PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939634

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1939634

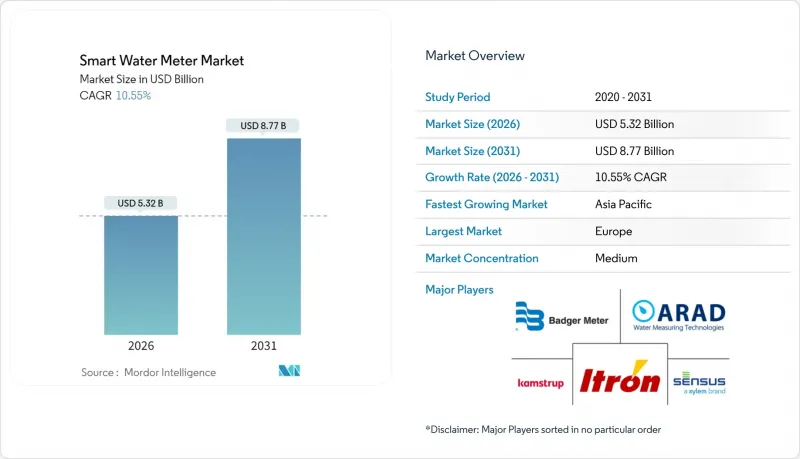

Smart Water Meter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Smart Water Meter market was valued at USD 4.81 billion in 2025 and estimated to grow from USD 5.32 billion in 2026 to reach USD 8.77 billion by 2031, at a CAGR of 10.55% during the forecast period (2026-2031).

Utilities continue to migrate from mechanical meters to connected devices that enable real-time monitoring, automated billing, and data-driven leak detection. Regulatory mandates for conservation, mounting pressure to replace aging distribution assets, and the expansion of Internet of Things platforms combine to accelerate adoption across utility classes. Vendor competition centers on integrating analytics and two-way communications while maintaining a favorable total cost of ownership. Expanding financing options, such as pay-as-you-save models, and performance-based regulation that rewards verified water-loss reduction, further strengthen demand pipelines in developed and emerging economies.

Global Smart Water Meter Market Trends and Insights

Supportive Government Regulations

Mandatory deployment timelines and water-efficiency standards push utilities toward advanced metering solutions that satisfy compliance and reporting needs. The EU Drinking Water Directive requires end-to-end monitoring, prompting Germany and France to stipulate smart meters in all new constructions and major renovations. California's permanent water-use rules demand granular data for enforcement, making AMI rollouts a prerequisite for funding eligibility. Utilities gain cost recovery mechanisms when they document water-loss cuts and customer engagement improvements, which lowers investment risk and supports full-territory deployments. Vendors benefit from volume orders that reduce per-unit costs, while policymakers secure transparent performance metrics to track conservation progress. Across municipal, regional, and national levels, regulation underwrites the long-term certainty needed for widespread Smart Water Meter market adoption.

Need to Improve Water-Use Efficiency

Utilities in water-scarce regions adopt connected meters to identify high-consumption patterns and empower customers with hourly data that supports behavioral changes. Industrial facilities using continuous telemetry report 20-30% consumption cuts after pinpointing leaks and optimizing processes. Agricultural pilots that combine soil-moisture sensing with weather-based scheduling record up to 28% savings, demonstrating cross-sector utility. Efficiency gains also yield energy savings because water production and pumping constitute large operational expenses. Analytics applications forecast demand, allowing utilities to flatten peaks and defer capacity expansion. As utilities tie conservation to revenue decoupling, efficiency gains translate into stable financial performance and propel the Smart Water Meter market forward.

High Upfront Costs and Cybersecurity Risks

Full AMI rollouts cost USD 200-400 per endpoint, challenging utilities with tight capital budgets. Rate-case approvals can stretch over several years, delaying project start dates. Cybersecurity countermeasures, encryption, intrusion detection, and 24-hour monitoring raise the total project expense by an additional 15-25%. Smaller systems, especially in developing economies, often defer investments without concessional finance. High-profile cyber incidents intensify regulatory scrutiny, further elevating compliance costs. These factors collectively weigh on Smart Water Meter market growth until financing mechanisms mature and security frameworks standardize.

