PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073641

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073641

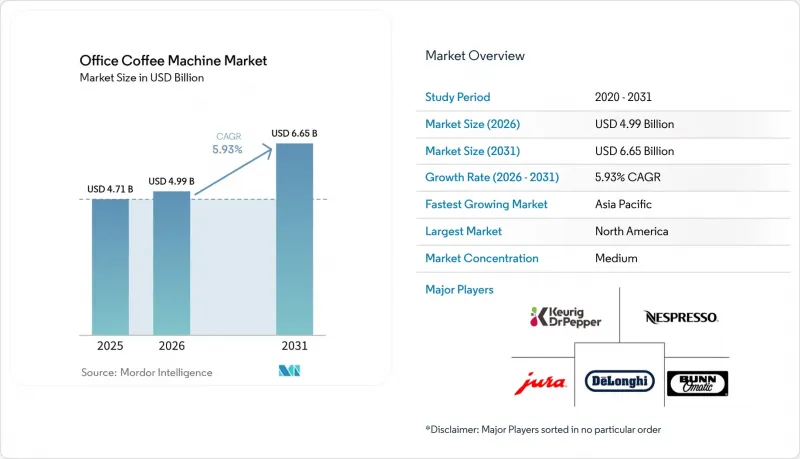

Office Coffee Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the office coffee machine market size was valued at USD 4.71 billion in 2025 and estimated to grow from USD 4.99 billion in 2026 to reach USD 6.65 billion by 2031, at a CAGR of 5.93% during the forecast period (2026-2031).

This report is Segmented by Type (Vending Machines, Pods/Capsule Coffee Machines, Automatic Espresso Machines), Capacity (Low-Volume (less Than 50 Cups/Day), Medium-Volume (50-200 Cups/Day), High-Volume (greater Than 200 Cups/Day)), Distribution Channel (Direct Sales, and Other), and Geography (North America, and Other). The Market Forecasts are Provided in Terms of Value (USD).

Global Office Coffee Machine Market Trends and Insights

Premium in-office coffee experiences

Companies view cafe-quality beverages as a cost-effective morale lever, prompting wider adoption of bean-to-cup machines that deliver fresh espresso, milk micro-foam, and flavor consistency. Global workplace surveys show three-quarters of employees link high-quality coffee with job satisfaction. Facilities teams now place machines in collaboration zones to spur informal meetings, mirroring designs pioneered by technology campuses. This shift propels demand for fully automatic platforms that brew multiple recipes from whole beans within 30 seconds. Producers respond with dual-hopper grinders so users can toggle between blends or switch to decaf. As premiumization spreads from headquarters to satellite sites, entry-level capsule models give way to mid-range super-automatic systems offering remote telemetry for ingredient usage tracking.

Hybrid work models elevating on-site perks

Return-to-office mandates compress coffee consumption into fewer days, yet they boost per-capita intake when employees are present. Office coffee service providers report double-digit revenue rebounds tied to concentrated midweek footfall. Management teams upgrade equipment to persuade staff that workplace beverages surpass home brewers. Hybrid scheduling further favors machines with rapid start-up times and minimal cleaning since utilization peaks in short bursts. Machine makers highlight one-touch latte functions and automatic milk rinses that support busy facilities crews. The hybrid trend also expands small-format deployments in co-working venues and flexible leases, benefiting suppliers that bundle rental, beans, and maintenance in a single monthly invoice.

Import tariffs on automatic machines

Import duties significantly impact automatic coffee machine accessibility in developing markets, with recent U.S. tariff implementations exemplifying broader trade tensions. The August 2025 U.S. tariff schedule imposed 50% duties on Brazilian green coffee and 40% on Vietnamese robusta, directly affecting ingredient costs for office coffee suppliers. These tariffs create landed cost increases of 20-30% for mid-sized importers and compel procurement strategy reassessment by major processors, including Nestle and J.M. Smucker. Emerging markets face similar barriers to fully automatic machine imports, limiting SME access to premium equipment and constraining market expansion in price-sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

- IoT-enabled predictive maintenance

- Corporate sustainability mandates

- Rising specialty coffee bean prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pods and capsule machines held the largest share thanks to plug-and-play operation and portion control that minimizes waste. Nonetheless, the automatic espresso category is on the rise as organizations seek cafe-level quality without barista labour. The office coffee machine market size for automatic espresso platforms is predicted to widen fastest because integrated grinders yield fresher brews and lower consumable cost per cup. Manufacturers are introducing touch-screen interfaces with swipeable drink menus, elevating user experience. Super-automatic units also connect to corporate Wi-Fi networks for usage analytics, a capability that appliances typically lack. Feature upgrades include automatic milk texturing modules and flavor powder stations, enabling menu diversity from a single footprint. Pods retain relevance where variable staff counts make fixed doses attractive, yet recycling obligations for aluminium capsules could dampen growth in jurisdictions with strict waste rules. Vending machines remain staples in transportation hubs and factories, but white-collar sites are gravitating to bean-to-cup systems that deliver higher perceived value.

Competitive differentiation now centers on extraction technology and maintainability. Patented pressure profiling replicates artisan espresso while adaptive burr grinders handle lighter roasts preferred by younger professionals. Self-service cleaning cycles reduce daily operator tasks, important for offices without dedicated pantry staff. Some premium models incorporate RFID readers to support cashless payments in public-access areas, extending revenue streams for facilities management firms. The office coffee machine market share of automatic espresso devices is therefore set to capture volume from both capsules and legacy vending. Suppliers investing in modular architecture can tailor boilers, grinders, and payment modules to site-specific needs, shortening lead times and simplifying after-sales support.

