PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061925

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061925

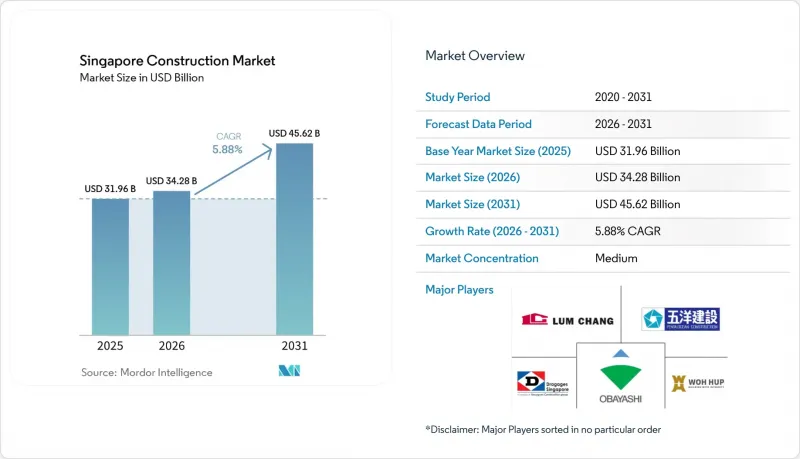

Singapore Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the singapore construction market size was valued at USD 31.96 billion in 2025 and estimated to grow from USD 34.28 billion in 2026 to reach USD 45.62 billion by 2031, at a CAGR of 5.88% during the forecast period (2026-2031).

This report is Segmented by Sector (Residential, Commercial, Infrastructure), by Construction Type (New Construction, Renovation/Retrofit), by Construction Method (Conventional On-Site, Modern Methods of Construction), by Investment Source (Public, Private, PPP), and by Region (Core Central Region (CCR) and More). Market Forecasts are Provided in Terms of Value (USD).

Singapore Construction Market Trends and Insights

Tuas Port and Changi T5 megaprojects anchor the infrastructure pipeline

Tuas Port reclamation is 75% complete and will scale from 11 to 18 berths by 2027 before reaching 65 million TEUs capacity in the 2040s. At the other end of the island, construction on Changi Terminal 5 started in 2025 after USD 3.56 billion in substructure and airside contracts were awarded. Complex marine, tunnelling, and aviation packages are lifting demand for specialist engineering services, robotics, and large-format precast elements. With a combined public investment of around USD 15 billion, these flagship projects secure a decade-plus workload for heavy civil contractors and their supply chains.

Housing Development Board's accelerated BTO programme sustains residential demand

HDB plans to launch 25,000 new flats in 2025, pushing the total 2021-2025 supply above 102,000 units. The programme introduces Standard, Plus, and Prime flat categories that deepen affordability and shorten waiting times, while half of all BTO sites now deploy painting and plastering robots that cut labour hours by 30%. Large suburban sites in Tengah and Mount Pleasant are embedding centralised cooling and solar installations, keeping the Singapore construction market aligned with national climate goals.

Tight foreign-worker quotas constrain labour supply

The dependency ratio ceiling remains at 83.3%, limiting firms to five Work-Permit holders for each local employee, while S-Pass salary minimums rose to USD 2,475 in 2025. Levies will climb to USD 488 by September 2025, and new capital requirements for contractor registration add a further hurdle. These rules inflate total labour costs and encourage heavier reliance on automation, but smaller firms may struggle to fund the transition, risking project delays.

Other drivers and restraints analyzed in the detailed report include:

- Public-sector Green Mark procurement drives sustainable construction standards

- Hyperscale data-centre expansion follows moratorium lift

- Scarce land drives vertical-build complexity and risk

- Scarce Land Drives Vertical Construction Complexity and Project Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential work held 46.62% of the Singapore construction market share in 2025, fuelled by the BTO pipeline and steady private condominium launches. Infrastructure, although smaller, is set to record the fastest 5.72% CAGR to 2031, reflecting long-cycle port, rail and airport expansions.

Rising population density sustains apartment demand, while energy-efficient designs and prefab components help developers meet Green Mark targets. On the infrastructure side, Phase 2 of the Cross Island Line began in 2025, and Tuas Port's next berth tranche requires heavy caisson fabrication. The Singapore construction market size tied to transport corridors will therefore outpace other segments as the nation reinforces its role as a trans-shipment and aviation hub.

New builds made up 62.35% of 2025 output, underpinned by greenfield housing and megaprojects. Renovation earns the top growth slot at a 5.83% CAGR as mature estates enter cyclical upgrade programmes.

CORENET X digital approvals shorten design cycles for new towers, but brownfield retrofits enjoy tailwinds from mandated energy improvements and universal-design upgrades. As many commercial offices head for repositioning to retain tenants, capital spending shifts towards facade recladding, low-energy HVAC, and structural strengthening. These trends enlarge the Singapore construction market size for fit-out and M&E contractors through 2031.

List of Companies Covered in this Report:

- Woh Hup (Private) Ltd.