Other drivers and restraints analyzed in the detailed report include:

- Reducing Non-Revenue Water Losses

- Smart-City and IoT Platform Integration

- Systems-Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automatic Meter Reading systems accounted for 57.10% of Smart Water Meter market share in 2025, reflecting their entrenched base and cost-efficient one-way data transmission. Many utilities adopt AMR during early modernization phases because drive-by collection sharply reduces manual labor without extensive network build-out. The Smart Water Meter market size attached to AMR remains large, yet its growth moderates as second-generation rollouts favor two-way architectures.

Advanced Metering Infrastructure records an 11.55% CAGR to 2031 as utilities seek real-time leak alerts, remote disconnect, and time-variant pricing schemes. Cellular, NB-IoT, and LoRaWAN modules drop in cost, erasing a key barrier to AMI adoption. Service providers package meters, analytics, and software subscriptions, distributing capital costs over operating budgets. Data-rich AMI platforms integrate easily with conservation programs, accelerating regional penetration and widening the Smart Water Meter market.

Residential deployments formed 58.00% of the Smart Water Meter market size in 2025 after multiple European and North American mandates required smart meters for new housing. Consumers benefit from usage portals that connect conservation goals to tangible savings, sustaining stable replacement cycles.

Commercial buildings show the fastest uptake at a 11.85% CAGR, propelled by facility-management software that pairs water, energy, and HVAC data. High-rise real-estate owners justify investment through lower operating expenses and green-building certifications. Retail chains and hospitality groups apply analytics to benchmark sites, uncover concealed leaks, and optimize irrigation. As sustainability reporting frameworks tighten, enterprise users expand deployments, bolstering overall Smart Water Meter market growth.

The Smart Water Meter Market Report is Segmented by Technology (Automatic Meter Reading & Advanced Metering Infrastructure), Application (Residential, and More), Meter Type (Mechanical/Turbine, Ultrasonic, and Electromagnetic), Communication Technology (Radio-Frequency, LoRaWAN/Other LPWAN, and More), Component (Hardware, Software and Analytics, and Services), Deployment (New Installations and Retrofit/Replacement), and Geography.

Geography Analysis

Europe dominated the Smart Water Meter market with 36.10% revenue share in 2025, anchored by EU directives that compel water-loss tracking and transparent billing. National implementation roadmaps guarantee steady tender pipelines, and long-term vendor frameworks streamline procurement. Utilities also tap recovery funds targeting climate resilience, accelerating district-wide AMI deployments that underpin stable regional demand.

Asia-Pacific registers the fastest expansion, clocking a 12.05% CAGR to 2031. China's extensive smart-city pilots embed metering within neighborhood digital twins, while India's Jal Jeevan Mission finances rural connections that include smart endpoints. Southeast Asian economies such as Indonesia and Vietnam upgrade legacy assets concurrently with rapid urbanization, avoiding sunk costs tied to older technologies. Government grants, multilateral loans, and public-private partnerships combine to scale installations and enlarge the Smart Water Meter market.

North America benefits from aging infrastructure replacement and statewide conservation mandates. California utilities deploy AMI to enforce per-capita usage limits and to support wildfire resilience through remote shut-off capabilities. Canada advances province-level modernization programs focusing on non-revenue water recovery, adding incremental growth. Latin America's concession tenders in Brazil signal sizable upcoming opportunities, while Middle East and Africa utilities leverage smart meters to address scarcity and reduce theft, though deployment progress varies by funding availability and communication-network readiness.

- Arad Ltd.

- Badger Meter Inc.

- Itron Inc.

- Sensus USA Inc. (Xylem Inc.)

