PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073373

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073373

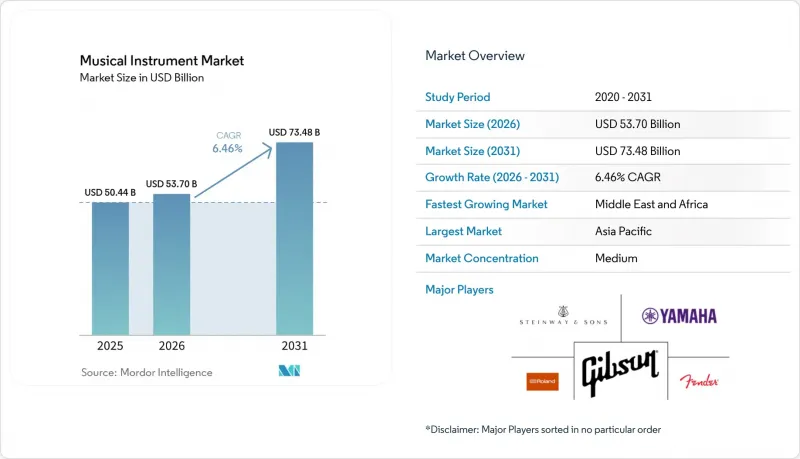

Musical Instrument - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the musical instrument market size was valued at USD 50.44 billion in 2025 and estimated to grow from USD 53.7 billion in 2026 to reach USD 73.48 billion by 2031, at a CAGR of 6.46% during the forecast period (2026-2031).

This report is Segmented by Product Type (String Instruments, Wind Instruments, and More), Distribution Channel (Offline Retail, Online Retail), Technology (Acoustic Instruments, Digital Instruments, Hybrid/Smart Instruments), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Musical Instrument Market Trends and Insights

Surge in Subscription-Based Remote Music Learning Platforms

Subscription-centric learning portals have dismantled geographical and economic barriers, heightening first-time purchases of entry-level keyboards and guitars across North America and Europe. Yamaha's School Project alone has connected with more than 3 million children, expanding its funnel for digital and acoustic starter models. Recurring fees motivate platform owners to continuously refresh curricula, keeping learners engaged and nudging periodic instrument upgrades. The alignment between structured lessons and instrument replacement cycles accelerates revenue stability for manufacturers. Moreover, data exhaust from these platforms furnishes granular insights into play patterns, narrowing feedback loops on product design. Together, these dynamics fuel sustained tailwinds for the musical instrument market.

Government-Backed Music-Education Mandates in Nordics and South Korea

Nordic governments and South Korea now embed multi-year funding for music into school budgets, anchoring predictable procurement of durable, education-grade instruments. England's Music Opportunities Pilot allocates GBP 5.8 million (USD 7.89 million) to supply lessons, instruments, and examinations for disadvantaged students. In the United States, California's Proposition 28 dedicates 1% of K-12 Proposition 98 monies to arts, reserving at least 80% for certified staff. Such mandates smooth order visibility for producers, yet skew specifications toward ruggedness and cost-efficiency over premium sound. Manufacturers thus balance feature sets to meet institutional price points while preserving margins.

Scarcity of CITES-Regulated Tonewoods Disrupting High-End Guitar Supply

Despite the 2024 easing for certain rosewood items under 10 kg, Brazilian Dalbergia remains tightly controlled, squeezing supplies for boutique luthiers and mass-market brands alike. Gibson and Martin now source FSC-certified alternatives, yet buyers often equate heritage timbers with tonal authenticity, limiting substitution elasticity. Resulting cost inflation narrows margins or pushes retail prices higher, dampening demand among aspirational amateurs. The premium guitar corridor therefore faces lingering volatility that tempers the otherwise upbeat musical instrument market trajectory.