- Obayashi Singapore Pte. Ltd.

- Dragages Singapore Pte. Ltd.

- Penta-Ocean Construction Co., Ltd. (Singapore)

- Lum Chang Building Contractors Pte. Ltd.

- Tiong Seng Contractors (Pte.) Ltd.

- Gammon Pte. Ltd.

- Samsung C&T Corp. (Singapore)

- Lendlease Singapore Pte. Ltd.

- Kajima Overseas Asia Pte. Ltd.

- China Construction (South Pacific) Dev. Co. Pte. Ltd.

- Ssangyong Engineering & Construction Co., Ltd. (Singapore)

- Hock Lian Seng Infrastructure Ltd.

- Koon Construction & Transport Co. Pte. Ltd.

- Straits Construction Singapore Pte. Ltd.

- Takenaka Corp. (Singapore Office)

- Civil Tech Pte. Ltd.

- BHCC Construction Pte. Ltd.

- United Engineers Ltd.

- Chip Eng Seng Contractors (1988) Pte. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Public-sector "Green Mark" procurement linked to embodied-carbon thresholds

- 4.2.2 Tuas Port & Changi T5 megaprojects anchoring civil-infrastructure pipeline

- 4.2.3 Housing Development Board's accelerated BTO programme

- 4.2.4 Hyperscale-data-centre moratorium lift triggering new permits

- 4.2.5 Mandatory Integrated Digital Delivery (IDD) raising BIM-prefab adoption

- 4.2.6 Neighbourhood-Renewal Programme boosting brownfield retrofits

- 4.3 Market Restraints

- 4.3.1 Tight foreign-worker quotas inflating labour costs

- 4.3.2 Scarce land driving vertical-construction complexity & risk

- 4.3.3 Volatile imported-material prices (re-export hub exposure)

- 4.3.4 Rising workplace-safety compliance penalties

- 4.4 Value / Supply-Chain Analysis

- 4.4.1 Overview

- 4.4.2 Developers & Main Contractors - key quantitative & qualitative insights

- 4.4.3 Architectural & Engineering Firms - key quantitative & qualitative insights

- 4.4.4 Building-Material & Equipment Suppliers - key quantitative & qualitative insights

- 4.5 Government Initiatives & Vision

- 4.6 Regulatory Outlook

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing (Construction Materials) & Construction Cost Analysis

- 4.10 Comparison of Key Industry Metrics of Singapore with Other Countries

- 4.11 Key Upcoming/Ongoing Projects (focus on mega projects)

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Sector

- 5.1.1 Residential

- 5.1.1.1 Apartments / Condominiums

- 5.1.1.2 Villas and Landed Houses

- 5.1.2 Commercial

- 5.1.2.1 Office

- 5.1.2.2 Retail

- 5.1.2.3 Industrial and Logistics

- 5.1.2.4 Others

- 5.1.3 Infrastructure

- 5.1.3.1 Transportation Infrastructure (Roadways, Railways, Airways, others)

- 5.1.3.2 Energy & Utilities

- 5.1.3.3 Others

- 5.1.1 Residential

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Renovation / Retrofit

- 5.3 By Construction Method

- 5.3.1 Conventional On-Site

- 5.3.2 Modern Methods of Construction

- 5.4 By Investment Source

- 5.4.1 Public

- 5.4.2 Private

- 5.4.3 Public-Private Partnership (PPP)

- 5.5 By Region

- 5.5.1 Core Central Region (CCR)

- 5.5.2 Rest of Central Region (RCR)

- 5.5.3 Outside Central Region (OCR)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Woh Hup (Private) Ltd.

- 6.4.2 Obayashi Singapore Pte. Ltd.

- 6.4.3 Dragages Singapore Pte. Ltd.

- 6.4.4 Penta-Ocean Construction Co., Ltd. (Singapore)

- 6.4.5 Lum Chang Building Contractors Pte. Ltd.

- 6.4.6 Tiong Seng Contractors (Pte.) Ltd.

- 6.4.7 Gammon Pte. Ltd.

- 6.4.8 Samsung C&T Corp. (Singapore)

- 6.4.9 Lendlease Singapore Pte. Ltd.

- 6.4.10 Kajima Overseas Asia Pte. Ltd.

- 6.4.11 China Construction (South Pacific) Dev. Co. Pte. Ltd.

- 6.4.12 Ssangyong Engineering & Construction Co., Ltd. (Singapore)

- 6.4.13 Hock Lian Seng Infrastructure Ltd.

- 6.4.14 Koon Construction & Transport Co. Pte. Ltd.

- 6.4.15 Straits Construction Singapore Pte. Ltd.

- 6.4.16 Takenaka Corp. (Singapore Office)

- 6.4.17 Civil Tech Pte. Ltd.

- 6.4.18 BHCC Construction Pte. Ltd.

- 6.4.19 United Engineers Ltd.

- 6.4.20 Chip Eng Seng Contractors (1988) Pte. Ltd.

7 Market Opportunities & Future Outlook