PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045790

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2045790

Germany Construction Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

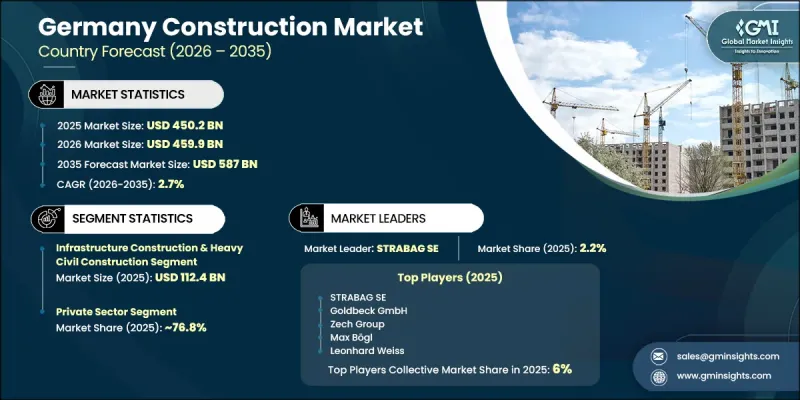

Germany Construction Market was valued at USD 450.2 billion in 2025 and is estimated to grow at a CAGR of 2.7% to reach USD 587 billion by 2035.

The industry is undergoing a structural shift driven by sustainability regulations, energy transition goals, and modernization needs across the built environment. Policy frameworks under the EU Green Deal are increasingly directing capital toward energy-efficient renovation and retrofitting projects rather than purely new construction activity. This shift is reshaping investment priorities across residential, commercial, and institutional buildings, with strong emphasis on reducing emissions, improving insulation standards, and integrating renewable energy systems. Germany's large stock of aging buildings is further reinforcing demand for modernization, as compliance requirements are translating into recurring renovation cycles. As a result, construction companies are benefiting from more stable and predictable project pipelines with reduced exposure to short-term economic volatility. In parallel, digital construction technologies and advanced building materials are gradually improving productivity and project efficiency. The market is also being influenced by shifting financing conditions, demographic pressures, and urban housing shortages, all of which are contributing to a more structurally supported long-term growth trajectory for the sector.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $450.2 Billion |

| Forecast Value | $587 Billion |

| CAGR | 2.7% |

The infrastructure construction and heavy civil engineering segment accounted for USD 112.4 billion in 2025, representing the leading segment of the Germany construction market. This segment continues to expand as governments and private stakeholders prioritize the modernization of critical national assets. Investment focus is increasingly directed toward upgrading transportation networks, strengthening energy systems, and improving water management infrastructure to support economic resilience and climate objectives. Large-scale rehabilitation projects, expansion of rail connectivity, road network improvements, and development of renewable energy-related infrastructure are shaping segment growth, reinforcing its dominant position within overall construction activity.

The private sector held a 76.8% share in 2025. Investment activity from private developers, corporations, and institutional investors is increasingly concentrated in asset classes aligned with long-term structural demand. Strong momentum is observed in logistics infrastructure, healthcare facilities, data centers, and energy-related developments. Compared to public sector projects, private construction activity benefits from faster execution timelines, clearer financial returns, and greater flexibility in project design and capital allocation, making it a key driver of overall market expansion.

Germany Construction Market is led by HOCHTIEF AG, STRABAG SE, ACS Group, ACCIONA S.A., RONESANS Holding, and Vinci Construction Germany (Eurovia), alongside key regional participants such as Max Bogl Firmengruppe, Goldbeck GmbH, Ed. Zublin AG, Wolff & Muller, Bremer SE, Zech Group (Zech Building SE), and Leonhard Weiss. Emerging and specialized firms including PORR Deutschland, Gropyus GmbH, GP Gunter Papenburg AG, Johann Bunte Bauunternehmung SE & Co. KG, Kondor Wessels Deutschland, Heitkamp Ingenieur- und Bruckenbau GmbH, and Weisenburger Bau GmbH are also contributing to competitive market dynamics. Companies in the Germany construction market are adopting several strategic approaches to strengthen their competitive position and secure long-term growth. Leading players are increasing investments in digital construction technologies such as Building Information Modeling and automation tools to enhance project efficiency and cost control. Sustainability-focused construction practices are being prioritized to align with stringent environmental regulations and energy efficiency standards. Firms are also expanding capabilities in renovation and retrofit projects to capture demand driven by the EU Green Deal. Strategic partnerships with technology providers, energy companies, and public authorities are enabling access to large infrastructure projects and integrated development opportunities. In addition, companies are strengthening their financial resilience through diversified project portfolios spanning residential, commercial, and infrastructure segments. Expansion into high-growth areas such as logistics, data infrastructure, and renewable energy facilities is further supporting market positioning and ensuring long-term stability in an evolving construction landscape.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Contracting Type

- 2.2.4 Scale

- 2.2.5 End Use

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Manufacturer/designer tier

- 3.1.3 Distribution & retail layer

- 3.1.4 End-user segment

- 3.1.5 Profit margin analysis by value chain stage

- 3.1.6 Value addition at each stage

- 3.1.7 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis (driven by primary research)

- 3.6.1 Historical price trend analysis

- 3.6.2 Pricing strategy by player type (premium / value / cost-plus)

- 3.7 Regulatory Landscape

- 3.7.1 Building codes & standards

- 3.7.2 Energy efficiency requirements

- 3.7.3 Permit & approval processes

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Trade data analysis - 995411: Construction services for residential buildings (Driven by paid database)

- 3.10.1 Import/Export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Impact of AI & generative AI on the market

- 3.11.1 AI-Driven disruption of existing business models

- 3.11.2 GenAI use cases & adoption roadmap by segment

- 3.11.3 Risks, limitations & regulatory considerations

- 3.12 Service delivery capacity & provider infrastructure (driven by primary research)

- 3.12.1 Provider network density & coverage by region (driven by primary research)

- 3.12.2 Capacity gaps & addressable demand mismatch (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Residential construction

- 5.2.1 Single-family homes

- 5.2.2 Multi-family apartments

- 5.2.3 Social/affordable housing

- 5.3 Commercial construction

- 5.3.1 Hospitality facilities construction

- 5.3.2 Retail facilities construction

- 5.3.3 Office buildings construction

- 5.3.4 Others (sports facilities, entertainment, etc.)

- 5.4 Industrial construction

- 5.4.1 Manufacturing facilities

- 5.4.2 Warehouses & distribution centers

- 5.4.3 Logistics hubs

- 5.5 Infrastructure construction & heavy civil construction

- 5.5.1 Transportation infrastructure

- 5.5.2 Water & wastewater systems

- 5.5.3 Energy infrastructure

- 5.6 Institutional construction

- 5.7 Mixed-use construction

- 5.8 Specialized construction

- 5.8.1 Data Centers

- 5.8.2 Clean Room Facilities

- 5.9 Renovation/remodeling construction

- 5.10 Others (environmental construction, etc.)

Chapter 6 Market Estimates and Forecast, By Contracting Type, 2022 - 2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 General contracting

- 6.3 Design-build contracting

- 6.4 Construction management

Chapter 7 Market Estimates and Forecast, By Scale, 2022 - 2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Mega Project (>€500M)

- 7.3 Major Project (€100M-€500M)

- 7.4 Medium Project (€10M-€100M)

- 7.5 Small Project (<€10M)

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Private sector

- 8.3 Public sector

Chapter 9 Company Profiles

- 9.1 Top Global Construction Companies

- 9.1.1 HOCHTIEF AG

- 9.1.2 STRABAG SE

- 9.1.3 ACS Group

- 9.1.4 ACCIONA S.A.

- 9.1.5 RONESANS Holding

- 9.1.6 Vinci Construction Germany (Eurovia)

- 9.1.7 Implenia

- 9.2 Regional Players

- 9.2.1 Goldbeck GmbH

- 9.2.2 Max Bogl Firmengruppe

- 9.2.3 Ed. Zublin AG

- 9.2.4 Wolff & Muller

- 9.2.5 Zech Group (Zech Building SE)

- 9.2.6 Bremer SE

- 9.2.7 Leonhard Weiss

- 9.3 Emerging Companies

- 9.3.1 PORR Deutschland

- 9.3.2 Johann Bunte Bauunternehmung SE & Co. KG

- 9.3.3 GP Gunter Papenburg AG

- 9.3.4 Heitkamp Ingenieur- und Bruckenbau GmbH

- 9.3.5 Gropyus GmbH

- 9.3.6 Kondor Wessels Deutschland

- 9.3.7 Weisenburger Bau GmbH