Complete Report Scope:

- By Type

- Vending Machines

- Pods / Capsule Coffee Machines

- Automatic Espresso Machines

- By Capacity

- Low-Volume (Less than 50 cups/day)

- Medium-Volume (50-200 cups/day)

- High-Volume (Greater than 200 cups/day)

- By Distribution Channel

- Direct Sales

- Dealers / Distributors

- Online Retail

- Rental / Lease Services

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (SG, MY, TH, ID, VN, PH)

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Geography Analysis

Europe maintains market leadership with a 27.92% share in 2025, supported by a mature coffee culture, stringent sustainability regulations, and an established commercial coffee infrastructure. The region benefits from regulatory frameworks, including the EU Deforestation-free Regulation (EUDR), that, despite implementation challenges, drive demand for traceable, sustainable coffee solutions. European companies lead circular economy initiatives, with JURA implementing recycling passes for end-of-life material recovery and Nespresso achieving carbon neutrality across its capsule lifecycle. Major European equipment manufacture, including Thermoplan, WMF Group, and Schaerer, G, leverage Swiss precision engineering and sustainability credentials to command premium positioning in global markets.

Asia-Pacific represents the fastest-growing region with 8.04% CAGR through 2031, driven by expanding corporate coffee culture and infrastructure development in key markets. China's branded coffee shop market reached 49,691 outlets in 2023 after 58% growth, with digital-first chains like Luckin Coffee demonstrating strong workplace delivery integration. The Philippines showcases rapid small-format chain expansion, with Pickup Coffee scaling from its first store in June 2022 to 300 sites by December 2024, indicating strong out-of-home consumption growth that supports workplace coffee demand. However, the region faces infrastructure constraints and tariff pressures that limit premium equipment penetration in price-sensitive segments.

North America demonstrates steady growth supported by return-to-office trends and corporate amenity investments, though market maturity constrains expansion rates compared to emerging regions. The region benefits from established office coffee service networks and strong single-serve system penetration led by Keurig Dr Pepper's dominant ecosystem. Recent consolidation, including KDP's USD 18 billion JDE Peet's acquisition, positions North America as the headquarters for the combined Global Coffee Co., potentially accelerating innovation and market development. The region's mature commercial real estate infrastructure supports premium equipment deployment, though aging buildings present plumbing and electrical upgrade requirements for advanced coffee systems.

- Keurig Dr Pepper

- Nestle (Nespresso)

- JURA Elektroapparate AG

- De'Longhi Group

- Bunn-O-Matic Corporation

- WMF Group

- Melitta Group

- Hamilton Beach Brands

- Newco Coffee

- La Marzocco

- Eversys AG

- Breville Group

- Saeco (Philips)

- Franke Coffee Systems

- Rhea Vendors Group

- Schaerer AG

- Animo B.V.

- Bravilor Bonamat

- Gruppo Cimbali (Faema, Gaggia)

- Gaggia

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for premium coffee experiences in corporate settings

- 4.2.2 Growing hybrid-working models boosting in-office perks

- 4.2.3 Declining total cost of ownership of bean-to-cup machines

- 4.2.4 Vendor financing & leasing innovations for SMEs (under-reported)

- 4.2.5 IoT-enabled predictive maintenance reducing downtime (under-reported)

- 4.2.6 Workplace sustainability mandates favouring energy-efficient units (under-reported)

- 4.3 Market Restraints

- 4.3.1 High import tariffs on fully-automatic machines in emerging markets

- 4.3.2 Rising specialty-coffee bean prices squeezing OPEX

- 4.3.3 Limited plumbing infrastructure in older office buildings

- 4.3.4 ESG scrutiny of single-use capsules (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Vending Machines

- 5.1.2 Pods / Capsule Coffee Machines

- 5.1.3 Automatic Espresso Machines

- 5.2 By Capacity

- 5.2.1 Low-Volume (Less than 50 cups/day)

- 5.2.2 Medium-Volume (50-200 cups/day)

- 5.2.3 High-Volume (Greater than 200 cups/day)

- 5.3 By Distribution Channel

- 5.3.1 Direct Sales

- 5.3.2 Dealers / Distributors

- 5.3.3 Online Retail

- 5.3.4 Rental / Lease Services

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South East Asia (SG, MY, TH, ID, VN, PH)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East & Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East & Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Keurig Dr Pepper

- 6.4.2 Nestle (Nespresso)

- 6.4.3 JURA Elektroapparate AG

- 6.4.4 De'Longhi Group

- 6.4.5 Bunn-O-Matic Corporation

- 6.4.6 WMF Group

- 6.4.7 Melitta Group

- 6.4.8 Hamilton Beach Brands

- 6.4.9 Newco Coffee

- 6.4.10 La Marzocco

- 6.4.11 Eversys AG

- 6.4.12 Breville Group

- 6.4.13 Saeco (Philips)

- 6.4.14 Franke Coffee Systems

- 6.4.15 Rhea Vendors Group

- 6.4.16 Schaerer AG

- 6.4.17 Animo B.V.

- 6.4.18 Bravilor Bonamat

- 6.4.19 Gruppo Cimbali (Faema, Gaggia)

- 6.4.20 Gaggia

7 Market Opportunities & Future Outlook

- 7.1 AI-driven personalization of beverage profiles

- 7.2 Carbon-neutral machine lines & circular capsule programs