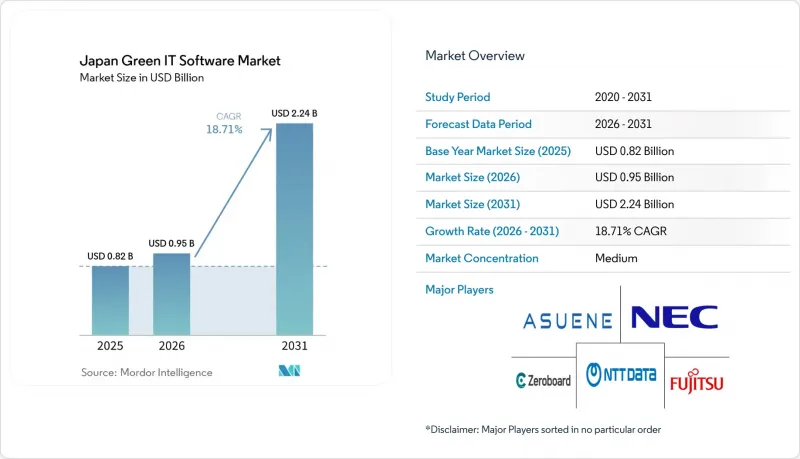

Japan Green IT Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the japan green IT software market size was valued at USD 0.82 billion in 2025 and is projected to reach USD 2.24 billion by 2031, growing at a CAGR of 18.71% from 2026 to 2031.

This report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, On-Premise, and Hybrid), Solution Type (Carbon Management and Accounting Software, and More), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Information Technology and Telecommunications, Manufacturing, and More). The Market Forecasts are Provided in Terms of Value (USD).

Japan Green IT Software Market Trends and Insights

Tighter Gx Disclosure and Audit Expectations

Tighter disclosure and audit expectations are giving the Japan green IT software market a more compliance-led buying pattern, especially among larger listed companies and major industrial groups. Buyers are no longer looking only for dashboards or emissions visibility, they are looking for systems that can support repeatable documentation, internal controls, and third-party review across multiple reporting cycles. This is pushing software selection toward platforms that can keep one consistent emissions record across operating teams, finance teams, and supply chain functions. The pressure also favors vendors that can reduce the burden of duplicate reporting by linking carbon data with broader sustainability workflows. As a result, product depth in audit trails, record traceability, and verification support is becoming more important than basic reporting features alone.

Rising Data Center Power Efficiency Pressure

Power efficiency pressure in data centers is creating a separate but closely linked growth lane for the Japan green IT software market as operators face greater scrutiny on energy performance and utilization. The issue is widening beyond facility management because higher AI-related compute demand is making energy visibility, workload planning, and reporting more material to cost control and corporate decarbonization efforts. Software demand is therefore shifting toward tools that can connect energy data, utilization trends, and carbon outcomes in one operating view. NTT's March 2026 formalization of CO2 calculation rules for the full software lifecycle also broadened the discussion from hardware efficiency toward the carbon profile of software development and use itself. That development supports a wider market role for digital tools that can measure both operating energy performance and embedded software-related emissions across IT environments.

Legacy System Integration Complexity

Legacy system integration remains one of the clearest restraints on the Japan green IT software market because many enterprises still operate older ERP, production, and facility systems that were not built for open and continuous data exchange. The problem is most visible in manufacturing-heavy environments where emissions information often sits across part tables, production records, utility documents, and site-level systems that do not naturally connect. This slows deployment, raises customization costs, and makes implementation risk a bigger factor in vendor selection. NTT DATA Kansai's BIZXIM CFP launch reflected this challenge by focusing on direct carbon footprint extraction from production management data, which shows how much adaptation is still required in industrial settings. Vendors with stronger connector libraries and better implementation depth are therefore more likely to shorten sales cycles and reduce early churn in accounts that depend on older operational systems.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Cloud-Based Sustainability Workflows

- Scope 3 Data Demands From Large Customers

- Cybersecurity and Data Governance Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software represented 68.41% of the Japan green IT software market in 2025, which reflected a clear preference for owned and auditable digital workflows across corporate users. That preference fits a market where companies want direct control over emissions records, reporting steps, and compliance documentation rather than relying only on managed support. It also favors vendors that can keep configuration, workflow management, and data ownership inside the customer environment. Services, however, are projected to grow at 23.22% CAGR from 2026 to 2031, which shows that implementation, assurance preparation, and ongoing support are becoming more material as deployments move from pilot stage to operating scale. The mix therefore points to a market where software remains the core purchase, while services become more important as enterprises try to use those platforms in a consistent and verified way.

The services opportunity is being shaped by the practical work that follows software procurement, including onboarding suppliers, aligning internal teams, preparing documentation, and supporting review processes across repeated reporting cycles. This means demand is no longer limited to installation support, it increasingly includes readiness work that helps companies turn data collection into disclosures and auditable records. Vendors that can combine software subscriptions with structured assurance support are better placed to defend revenue and keep customers from fragmenting their workflow across too many partners. Zeroboard's assurance support package, launched for companies preparing for stricter disclosure requirements, illustrates how vendors are trying to widen their role beyond software alone. That supports a two-layer structure in which software anchors the system of record, while services help customers sustain usage, pass verification, and expand platform scope over time.

Cloud-based platforms held 63.41% of the Japan green IT software market size in 2025 and are also projected to grow at a 19.96% CAGR through 2031, which gives cloud a rare position as both the largest and fastest-growing deployment model. This dual role reflects the practical reality that large organizations need centralized access across dispersed facilities, multiple business units, and supplier networks. It also reflects a cost and usability advantage for smaller firms that cannot justify dedicated infrastructure for carbon accounting and sustainability reporting. On-premise systems still hold relevance in organizations with stricter control requirements, while hybrid models are gaining traction as a middle path for more sensitive use cases. The market is therefore not moving toward one rigid architecture, but toward deployment choices that balance scale, speed, and governance.

Cloud adoption is also being reinforced by visible enterprise examples that show how large and geographically dispersed users can standardize data intake across many sites. Asuene's work with SMBC Group across more than 3,000 locations, including the use of AI-driven OCR for utility invoice data extraction, is one example of how cloud-based models can reduce reporting friction in complex operating environments. Even so, the strongest differentiation is beginning to shift from hosting model alone toward the ability to preserve audit integrity and data control in more regulated environments. That is why hybrid deployment is becoming strategically important in banking, government, and healthcare, where buyers want cloud efficiency without giving up tight control over sensitive identifiers and records. In that sense, the deployment story in the Japan green IT software market is becoming less about pure cloud migration and more about trusted architecture design for repeatable compliance work.

Complete Report Scope:

- By Offering

- Software

- Services

- By Deployment

- Cloud-Based

- On-Premise

- Hybrid

- By Solution Type

- Carbon Management and Accounting Software

- ESG Reporting and Compliance Software

- Sustainability Data Management Platforms

- Decarbonization Planning Software

- Energy and Resource Optimization Software

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises

- By End-Use Industry

- IT and Telecommunications

- Manufacturing

- Banking, Financial Services, and Insurance (BFSI)

- Government and Public Sector

- Energy and Utilities

- Healthcare

- Retail and E-Commerce

- Construction and Infrastructure

- Other End User Industries

List of Companies Covered in this Report:

- Asuene Inc.

- Zeroboard Inc.

- Fujitsu Limited

- NEC Corporation

- NTT DATA Corporation

- Hitachi, Ltd.

- Ricoh Company, Ltd.

- Panasonic Holdings Corporation

- Toshiba Digital Solutions Corporation

- IBM Japan, Ltd.

- SAP Japan Co., Ltd.

- Microsoft Japan Co., Ltd.

- Oracle Corporation Japan

- Salesforce Japan K.K.

- Schneider Electric Japan Holdings Ltd.

- Honeywell Japan Ltd.

- Accenture Japan Ltd.

- Nomura Research Institute, Ltd.

- Mizuho Research and Technologies, Ltd.

- Persol Process and Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tighter GX Disclosure and Audit Expectations

- 4.2.2 Rising Data Center Power Efficiency Pressure

- 4.2.3 Shift Toward Cloud-Based Sustainability Workflows

- 4.2.4 Scope 3 Data Demands From Large Customers

- 4.2.5 AI-Enabled Automation for Carbon and Energy Analytics

- 4.2.6 Software Consolidation to Reduce IT Waste and License Sprawl

- 4.3 Market Restraints

- 4.3.1 Legacy System Integration Complexity

- 4.3.2 Cybersecurity and Data Governance Concerns

- 4.3.3 Shortage of Sustainability-Focused IT Talent

- 4.3.4 Localization and Audit-Readiness Gaps for Smaller Firms

- 4.4 Industry Value-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power Of Buyers

- 4.8.2 Bargaining Power Of Suppliers

- 4.8.3 Threat Of New Entrants

- 4.8.4 Threat Of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Solution Type

- 5.3.1 Carbon Management and Accounting Software

- 5.3.2 ESG Reporting and Compliance Software

- 5.3.3 Sustainability Data Management Platforms

- 5.3.4 Decarbonization Planning Software

- 5.3.5 Energy and Resource Optimization Software

- 5.4 By Enterprise Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End-Use Industry

- 5.5.1 IT and Telecommunications

- 5.5.2 Manufacturing

- 5.5.3 Banking, Financial Services, and Insurance (BFSI)

- 5.5.4 Government and Public Sector

- 5.5.5 Energy and Utilities

- 5.5.6 Healthcare

- 5.5.7 Retail and E-Commerce

- 5.5.8 Construction and Infrastructure

- 5.5.9 Other End User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Asuene Inc.

- 6.4.2 Zeroboard Inc.

- 6.4.3 Fujitsu Limited

- 6.4.4 NEC Corporation

- 6.4.5 NTT DATA Corporation

- 6.4.6 Hitachi, Ltd.

- 6.4.7 Ricoh Company, Ltd.

- 6.4.8 Panasonic Holdings Corporation

- 6.4.9 Toshiba Digital Solutions Corporation

- 6.4.10 IBM Japan, Ltd.

- 6.4.11 SAP Japan Co., Ltd.

- 6.4.12 Microsoft Japan Co., Ltd.

- 6.4.13 Oracle Corporation Japan

- 6.4.14 Salesforce Japan K.K.

- 6.4.15 Schneider Electric Japan Holdings Ltd.

- 6.4.16 Honeywell Japan Ltd.

- 6.4.17 Accenture Japan Ltd.

- 6.4.18 Nomura Research Institute, Ltd.

- 6.4.19 Mizuho Research and Technologies, Ltd.

- 6.4.20 Persol Process and Technology Co., Ltd.

7 MARKET OPPORTUNITIES ANDFUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment