PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073598

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2073598

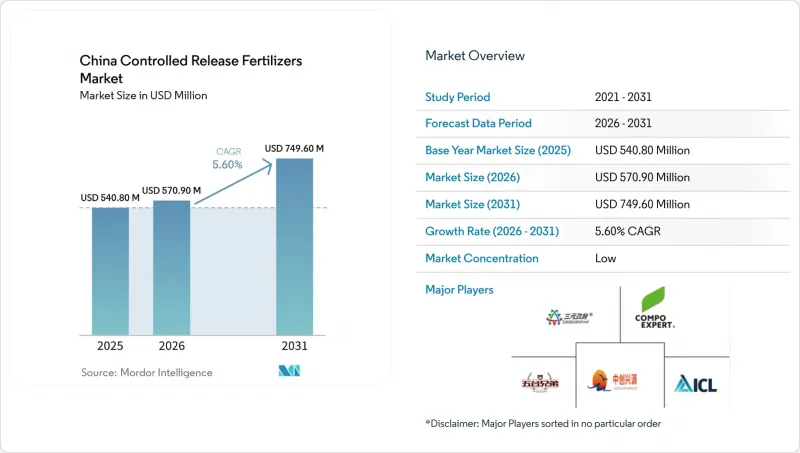

China Controlled Release Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the china controlled release fertilizers market size was valued at USD 540.80 million in 2025 and is estimated to grow from USD 570.90 million in 2026 to USD 749.60 million by 2031, at a CAGR of 5.60% during the forecast period (2026-2031).

This report is Segmented by Coating Type (Polymer Coated, Polymer-Sulfur Coated, and Others) and by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons)

China Controlled Release Fertilizers Market Trends and Insights

Government Eco-Subsidies for Efficiency Fertilizers

Central government subsidies under the Ministry of Agriculture and Rural Affairs' 2025+ framework reimburse 30% of controlled-release fertilizer costs for certified eco-farms, creating a direct economic incentive that narrows the price gap with conventional fertilizers. This policy intervention addresses the primary adoption barrier while advancing China's agricultural sustainability objectives. The subsidy mechanism operates through provincial agricultural bureaus, with Jiangsu Province leading implementation by covering over 2 million mu of rice paddies in 2024. The program's expansion to additional provinces in 2025 creates a multiplier effect where early adopters demonstrate yield improvements of 5-6%, encouraging neighboring farms to transition. Compliance requirements under the Green Food certification system ensure that subsidized farms maintain nutrient use efficiency standards, creating a self-reinforcing cycle of sustainable practices adoption.

Rising Labor Costs Driving Mechanized, Low-Touch Nutrition

Agricultural labor costs exceeding CNY 180 per day (USD 25) in major farming regions force growers to adopt mechanized, low-maintenance fertilization regimes where controlled-release products reduce application frequency from 3-4 times to once per season. This labor arbitrage creates compelling economics for CRF adoption, particularly in rice and corn production systems where manual broadcasting represents 15-20% of total production costs. Northeast China's large-scale farming operations demonstrate the clearest adoption patterns, with mechanized transplanting systems incorporating slow-release fertilizers achieving 25% labor cost reductions compared to conventional split applications. The trend accelerates as rural-urban migration continues, with agricultural employment declining 3% annually while remaining workers command premium wages. Smart application equipment manufacturers like Lovol and Zoomlion integrate CRF-compatible systems into their machinery offerings, creating technology lock-in effects that sustain demand growth.

Premium Price Gap Versus Conventional Bulk NPK

Controlled-release fertilizers command 2-3 times the price of conventional bulk NPK, creating affordability barriers for smallholder farmers who operate on margins below 10% of revenue and lack access to agricultural credit for premium inputs. This price differential becomes particularly constraining during commodity price downturns when farmers prioritize cost reduction over efficiency gains. China's 200 million smallholder farming households, averaging 0.6 hectares per operation, struggle to justify CRF premiums without demonstrated yield improvements exceeding 15% . Regional price sensitivity varies significantly, with Central and Southwest China showing the highest resistance due to lower crop values and limited mechanization. Fertilizer cooperatives and bulk purchasing programs provide partial solutions, but coverage remains limited to 30% of eligible farms, constraining market penetration in price-sensitive segments.

Other drivers and restraints analyzed in the detailed report include:

- Tighter Nutrient-Runoff Regulations

- Smart-Fertigation Demand for Steady Nutrient Release

- Polymer-Feedstock Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The polymer-coated fertilizer segment dominates the Chinese controlled-release fertilizer market, commanding about 72.4% market share in 2025. This segment's prominence stems from its superior ability to regulate nutrient release through tailored coating characteristics, thickness, and material ratios aligned with specific crop needs. Within this category, polymer-coated urea fertilizer has emerged as the leading variant, particularly valued for its nitrogen efficiency and potential to reduce nitrogen fertilizer use by 30% to 40%.

Polymer sulfur-coated products are projected to be the fastest-growing coating type, with a projected CAGR of 6.2% through 2031. This growth is driven by lower coating costs and the ability to provide extended nutrient release for broad-acre crops. Additionally, polymer-coated fertilizers maintain a strong market position due to increasing adoption in horticultural and ornamental crops, where precise nutrient-release requirements and environmental considerations are essential. Advancements in coating technologies and materials continue to enhance the market by enabling manufacturers to optimize yields while addressing environmental sustainability.

Complete Report Scope:

- Coating Type

- Polymer Coated

- Polymer-Sulfur Coated

- Others

- Crop Type

- Field Crops

- Horticultural Crops

- Turf & Ornamental

List of Companies Covered in this Report:

- Hebei Woze Wufeng Biological Technology Co., Ltd

- Grupa Azoty S.A. (Compo Expert)

- Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- Zhongchuang xingyuan chemical technology co.ltd

- Kingenta Ecological Engineering Group Co., Ltd.

- Sinochem Holdings Corporation Ltd.

- Xinyangfeng Agricultural Technology Co., Ltd.

- Stanley Agriculture Group Co., Ltd.

- Haifa Group

- Luxi Chemical Group Co., Ltd.

- Shikefeng Chemical Industry Co., Ltd.

- ICL Group Ltd.

- Zhongchuang Xingyuan Chemical Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY & KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Acreage Of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1 Primary Nutrients

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Government eco-subsidies for efficiency fertilizers

- 4.5.2 Rising labor costs driving mechanized, low-touch nutrition

- 4.5.3 Tighter nutrient-runoff regulations post

- 4.5.4 Smart-fertigation demand for steady nutrient release

- 4.5.5 Carbon-credit pilots rewarding nitrogen-use efficiency

- 4.5.6 E-commerce platforms expanding rural product access

- 4.6 Market Restraints

- 4.6.1 Premium price gap versus conventional bulk NPK

- 4.6.2 Limited public R&D funding for specialty coatings

- 4.6.3 Pending micro-plastic coating legislation

- 4.6.4 Polymer-feedstock price volatility

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Coating Type

- 5.1.1 Polymer Coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Others

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Turf & Ornamental

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Hebei Woze Wufeng Biological Technology Co., Ltd

- 6.4.2 Grupa Azoty S.A. (Compo Expert)

- 6.4.3 Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

- 6.4.4 Zhongchuang xingyuan chemical technology co.ltd

- 6.4.5 Kingenta Ecological Engineering Group Co., Ltd.

- 6.4.6 Sinochem Holdings Corporation Ltd.

- 6.4.7 Xinyangfeng Agricultural Technology Co., Ltd.

- 6.4.8 Stanley Agriculture Group Co., Ltd.

- 6.4.9 Haifa Group

- 6.4.10 Luxi Chemical Group Co., Ltd.

- 6.4.11 Shikefeng Chemical Industry Co., Ltd.

- 6.4.12 ICL Group Ltd.

- 6.4.13 Zhongchuang Xingyuan Chemical Technology Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR FERTILIZER CEOS