PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073338

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073338

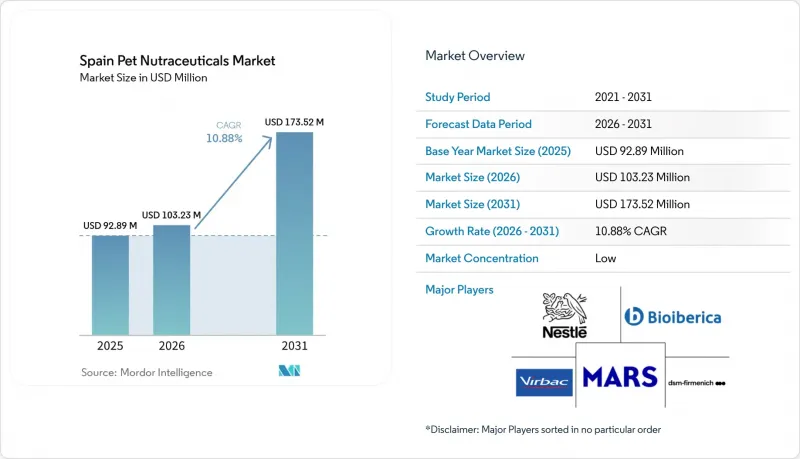

Spain Pet Nutraceuticals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the spain pet nutraceutical market was valued at USD 92.89 million in 2025 and is projected to grow from USD 103.23 million in 2026 to USD 173.52 million by 2031, with a CAGR of 10.88% during the forecasted period from 2026 to 2031.

This report is Segmented by Sub-Product (Milk Bioactives, Omega-3 Fatty Acids, Probiotics, Proteins and Peptides, Vitamins and Minerals, and More), by Pets (Cats, Dogs, and Other Pets), and by Distribution Channel (Convenience Stores, Online Channel, Specialty Stores, Supermarkets and Hypermarkets, and Other Channels). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Spain Pet Nutraceuticals Market Trends and Insights

Pet Humanization and Preventive Wellness Spending

Pet owners are increasingly prioritizing long-term wellness by using products that support mobility, digestive health, immunity, skin and coat health, and healthy aging. This trend is driving the adoption of daily nutritional supplements as a regular part of pet care routines. According to GlobalPETS in 2025, 9 out of 10 Spanish dog and cat owners make regular veterinary visits. These visits provide opportunities for veterinarians to recommend supplements, thereby enhancing awareness of preventive health solutions among pet owners.

Veterinary Recommendation Power in Supplement Adoption

Veterinary professionals educate pet owners on preventive nutrition, healthy aging, digestive health, mobility support, and other long-term wellness needs. Their recommendations foster trust in nutraceutical products and promote consistent usage among pet owners seeking reliable, evidence-based solutions. According to GlobalPETS in 2026, 23% of cat owners purchase pet products through veterinary clinics. This underscores the importance of veterinary channels in shaping consumer behavior and driving demand for professionally recommended nutritional supplements in Spain.

Labeling and Claims Compliance Limits Commercial Messaging

The market faces challenges stemming from stringent regulatory and labeling requirements for companion animal nutrition products. Manufacturers are required to adhere to ingredient authorization, labeling standards, safety documentation, and product communication regulations before product launches. These obligations can prolong development timelines and elevate compliance costs, especially for products aimed at digestive health, microbiome support, mobility, and other functional benefits. In September 2025, the European Pet Food Industry Federation (FEDIAF) published the 2025 edition of its Nutritional Guidelines for Complete and Complementary Pet Food for Cats and Dogs, which introduced updated standards for formulation, labeling, and marketing practices. The evolving regulatory landscape adds complexity to compliance processes and may delay product commercialization, particularly for smaller companies with limited regulatory resources.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of Microbiome-Targeted and Functional Formulations

- Aging Pets and Chronic Condition Management Demand

- Uneven Veterinary Trust Slows Conversion for New Brands

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Spain pet nutraceutical market share for vitamins and minerals accounted for the largest 27.0% in 2025. This segment maintains its leading position as it forms the foundation of preventive pet healthcare and is applicable across various life stages and health conditions. Pet owners often consider vitamin and mineral supplementation as an accessible entry point before transitioning to more specialized nutraceutical products. The category also enjoys strong acceptance among veterinarians and retailers due to its broad applicability in promoting overall wellness. Its versatility in daily maintenance, recovery support, and healthy aging continues to drive demand across companion animal populations.