Other drivers and restraints analyzed in the detailed report include:

- Social-Media-Driven "Bedroom Producer" Culture Boosting MIDI Controller Demand

- IoT-Enabled Smart Instruments Creating Recurring Revenue Streams

- Shift to Software-Only Virtual Instruments Reducing Entry-Level Keyboard Demand

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

String instruments delivered 27.45% of musical instrument market share in 2025, underscoring their foundational place across genres. In contrast, the electronic cohort led segment expansion with an 8.78% CAGR tailwind, propelled by rising demand for MIDI controllers, digital pianos, and electronic drums. Hybrid guitars that blend piezo pickups with modeled amplifiers have blurred acoustic-electric borders, appealing to live performers who need tonal versatility without pedalboard clutter. CITES-related tonewood scarcities prompted wider adoption of 3D-printed bridges and responsibly harvested pau ferro, keeping production lines fluid despite regulatory friction. Meanwhile, violin, viola, and cello categories benefit from conservatory programs, though growth remains modest relative to electronics.

Electronic innovation is also reshaping percussion. Apartment dwellers and content creators gravitate toward mesh-head kits with Bluetooth, satisfying both noise restrictions and mobile creativity. The infusion of sample libraries into hardware modules allows drummers to blend acoustic strikes with EDM layers on the fly. Above all, demand interplay between heritage craftsmanship and digital enhancement supports balanced portfolio strategies, illustrating why both traditional and electronic lines remain central pillars of the musical instrument market.

Complete Report Scope:

- By Product Type

- String Instruments

- Guitars

- Violins, Violas, Cellos

- Harps and Others

- Wind Instruments

- Brass

- Woodwind

- Percussion Instruments

- Acoustic Drums

- Electronic Drums and Pads

- Keyboard Instruments

- Acoustic Pianos

- Digital Pianos and Stage Pianos

- MIDI Controllers and Synthesizers

- Electronic Instruments

- DJ Controllers and Turntables

- Samplers and Workstations

- Accessories

- Pedals and Effects

- Strings, Reeds and Sticks

- Cases and Bags

- Other Product Types

- String Instruments

- By Distribution Channel

- Offline Retail

- Independent Music Stores

- Specialty Chains

- Online Retail

- Direct-to-Consumer Brand Stores

- E-commerce Marketplaces

- Offline Retail

- By Technology

- Acoustic Instruments

- Digital Instruments

- Hybrid/Smart Instruments

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Geography Analysis

Asia generated 33.45% of 2025 revenue, sustained by Japan's innovation leadership and a dense supplier ecosystem. Yet Chinese piano makers Pearl River and Hailun posted respective 31.47% and 21.99% revenue declines in 2023, reflecting softening middle-class sentiment and shifting parental priorities away from costly piano lessons. South Korea and Singapore counterbalance with government support, anchoring steady classroom demand. India's rising disposable income and widespread smartphone adoption offer fertile ground for app-linked guitars and keyboards, though import duties still constrain price competitiveness.

North America remains a premium outpost. Gibson, Fender, and Taylor command loyalty among hobbyists and touring artists, while classical education keeps orchestral instrument turnover steady. Yet acoustic piano shipments fell to fewer than 18,000 units in 2024, eclipsed by 188,000 digital pianos that cater to apartment dwellers. California's Proposition 28 secures ongoing school budgets, stabilizing low-to-mid price tiers.

The Middle East leads growth at 7.72% CAGR on the back of national cultural initiatives and expanding youth populations. Concert halls in Dubai, Riyadh, and Doha now specify smart stage pianos and modular PA rigs, fostering spill-over demand for practice instruments. Europe shows moderate but steady momentum. Germany's orchestral heritage sustains wind-instrument factories, while the Nordics channel public funds into school music kits that emphasize sustainability and digital integration. South America's potential remains tempered by Brazil's and Argentina's import tariffs, nudging local assembly operations but keeping prices elevated.

- Yamaha Corporation

- Fender Musical Instruments Corporation

- Gibson Brands Inc.

- Roland Corporation

- Steinway & Sons

- Korg Inc.

- Casio Computer Co. Ltd.

- Native Instruments

- C. F. Martin & Co.

- Pearl Musical Instrument Co.

- Arturia

- Ableton

- Moog Music

- inMusic Brands (Alesis, Akai Pro, etc.)

- PRS Guitars

- Ibanez (Hoshino Gakki)

- Behringer (Music Tribe)

- Donner Music

- DW Drums

- Gretsch Drums and Guitars

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Subscription-Based Remote Music Learning Platforms (North America, Europe)

- 4.2.2 Chinese Middle-Class Income Growth Accelerating Acoustic Piano Sales

- 4.2.3 Social-Media-Driven "Bedroom Producer" Culture Boosting MIDI Controller Demand

- 4.2.4 Government-Backed Music-Education Mandates in Nordics and South Korea

- 4.2.5 Eco-Friendly Tonewoods and Circular-Luthier Programs Differentiating Premium Guitars

- 4.2.6 IoT-Enabled Smart Instruments Creating Recurring Revenue Streams

- 4.3 Market Restraints

- 4.3.1 Scarcity of CITES-Regulated Tonewoods Disrupting High-End Guitar Supply

- 4.3.2 Import Tariffs on Finished Instruments in Brazil and Argentina

- 4.3.3 Shift to Software-Only Virtual Instruments Reducing Entry-Level Keyboard Demand

- 4.3.4 Fragmented After-Sales Networks in Africa Constraining Electronic Drum Adoption

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 String Instruments

- 5.1.1.1 Guitars

- 5.1.1.2 Violins, Violas, Cellos

- 5.1.1.3 Harps and Others

- 5.1.2 Wind Instruments

- 5.1.2.1 Brass

- 5.1.2.2 Woodwind

- 5.1.3 Percussion Instruments

- 5.1.3.1 Acoustic Drums

- 5.1.3.2 Electronic Drums and Pads

- 5.1.4 Keyboard Instruments

- 5.1.4.1 Acoustic Pianos

- 5.1.4.2 Digital Pianos and Stage Pianos

- 5.1.4.3 MIDI Controllers and Synthesizers

- 5.1.5 Electronic Instruments

- 5.1.5.1 DJ Controllers and Turntables

- 5.1.5.2 Samplers and Workstations

- 5.1.6 Accessories

- 5.1.6.1 Pedals and Effects

- 5.1.6.2 Strings, Reeds and Sticks

- 5.1.6.3 Cases and Bags

- 5.1.7 Other Product Types

- 5.1.1 String Instruments

- 5.2 By Distribution Channel

- 5.2.1 Offline Retail

- 5.2.1.1 Independent Music Stores

- 5.2.1.2 Specialty Chains

- 5.2.2 Online Retail

- 5.2.2.1 Direct-to-Consumer Brand Stores

- 5.2.2.2 E-commerce Marketplaces

- 5.2.1 Offline Retail

- 5.3 By Technology

- 5.3.1 Acoustic Instruments

- 5.3.2 Digital Instruments

- 5.3.3 Hybrid/Smart Instruments

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 South Korea

- 5.4.4.4 India

- 5.4.4.5 Australia

- 5.4.4.6 New Zealand

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Vendor Positioning Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 Yamaha Corporation

- 6.3.2 Fender Musical Instruments Corporation

- 6.3.3 Gibson Brands Inc.

- 6.3.4 Roland Corporation

- 6.3.5 Steinway & Sons

- 6.3.6 Korg Inc.

- 6.3.7 Casio Computer Co. Ltd.

- 6.3.8 Native Instruments

- 6.3.9 C. F. Martin & Co.

- 6.3.10 Pearl Musical Instrument Co.

- 6.3.11 Arturia

- 6.3.12 Ableton

- 6.3.13 Moog Music

- 6.3.14 inMusic Brands (Alesis, Akai Pro, etc.)

- 6.3.15 PRS Guitars

- 6.3.16 Ibanez (Hoshino Gakki)

- 6.3.17 Behringer (Music Tribe)

- 6.3.18 Donner Music

- 6.3.19 DW Drums

- 6.3.20 Gretsch Drums and Guitars

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment