PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1640689

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1640689

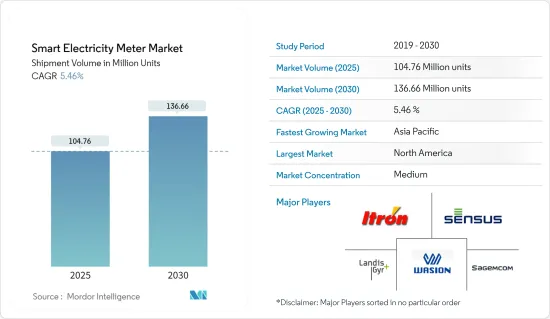

Smart Electricity Meter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Smart Electricity Meter Market size in terms of shipment volume is expected to grow from 104.76 million units in 2025 to 136.66 million units by 2030, at a CAGR of 5.46% during the forecast period (2025-2030).

Smart meters deployment enabled the implementation of a Home Energy Management System (HEMS) or Building Energy Management System (BEMS) that allows visualization of the electric power usage in individual homes or entire buildings.

Key Highlights

- Energy efficiency is increasingly becoming the primary focus globally, owing to the increasing economic activities, which led to high energy consumption rates and pushed global electricity grids to their limits. The global electricity generation in 2021 stood at 28,466 Terawatt-hours, according to BP.

- Digitization has been further accelerating and modernizing energy efficiency measures due to which the deployment of smart grids has been increasing globally, as they are capable of dynamically optimizing supply and fostering supply of large amounts of electricity from renewable energy sources, such as solar power.

- The recent COVID -19 outbreak and nationwide lockdown across the globe impacted the overall rollout of Smart meters globally. The global COVID -19 pandemic resulted in lockdowns in various parts of the world, which halted several operations across industries. As a result, the shipments and installations of smart meters were also affected.

- However, as the COVID-19 regulations are slowly being eased, the number of smart meters being installed is also expected to witness an increase in the long term. In many developed regions, most energy suppliers have been motivating their customers to upgrade to smart meters as it minimizes direct human interaction and offers several other benefits across the entire value chain, such as incentivizing energy conservation and facilitating easy bill payments, remote meter reading, improving billing and collection efficiency, reducing aggregate technical and commercial losses, and curbing power theft, among others.

- Consumer electronics, office equipment, and other plug loads consume nearly 15% to 20% of the total residential and commercial electricity while not in the primary mode. Most of this energy is consumed when they operate in low-power modes (even while they are not in use). Consumers are increasingly tending to install a smart energy management system to track such scenarios.

Smart Electricity Meter Market Trends

Residential Segment to Register Significant Growing

- Smart electric meter plays a significant role in the residential sector, as this meter measures the energy consumed by the consumers. The increasing smart grid investments and the surge in the rate of integration of renewable sources of power generation to the existing grids in developed economies are expected to support the growth of the smart electricity meter market.

- The meter measures the electricity consumption and communicates this to the central utility system. Globally, installations of these devices in the residential sector help in the reduction of CO2 emissions, owing to the increased consumer's inclination toward peak time savings of energy.

- The increasing residential construction activities and government mandates, like the EU 20-20-20 policy aiming to convert over 80% of the installed meter base to a smart one, have ensured growth prospects for the smart electricity meters market.

- Furthermore, as consumers move toward stand-alone energy generation systems, the interactive capacity of the Smart Grid will become more and more important. Rooftop solar electric systems and small wind turbines are now widely available and have become cost-effective for many homeowners and businesses. Installations of smart meters will help to effectively connect all these mini-power generating systems to the grid to help the overall power distribution and measurement process be effective and more efficient.

- Moreover, increasing urbanization and the increasing inclination toward the focus on developing urban lifestyles led to the expansion of deployment of smart home technologies and devices, which involves automatic control of electricity, light, and energy to avoid wastage. Hence, the increasing adoption of smart home devices and technologies across the homes globally is further expected to foster the growth in smart meters in the residential segment.