- Kamstrup A/S

- Diehl Stiftung and Co. KG

- Zenner International GmbH and Co. KG

- Landis+Gyr Group AG

- Honeywell International Inc.

- Neptune Technology Group Inc. (Roper)

- Aclara Technologies LLC (Hubbell)

- Apator SA

- Axioma Metering

- B Meters Srl

- Datamatic Inc.

- Maddalena S.p.A.

- Suntront Tech Co., Ltd.

- Mueller Systems LLC

- Waviot

- Watertech S.p.A. (Arad)

- Jiangxi Sanchuan Water Meter Co. Ltd.

- Ningbo Water Meter Co. Ltd.

- BETAR Company

- Integra Metering AG

- IESLab Electronic Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Supportive government regulations

- 4.2.2 Need to improve water-use efficiency

- 4.2.3 Reducing non-revenue water (NRW) losses

- 4.2.4 Smart-city and IoT platform integration

- 4.2.5 Pay-as-you-save financing models

- 4.2.6 Drought-driven conservation mandates

- 4.3 Market Restraints

- 4.3.1 High upfront costs and cybersecurity risks

- 4.3.2 Systems-integration complexity

- 4.3.3 Shortage of utility data-analytics talent

- 4.3.4 Battery-life limits in ultrasonic units

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 ROI Analysis for Smart Meters

- 4.9 Protocol Benchmarking and Comparison

- 4.10 LoRaWAN Implementation Steps and Use-cases

- 4.11 Utility Digitalisation Benefits

- 4.12 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Technology

- 5.1.1 Automatic Meter Reading (AMR)

- 5.1.2 Advanced Metering Infrastructure (AMI)

- 5.2 By Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.2.3 Industrial

- 5.2.4 Agricultural

- 5.3 By Meter Type

- 5.3.1 Mechanical / Turbine

- 5.3.2 Ultrasonic

- 5.3.3 Electromagnetic

- 5.4 By Communication Technology

- 5.4.1 Radio-frequency (Proprietary RF)

- 5.4.2 LoRaWAN / Other LPWAN

- 5.4.3 Cellular (NB-IoT/LTE-M)

- 5.4.4 Wired (M-Bus/Ethernet)

- 5.5 By Component

- 5.5.1 Hardware

- 5.5.2 Software and Analytics

- 5.5.3 Services

- 5.6 By Deployment

- 5.6.1 New Installations

- 5.6.2 Retrofit / Replacement

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Chile

- 5.7.2.4 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Malaysia

- 5.7.4.6 Singapore

- 5.7.4.7 Australia

- 5.7.4.8 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 United Arab Emirates

- 5.7.5.1.2 Saudi Arabia

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Nigeria

- 5.7.5.2.3 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Arad Ltd.

- 6.4.2 Badger Meter Inc.

- 6.4.3 Itron Inc.

- 6.4.4 Sensus USA Inc. (Xylem Inc.)

- 6.4.5 Kamstrup A/S

- 6.4.6 Diehl Stiftung and Co. KG

- 6.4.7 Zenner International GmbH and Co. KG

- 6.4.8 Landis+Gyr Group AG

- 6.4.9 Honeywell International Inc.

- 6.4.10 Neptune Technology Group Inc. (Roper)

- 6.4.11 Aclara Technologies LLC (Hubbell)

- 6.4.12 Apator SA

- 6.4.13 Axioma Metering

- 6.4.14 B Meters Srl

- 6.4.15 Datamatic Inc.

- 6.4.16 Maddalena S.p.A.

- 6.4.17 Suntront Tech Co., Ltd.

- 6.4.18 Mueller Systems LLC

- 6.4.19 Waviot

- 6.4.20 Watertech S.p.A. (Arad)

- 6.4.21 Jiangxi Sanchuan Water Meter Co. Ltd.

- 6.4.22 Ningbo Water Meter Co. Ltd.

- 6.4.23 BETAR Company

- 6.4.24 Integra Metering AG

- 6.4.25 IESLab Electronic Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment