PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045745

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045745

Controlled Release Fertilizers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

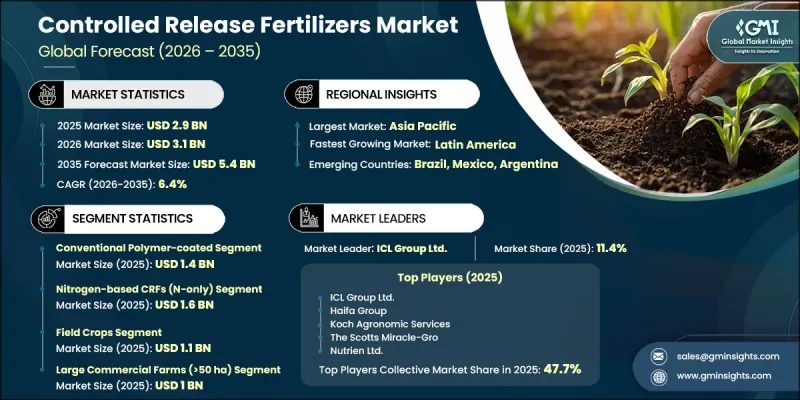

The Global Controlled Release Fertilizers Market was valued at USD 2.9 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 5.4 billion by 2035.

Controlled release fertilizers are specialized nutrient formulations designed to supply crops with essential nutrients gradually over an extended period. Unlike conventional fertilizers that release nutrients immediately after application, these products deliver nutrients at a controlled pace influenced by factors such as temperature, moisture levels, and microbial activity in the soil. This regulated nutrient distribution supports consistent crop development while improving nutrient availability throughout the plant growth cycle. The increasing emphasis on sustainable agriculture, precision farming, and efficient nutrient utilization continues to strengthen market demand. Farmers and commercial growers are increasingly adopting these fertilizers to reduce nutrient losses caused by leaching, runoff, and volatilization while enhancing crop productivity. Rising concerns regarding soil degradation, water conservation, and environmental sustainability are also contributing to broader product adoption across global agricultural systems. Controlled release fertilizers are widely utilized in agriculture, horticulture, landscaping, and turf management where maintaining long-term soil fertility and stable plant nutrition remains essential. Advancements in coating technologies and nutrient delivery systems are further improving fertilizer efficiency, encouraging growers to transition toward advanced crop nutrition solutions that support higher yields and improved soil management practices.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $2.9 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 6.4% |

Controlled release fertilizers are manufactured using advanced coating technologies that slow nutrient dissolution and provide crops with a steady nutrient supply over time. These fertilizers are increasingly preferred in crops with longer growth cycles because they maintain balanced nutrient levels throughout the cultivation period, helping improve plant health and overall agricultural productivity. Growing awareness among farmers regarding efficient fertilizer application and sustainable farming methods is accelerating product demand across both developed and emerging agricultural economies. In addition, increasing regulatory pressure associated with nutrient runoff and environmental protection is encouraging the adoption of fertilizers that improve nutrient absorption efficiency while reducing ecological impact. The market is also benefiting from rising investments in precision agriculture technologies and modern farming techniques that prioritize resource optimization and long-term soil productivity. As agricultural operations continue to focus on maximizing crop output while minimizing environmental impact, controlled release fertilizers are expected to remain a critical component of modern nutrient management strategies.

The conventional polymer-coated segment accounted for USD 1.4 billion in 2025. Demand for traditional polymer-coated fertilizers continues to remain strong because these products provide predictable nutrient release patterns and reliable crop performance across a wide range of agricultural applications. Their ability to maintain nutrient consistency over extended periods makes them highly suitable for commercial farming operations and large-scale crop production. At the same time, sulfur-coated fertilizers are attracting growing attention due to their cost efficiency and dual nutrient delivery benefits. These products not only provide controlled nutrient release but also supply sulfur, which is essential for plant growth and soil health. Increasing adoption across large-scale field crop cultivation and commercial agriculture is expected to further support segment growth.

The nitrogen-based controlled release fertilizers segment captured USD 1.6 billion in 2025. These fertilizers continue to witness strong demand because nitrogen plays a critical role in promoting vegetative growth, improving chlorophyll production, and supporting overall crop development. Farmers increasingly prefer nitrogen-based controlled release products due to their ability to enhance nitrogen use efficiency while minimizing nutrient wastage. Additionally, balanced nutrient formulations such as NPK controlled release fertilizers are gaining greater traction across diverse cropping systems and varying soil conditions. These formulations help deliver a more comprehensive nutrient profile, enabling improved crop performance and long-term soil fertility management. Growing demand for high-efficiency fertilizers capable of supporting precision agriculture and sustainable crop production practices is expected to further drive adoption of nitrogen-based and multi-nutrient controlled release fertilizer products during the forecast period.

North America Controlled Release Fertilizers Market is projected to grow from USD 568.3 million in 2025 to USD 1 billion by 2035. Regional demand is fueled by the rapid expansion of large-scale commercial agriculture and increasing focus on advanced nutrient management strategies. Farmers across North America are prioritizing fertilizer technologies that improve nutrient efficiency while helping meet environmental regulations related to runoff control and soil conservation. In the United States, growing adoption of precision farming technologies and rising investments in modern agricultural inputs are accelerating market growth. Controlled release fertilizers are also witnessing higher utilization across specialty crops, turf care, landscaping, and greenhouse cultivation due to their ability to deliver consistent crop nutrition and improve operational efficiency. Increasing awareness regarding sustainable agricultural practices and the need for long-term soil productivity are expected to continue supporting regional market expansion throughout the forecast period.

Major companies operating in the Global Controlled Release Fertilizers Market include Nutrien Ltd., ICL Group Ltd., Koch Agronomic Services, Yara International ASA, The Mosaic Company, Haifa Group, The Scotts Miracle-Gro Company, Kingenta Ecological Engineering, COMPO EXPERT GmbH, and SQM. These industry participants are actively focusing on product innovation, expansion of production capabilities, and advanced nutrient technologies to strengthen their competitive position and expand their presence across global agricultural markets. Companies operating in the controlled release fertilizers market are increasingly adopting strategic initiatives focused on innovation, sustainability, and geographic expansion to strengthen their market position. Major manufacturers are investing heavily in research and development to introduce advanced coating technologies that improve nutrient release efficiency and reduce environmental impact. Businesses are also expanding partnerships with agricultural distributors, precision farming companies, and commercial growers to improve product accessibility and strengthen customer relationships. In addition, companies are increasing investments in sustainable fertilizer solutions that align with environmental regulations and modern farming requirements. Expanding production facilities in high-growth agricultural regions and introducing customized nutrient formulations for specific crop applications are further supporting market penetration.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Coating Technology

- 2.2.2 Nutrient Composition

- 2.2.3 Crop Type

- 2.2.4 End User

- 2.2.5 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising focus on efficient nutrient use agriculture

- 3.2.1.2 Increasing adoption of precision farming practices globally

- 3.2.1.3 Longer crop cycles requiring sustained nutrient supply

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Higher initial costs compared with conventional fertilizers

- 3.2.2.2 Limited farmer awareness in developing agricultural regions

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for sustainable soil nutrient management

- 3.2.3.2 Expansion of horticulture and turfgrass applications worldwide

- 3.2.3.3 Advancements in biodegradable coating material technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By nutrient composition

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Coating Technology, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Sulfur-based coatings

- 5.3 Conventional polymer-coated

- 5.4 Biodegradable polymer-coated

- 5.5 Other coated & encapsulated fertilizers

Chapter 6 Market Estimates and Forecast, By Nutrient Composition, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Nitrogen-based CRFs (N-only)

- 6.3 Phosphorus-based CRFs (P-only)

- 6.4 Potassium-based CRFs (K-only)

- 6.5 NPK blends (multi-nutrient CRFs)

- 6.6 Specialty micronutrient CRFs

Chapter 7 Market Estimates and Forecast, By Crop Type, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Field crops

- 7.3 Specialty & plantation crops

- 7.4 Citrus & subtropical fruits

- 7.5 Horticulture - vegetables & temperate fruits

- 7.6 Horticulture - nursery & floriculture

- 7.7 Turf & landscape

- 7.8 Others

Chapter 8 Market Estimates and Forecast, By End User, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Large commercial farms (>50 ha)

- 8.3 Professional/institutional

- 8.4 Mid-size commercial farms (10-50 ha)

- 8.5 Smallholder farms & cooperatives (<10 ha)

- 8.6 Other

Chapter 9 Market Estimates and Forecast, By Distribution channel, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Direct sales (manufacturer to end user)

- 9.3 Distributors & chemical traders

- 9.4 Specialty chemical suppliers

- 9.5 Online platforms

- 9.6 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 ICL Group Ltd.

- 11.2 Haifa Group

- 11.3 Koch Agronomic Services

- 11.4 The Scotts Miracle-Gro

- 11.5 Nutrien Ltd.

- 11.6 Yara International ASA

- 11.7 The Mosaic Company

- 11.8 Kingenta Ecological Engineering

- 11.9 COMPO EXPERT GmbH

- 11.10 SQM