PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066699

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2066699

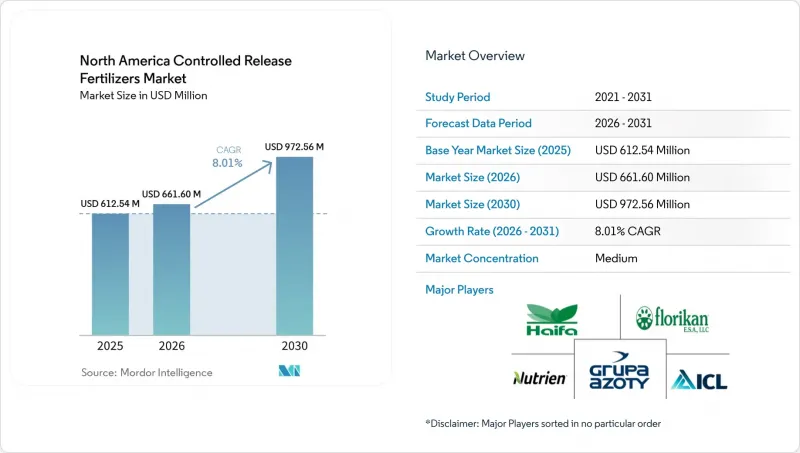

North America Controlled Release Fertilizers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america controlled release fertilizer market size is projected to expand from USD 612.54 million in 2025 and USD 661.60 million in 2026 to USD 972.56 million by 2031, registering a CAGR of 8.01% between 2026 to 2031.

This report is Segmented by Coating Type (Polymer Coated, Polymer-Sulfur Coated, Sulfur Coated, and Other Coated Technologies), Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental), and Geography (Canada, Mexico, United States, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

North America Controlled Release Fertilizers Market Trends and Insights

Precision Agriculture and Fertigation Adoption

The North America controlled release fertilizer market is growing due to the increased use of variable-rate technology and integrated nutrient management practices on commercial farms. In the United States, variable-rate technology is extensively applied to cropland, highlighting that many growers already operate within systems requiring precise nutrient placement. This approach reduces the number of fertilizer applications, thereby lowering field costs. Similarly, Canadian farms have adopted variable-rate input application and are already utilizing slow-release fertilizers, demonstrating a strong technical foundation for the wider adoption of controlled release fertilizers. A single application of controlled release fertilizer can align with zone-based nutrient prescriptions, reducing the need for multiple field passes. With ongoing labor shortages and high equipment ownership costs, the North America controlled release fertilizer market is supported by solutions that enhance operational efficiency while maintaining agronomic effectiveness.

Nutrient-Runoff Compliance Pressure

The North America controlled release fertilizer market is also supported by a more stringent regulatory framework for nutrient runoff and water quality. The United States Environmental Protection Agency has continued to support nutrient-reduction efforts in impaired watersheds. This includes a USD 3.7 million grant package announced for June 2025, aimed at organizations in Michigan and Ohio working within the Western Lake Erie Basin. This type of basin-level support demonstrates how nutrient management is becoming an integral part of broader water-quality action plans, particularly in sensitive or impaired watersheds. Similar policy support exists in Canada, including Quebec programs that support the adoption of polymer-coated urea through sustainable agriculture initiatives. These regulatory and policy developments continue strengthening long-term demand for controlled release fertilizers across North America.

Premium Price Versus Conventional Fertilizers

The clearest commercial barrier in the North America controlled release fertilizer market remains the price premium of coated products over conventional nitrogen materials. That premium reflects both coating cost and the added manufacturing complexity needed to deliver more predictable nutrient release. For large grain farms, especially in lower-margin cropping systems, the decision often depends on whether the product can show a clear multi-season return rather than a one-season saving. A University of Florida Institute of Food and Agricultural Sciences study published in February 2025 identified high material costs as the main barrier to wider field-crop use, even though local cost-share programs can soften the burden in some cases. Until price gaps narrow further, the North America controlled release fertilizer market will continue to expand fastest where nutrient control, compliance, or labor savings are valuable enough to offset the initial cost difference.

Other drivers and restraints analyzed in the detailed report include:

- Field-Crop Nitrogen-Use Efficiency Needs

- Protected Horticulture Expansion

- Dealer And Grower Application-Learning Gap

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polymer-coated formulations held 77.2% market share in 2025, giving them the largest share in the North America controlled release fertilizer market by coating type. That lead reflects broad acceptance across row crops, protected horticulture, and managed turf, where predictable release behavior is valued more than the lowest upfront input cost. The segment has also benefited from long commercial use in corn and turf systems, which has built confidence around application methods and crop response. Mature supply chains and compatibility with standard blending and spreading equipment have further strengthened adoption across the North America controlled release fertilizer industry. This installed base gives polymer-coated products a clear advantage over sulfur-based and niche coating alternatives when growers want consistency at a commercial scale.