Vitamins and minerals are projected to expand at the fastest CAGR of 11.4% from 2026 to 2031. This growth is driven by increasing consumer interest in preventive nutrition and routine wellness management for companion animals. As pet owners become more proactive in ensuring long-term health, the demand for products addressing nutritional gaps and supporting everyday vitality is rising. The segment also benefits from its integration into broader wellness programs recommended by veterinarians and specialty retail channels. Ongoing product innovation and the introduction of convenient administration formats further support adoption among both new and experienced pet supplement users.

Complete Report Scope:

- By Sub Product

- Milk Bioactives

- Omega-3 Fatty Acids

- Probiotics

- Proteins and Peptides

- Vitamins and Minerals

- Other Nutraceuticals

- By Pets

- Cats

- Dogs

- Other Pets

- By Distribution Channel

- Convenience Stores

- Online Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Other Channels

List of Companies Covered in this Report:

- Bioiberica, S.A.U. (SARIA SE & Co. KG)

- DSM-Firmenich AG

- Mars, Incorporated

- Nestle S.A.

- Virbac S.A.

- Vetoquinol S.A.

- Affinity Petcare, S.A. (Agrolimen)

- Alltech, Inc.

- Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company)

- Lallemand Inc.

- Nutreco N.V. (SHV Holdings N.V.)

- Petia Vet Health, S.L. (Zendal Group)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Pet Population

- 4.1.1 Cats

- 4.1.2 Dogs

- 4.1.3 Other Pets

- 4.2 Pet Expenditure

- 4.3 Consumer Trends

5 SUPPLY AND PRODUCTION DYNAMICS

- 5.1 Trade Analysis

- 5.2 Ingredient Trends

- 5.3 Value Chain and Distribution Channel Analysis

- 5.4 Regulatory Framework

- 5.5 Market Drivers

- 5.5.1 Pet humanization and preventive wellness spending

- 5.5.2 Veterinary recommendation power in supplement adoption

- 5.5.3 Rapid growth of microbiome-targeted and functional formulations

- 5.5.4 E-commerce and specialist channel expansion for premium products

- 5.5.5 Aging pets and chronic condition management demand

- 5.5.6 Demand for clean label and science-backed natural actives

- 5.6 Market Restraints

- 5.6.1 Labeling and claims compliance limits commercial messaging

- 5.6.2 Uneven veterinary trust slows conversion for new brands

- 5.6.3 Premium pricing limits mass-market penetration

- 5.6.4 Ingredient supply volatility in omega-3, probiotics, and collagen inputs

6 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 6.1 By Sub Product

- 6.1.1 Milk Bioactives

- 6.1.2 Omega-3 Fatty Acids

- 6.1.3 Probiotics

- 6.1.4 Proteins and Peptides

- 6.1.5 Vitamins and Minerals

- 6.1.6 Other Nutraceuticals

- 6.2 By Pets

- 6.2.1 Cats

- 6.2.2 Dogs

- 6.2.3 Other Pets

- 6.3 By Distribution Channel

- 6.3.1 Convenience Stores

- 6.3.2 Online Channel

- 6.3.3 Specialty Stores

- 6.3.4 Supermarkets/Hypermarkets

- 6.3.5 Other Channels

7 COMPETITIVE LANDSCAPE

- 7.1 Key Strategic Moves

- 7.2 Market Share Analysis

- 7.3 Brand Positioning Matrix

- 7.4 Market Claim Analysis

- 7.5 Company Landscape

- 7.6 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 7.6.1 Bioiberica, S.A.U. (SARIA SE & Co. KG)

- 7.6.2 DSM-Firmenich AG

- 7.6.3 Mars, Incorporated

- 7.6.4 Nestle S.A.

- 7.6.5 Virbac S.A.

- 7.6.6 Vetoquinol S.A.

- 7.6.7 Affinity Petcare, S.A. (Agrolimen)

- 7.6.8 Alltech, Inc.

- 7.6.9 Hill's Pet Nutrition, Inc. (Colgate-Palmolive Company)

- 7.6.10 Lallemand Inc.

- 7.6.11 Nutreco N.V. (SHV Holdings N.V.)

- 7.6.12 Petia Vet Health, S.L. (Zendal Group)

8 KEY STRATEGIC QUESTIONS FOR PET FOOD CEOS