PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083333

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2083333

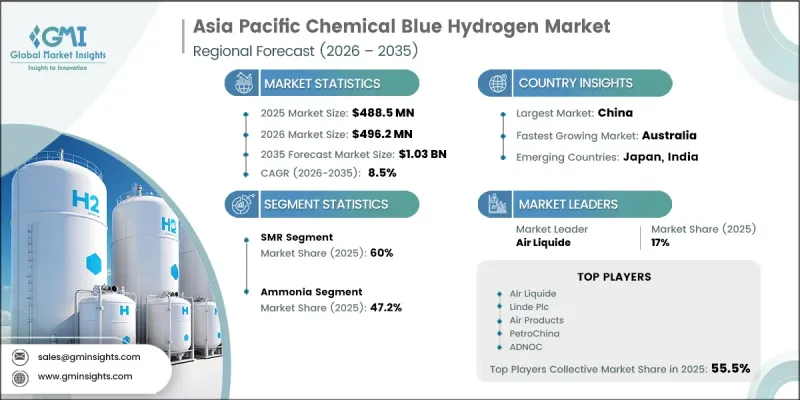

Asia Pacific Chemical Blue Hydrogen Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

Asia Pacific Chemical Blue Hydrogen Market was valued at USD 488.5 million in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 1.03 billion by 2035.

The market is witnessing steady growth as chemical manufacturers across the region accelerate efforts to lower carbon emissions and transition toward cleaner production pathways. Blue hydrogen is increasingly being adopted as a lower-emission alternative to conventional hydrogen sources, supporting sustainability initiatives throughout the chemical value chain. Rising demand from chemical processing applications is creating significant opportunities for market expansion, particularly as industries seek practical solutions to achieve decarbonization targets while maintaining operational efficiency. Continued investments in carbon capture and storage (CCS) infrastructure are strengthening the foundation for large-scale blue hydrogen production, enabling broader commercial deployment across the region. Government support through favorable policy frameworks, industrial decarbonization programs, financial incentives, and emission reduction strategies is further contributing to market development. In addition, growing global demand for lower-carbon chemical products is encouraging manufacturers to incorporate cleaner feedstocks into their production processes. As environmental performance becomes an increasingly important purchasing consideration, blue hydrogen is emerging as a strategic component of long-term sustainability plans within the chemical industry across Asia Pacific.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $488.5 Million |

| Forecast Value | $1.03 Billion |

| CAGR | 8.5% |

The steam methane reforming (SMR) segment held 60% share in 2025. Its dominant position is supported by the availability of natural gas resources across several regional markets, providing a dependable and economically viable feedstock for hydrogen generation. SMR continues to be widely utilized due to its proven scalability, operational reliability, and conversion efficiency, which typically ranges between 70% and 80%. These advantages make it a preferred technology for producing large volumes of blue hydrogen while supporting industrial decarbonization efforts.

The ammonia segment held a 47.2% share in 2025 and is forecast to grow at a CAGR of 10.6% from 2026 to 2035. Growing emphasis on reducing emissions associated with chemical and fertilizer production is encouraging greater integration of blue hydrogen into ammonia manufacturing processes. Since ammonia production requires significant hydrogen consumption, the adoption of blue hydrogen enables producers to lower carbon intensity while maintaining production efficiency and supporting broader sustainability objectives.

China Chemical Blue Hydrogen Market held a 60.9% share in 2025. Increasing commitment to carbon reduction goals and industrial sustainability initiatives is accelerating the adoption of blue hydrogen across key chemical sectors. Strong policy support, evolving emission reduction strategies, and growing demand for cleaner industrial inputs are encouraging chemical producers to incorporate low-carbon hydrogen solutions into their operations, driving long-term market growth.

Leading companies operating in the Asia Pacific chemical blue hydrogen market include Reliance Industries, Exxon Mobil Corporation, Air Products, PetroChina, INPEX Corporation, Sembcorp Industries, Woodside Energy, JERA, Indian Oil Corporation, Air Liquide, SK E&S, ADNOC, Mitsubishi Corporation, Bharat Petroleum Corporation, PTT Global Chemical, ENN Group, Petronas, ITOCHU Corporation, Idemitsu Kosan, and Linde plc. Companies active in the Asia Pacific chemical blue hydrogen market are pursuing a variety of strategies to strengthen their competitive position and expand their regional presence. Major participants are investing heavily in carbon capture and storage infrastructure, hydrogen production facilities, and integrated supply chain networks to improve operational efficiency and support large-scale deployment. Strategic collaborations, joint ventures, and long-term supply agreements are becoming increasingly common as companies seek to accelerate commercialization and secure reliable market access.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Technology trends

- 2.4 Application trends

- 2.5 Country trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.2.1 China

- 3.2.2 Japan

- 3.2.3 India

- 3.2.4 Australia

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of chemical blue hydrogen

- 3.8 Price trend analysis (Driven by Primary Research)

- 3.8.1 By technology USD/Ton (Driven by Primary Research)

- 3.8.2 Pricing strategy by player type (Premium / Value / Cost-plus) (Driven by Primary Research)

- 3.9 Impact of AI & generative AI on the market

- 3.9.1 Predictive maintenance & fault detection

- 3.9.2 Grid optimization & load forecasting

- 3.9.3 Digital twin simulation & testing

- 3.9.4 Risks, limitations & regulatory considerations

- 3.10 Emerging opportunities & trends

- 3.10.1 Digitalization & IoT integration

- 3.10.2 Emerging market penetration

- 3.11 Overall investment scenario and future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by country, 2025

- 4.2.1 China

- 4.2.2 Japan

- 4.2.3 India

- 4.2.4 Australia

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans & funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & MT)

- 5.1 Key trends

- 5.2 Steam methane reforming

- 5.3 Autothermal reforming

- 5.4 Partial oxidation

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & MT)

- 6.1 Key trends

- 6.2 Ammonia

- 6.3 Methanol

- 6.4 Refining chemicals

- 6.5 Others

Chapter 7 Market Size and Forecast, By Country, 2022 - 2035 (USD Million & MT)

- 7.1 Key trends

- 7.2 China

- 7.3 Japan

- 7.4 India

- 7.5 Australia

Chapter 8 Company Profiles

- 8.1 ADNOC

- 8.2 Air Liquide

- 8.3 Air Products

- 8.4 Bharat Petroleum Corporation

- 8.5 ENN Group

- 8.6 Exxon Mobil Corporation

- 8.7 Idemitsu kosan

- 8.8 Indian Oil Corporation

- 8.9 INPEX Corporation

- 8.10 ITOCHU Corporation

- 8.11 JERA

- 8.12 Linde plc

- 8.13 Mitsubishi Corporation

- 8.14 PetroChina

- 8.15 Petronas

- 8.16 PTT Global Chemical

- 8.17 Reliance Industries

- 8.18 Sembcorp Industries

- 8.19 SK E&S

- 8.20 Woodside Energy