Polymer-coated formulations are the fastest-growing coating type, with a CAGR of 8.1% projected from 2026 to 2031, demonstrating that this technology continues to gain traction rather than losing momentum. Pursell Agri-Tech and Wastech Group entered into a joint venture agreement in 2025 to establish a controlled release fertilizer polymer coating facility in Malaysia. The reported capital expenditure for the project exceeded RM80 million (approximately USD18 million). This facility is projected to serve Southeast Asian markets utilizing Pursell's coating technology. Polymer-sulfur coated and sulfur coated products still matter in more cost-sensitive settings because they provide a lower-cost path into enhanced efficiency use. Other coated technologies remain relevant in specialty niches, but they do not yet challenge the scale or growth profile of the polymer coated core within the North America controlled release fertilizer market.

List of Companies Covered in this Report:

- Nutrien Ltd.

- ICL Group Ltd.

- Koch Industries Inc.

- Haifa Group

- Grupa Azoty S.A. (Compo Expert)

- Yara International ASA

- Profile Products LLC

- The Andersons, Inc.

- J.R. Simplot Company

- Pursell Agri-Tech, LLC

- EuroChem Group AG

- New Mountain Capital (Florikan)

- The Scotts Miracle-Gro Company

- Helena Agri-Enterprises, LLC (Marubeni Corporation)

- Timac Agro USA, Inc. (Groupe Roullier)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Key Industry Trends

- 4.1 Acreage of Major Crop Types

- 4.1.1 Field Crops

- 4.1.2 Horticultural Crops

- 4.1.3 Turf and Ornamental

- 4.2 Average Nutrient Application Rates

- 4.2.1 Primary Nutrients

- 4.2.1.1 Field Crops

- 4.2.1.2 Horticultural Crops

- 4.2.1.3 Turf and Ornamental

- 4.2.1 Primary Nutrients

- 4.3 Regulatory Framework

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Precision agriculture and fertigation adoption

- 4.5.2 Nutrient-runoff compliance pressure

- 4.5.3 Field-crop nitrogen-use efficiency needs

- 4.5.4 Protected horticulture expansion

- 4.5.5 United States Department of Agriculture backed domestic capacity build

- 4.5.6 Biodegradable coating innovation

- 4.6 Market Restraints

- 4.6.1 Premium price versus conventional fertilizers

- 4.6.2 Dealer and grower application-learning gap

- 4.6.3 Microplastic scrutiny of polymer shells

- 4.6.4 Highly cyclical raw-material prices

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 Coating Type

- 5.1.1 Polymer Coated

- 5.1.1.1 Polyurethane and resin-coated

- 5.1.1.2 Biodegradable polymer-coated

- 5.1.2 Polymer-Sulfur Coated

- 5.1.3 Sulfur Coated

- 5.1.4 Other Coated Technologies

- 5.1.1 Polymer Coated

- 5.2 Crop Type

- 5.2.1 Field Crops

- 5.2.1.1 Cereals and Grains

- 5.2.1.2 Oilseeds and Pulses

- 5.2.1.3 Cotton and Other Fiber Crops

- 5.2.2 Horticultural Crops

- 5.2.2.1 Fruits

- 5.2.2.2 Vegetables

- 5.2.2.3 Orchard and Vineyard Crops

- 5.2.3 Turf and Ornamental

- 5.2.3.1 Golf and Sports Turf

- 5.2.3.2 Professional Landscaping

- 5.2.3.3 Nursery and Greenhouse Ornamentals

- 5.2.1 Field Crops

- 5.3 Geography

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 Competitive Landscape

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments)

- 6.4.1 Nutrien Ltd.

- 6.4.2 ICL Group Ltd.

- 6.4.3 Koch Industries Inc.

- 6.4.4 Haifa Group

- 6.4.5 Grupa Azoty S.A. (Compo Expert)

- 6.4.6 Yara International ASA

- 6.4.7 Profile Products LLC

- 6.4.8 The Andersons, Inc.

- 6.4.9 J.R. Simplot Company

- 6.4.10 Pursell Agri-Tech, LLC

- 6.4.11 EuroChem Group AG

- 6.4.12 New Mountain Capital (Florikan)

- 6.4.13 The Scotts Miracle-Gro Company

- 6.4.14 Helena Agri-Enterprises, LLC (Marubeni Corporation)

- 6.4.15 Timac Agro USA, Inc. (Groupe Roullier)

7 Market Opportunities and Future Outlook