United States to Hold Significant Market Share

- The automatic meter reading solutions market has been reaching maturity in the United States, resulting in sluggish growth. Furthermore, according to the Institute for Electric Innovation in the United States, 115 million smart meters have been installed in the US by 2021.

- The replacement of first-generation meters and the shift to advanced metering infrastructure (with higher capabilities and improved technology) are expected to drive the smart electricity meters market in the future.

- Electric companies across the United States are leveraging smart meter data to monitor the health of the energy grid, restore electric service more quickly when outages occur, integrate distributed energy resources (DERs), and deliver energy services and solutions to customers. Furthermore, electricity companies in the United States are making significant investments to enhance the energy grid.

- Moreover, vendors in the region leveraging smart electric meters' potential by pairing them with additional tools, such as customer engagement tools and other incentive strategies, are expected to drive the adoption of smart electric meters in the market. For instance, Baltimore Gas and Electric enrolls its customers into its smart energy rewards program whenever the Smart electricity meter is installed. Customers receive feedback, peak time rebate incentives, and help reduce energy costs.

- Similarly, Pacific Gas & Electric, in the United States, reported AMI targeting a home retrofit program that delivers 3.5 times more energy savings in the targeted homes. Additionally, the integration of smart electric meters with technologies, such as data analytics, is expected to further foster the growth of the market studied in the region.

Smart Electricity Meter Industry Overview

The smart electricity meters market is moderately competitive and consists of several major players. The market is moderately fragmented, owing to the presence of many small and large players. These companies are leveraging strategic innovations and collaborative initiatives to increase their market share and increase their profitability. The companies operating in the market are also acquiring start-ups working on enterprise network equipment technologies to strengthen their product capabilities.

In October 2022, the power utilities of Andhra Pradesh announced a great up for rolling out a smart electricity meter project. The Union government decided to replace around 25 crore conventional meters with smart meters across India under the Smart Meter National Programme (SMNP).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Supportive Government Regulations in Key Regions

- 5.1.2 Rise in Smart City Deployment

- 5.2 Market Restraints

- 5.2.1 High Costs and Security Concerns

- 5.2.2 Integration Difficulties with Smart Meters

6 MARKET SEGMENTATION

- 6.1 By End-user

- 6.1.1 Residential

- 6.1.2 Commercial

- 6.1.3 Industrial

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Spain

- 6.2.2.3 Germany

- 6.2.2.4 Italy

- 6.2.2.5 France

- 6.2.2.6 Turkey

- 6.2.2.7 Nordics

- 6.2.2.8 Benelux

- 6.2.2.9 Rest of Europe

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.3.4 Australia and New Zealand

- 6.2.3.5 South Korea

- 6.2.3.6 Southeast Asia (Malaysia, Singapore, Thailand and Others)

- 6.2.3.7 Rest of Asia-Pacific

- 6.2.4 Latin America

- 6.2.4.1 Brazil

- 6.2.4.2 Mexico

- 6.2.4.3 Columbia

- 6.2.4.4 Chile

- 6.2.4.5 Rest of Latin America

- 6.2.5 Middle East & Africa

- 6.2.5.1 GCC

- 6.2.5.2 South Africa

- 6.2.5.3 Egypt

- 6.2.5.4 Rest of Africa

- 6.2.5.5 Rest of Middle East

- 6.2.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Landis+gyr Group AG

- 7.1.2 Wasion Group Holdings

- 7.1.3 Elster Group GMBH (Honeywell International Inc.)

- 7.1.4 Jiangsu Linyang Energy Co. Ltd

- 7.1.5 Sagemcom SAS

- 7.1.6 Ningbo Sanxing Electric Co. Ltd

- 7.1.7 Kamstrup A/S

- 7.1.8 Hexing Electric Company Ltd

- 7.1.9 Itron Inc.

- 7.1.10 Holley Technology Ltd

- 7.1.11 Nanjing Xinlian Electronics Co. Ltd

- 7.1.12 Sensus USA Inc. (Xylem Inc)

- 7.1.13 Shenzhen Hemei Group Co. Ltd

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET