PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797886

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797886

Molecular Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

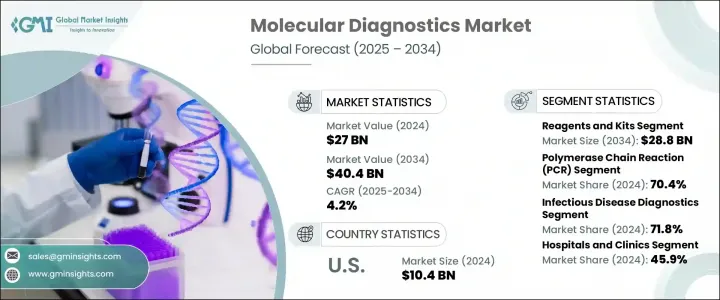

The Global Molecular Diagnostics Market was valued at USD 27 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 40.4 billion by 2034. This steady growth is being fueled by multiple converging factors such as rising cases of infectious diseases, continuous innovation in molecular diagnostic technologies, growing awareness of early disease detection, the surging need for point-of-care (POC) diagnostics, and the rapid expansion of the global elderly population.

Molecular diagnostics serves as a vital technique in identifying and monitoring diseases by analyzing biological markers in the genome and proteome, including DNA, RNA, and proteins. With healthcare systems under pressure to deliver faster and more accurate diagnostic solutions, this technique is playing an increasingly central role in modern clinical practice. Major players in the market-such as Thermo Fisher Scientific, Hologic, Sysmex Corporation, Danaher Corporation, and Qiagen-continue to expand their offerings to meet evolving global health needs.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $27 Billion |

| Forecast Value | $40.4 Billion |

| CAGR | 4.2% |

Molecular diagnostics involves highly sensitive and accurate tests that are critical for identifying a wide array of conditions, including genetic disorders, cancers, and infectious diseases. This accuracy is driving its adoption across both developed and emerging markets. Among the technologies used, polymerase chain reaction (PCR) led the market in 2024 with a 70.4% share. Its precise amplification of RNA and DNA and ability to detect even the smallest quantities of genetic material make PCR an essential tool for early detection, especially for infectious disease screening and genetic testing.

The oncology testing segment was valued at USD 2.1 billion in 2024 and is projected to reach USD 3.2 billion by 2034. Increasing cancer incidence across the globe, along with a rising demand for early diagnosis, is driving the uptake of advanced molecular testing tools in oncology. Healthcare systems are investing in molecular-based instruments, kits, and reagents that enable high sensitivity and specificity, improving patient outcomes and advancing cancer management protocols.

United States Molecular Diagnostics Market generated 10.4 billion in 2024. The U.S. and Canadian markets are witnessing significant momentum due to the continued rise of infectious diseases and strong support for the development and commercialization of next-generation diagnostic technologies. Even with strict regulatory standards in place, there is notable encouragement for the rollout of innovative diagnostic instruments and kits. Technological advancement and widespread adoption of sophisticated molecular testing platforms are helping to drive the market further in North America.

Leading companies operating in the Global Molecular Diagnostics Market include F. Hoffmann-La Roche, Qiagen, Agilent Technologies, Biocartis, Thermo Fisher Scientific, Siemens Healthineers, Abbott Laboratories, QuidelOrtho Corporation, Bio-Rad Laboratories, Illumina, Becton, Dickinson and Company, Sysmex Corporation, Huwel Lifesciences, Biomerieux, Danaher Corporation, and Hologic. To solidify their positions in the competitive molecular diagnostics space, companies are actively pursuing strategic alliances, mergers, and acquisitions. They are also focused on investing in R&D to innovate high-throughput, automated, and multiplex testing platforms. Expanding product portfolios, obtaining regulatory approvals, and entering new regional markets are helping players scale their global footprint. Additionally, integration of AI and digital platforms is enhancing diagnostic accuracy and speed, providing a technological edge.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Technology

- 2.2.3 Application

- 2.2.4 End use

- 2.2.5 Regional

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Technological advances and increasing awareness towards early disease diagnosis globally

- 3.2.1.2 Escalating demand for POC diagnostics

- 3.2.1.3 Increasing geriatric population base

- 3.2.1.4 Increasing number of R&D initiatives

- 3.2.1.5 Rising incidences of infectious diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of molecular diagnostic tests

- 3.2.2.2 Lack of skilled personnel

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging markets

- 3.2.3.2 Integration with artificial intelligence (AI)

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Technology and innovation landscape

- 3.4.1 Current technological trends

- 3.4.2 Emerging technologies

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East and Africa

- 3.6 Future market trends

- 3.7 Pricing analysis

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Instruments

- 5.3 Reagents and kits

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Polymerase chain reaction (PCR)

- 6.3 Hybridization

- 6.4 Sequencing

- 6.5 Isothermal nucleic acid amplification technology (INAAT)

- 6.6 Microarrays

- 6.7 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Infectious disease diagnostics

- 7.2.1 COVID-19

- 7.2.2 Flu

- 7.2.3 Respiratory syncytial virus (RSV)

- 7.2.4 Tuberculosis

- 7.2.5 CT/NG

- 7.2.6 HIV

- 7.2.7 Hepatitis C

- 7.2.8 Hepatitis B

- 7.2.9 Other infectious disease diagnostics

- 7.3 Genetic disease testing

- 7.4 Oncology testing

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and clinics

- 8.3 Diagnostic laboratories

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 Agilent Technologies

- 10.3 Becton, Dickinson, and Company

- 10.4 Biocartis

- 10.5 Biomerieux

- 10.6 Bio-Rad Laboratories

- 10.7 Danaher Corporation

- 10.8 F. Hoffmann-La Roche

- 10.9 Hologic

- 10.10 Huwel Lifesciences

- 10.11 Illumina

- 10.12 Qiagen

- 10.13 QuidelOrtho Corporation

- 10.14 Siemens Healthineers

- 10.15 Sysmex Corporation

- 10.16 Thermo Fisher Scientific