PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1642090

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1642090

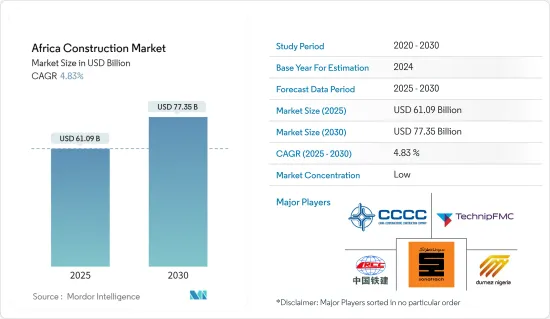

Africa Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Africa Construction Market size is estimated at USD 61.09 billion in 2025, and is expected to reach USD 77.35 billion by 2030, at a CAGR of 4.83% during the forecast period (2025-2030).

Key Highlights

- Despite near-term challenges, the medium- to long-term outlook remains positive. Over the short term, investments in the construction industry may be driven by government spending in the infrastructure sector.

- The African construction industry is the target destination for most large economies because of several benefits, such as the availability of natural resources, tremendous investment opportunities in energy and infrastructure, cheap labor, and a fast-growing consumer market.

- The country also has a beneficial business environment that includes favorable economic development policies, rising commodity prices, continued progress in the fight against corruption, and the adoption of democratic governments.

- Given its stable political environment and business-friendly policies, Ghana has a reputation as an attractive investment destination with a wide range of opportunities. The government has made substantial investments in infrastructure development over the last few years, leading to rapid growth of the construction industry and creating opportunities for investors and businesses.

- Several policies have been implemented by the Ghanaian government, such as Agenda 111's "One District, One Factory" and Agenda 111 Hospital Projects, which are attracting local and international investors to create several construction firms.

- To close the financing gap for public infrastructure, which is projected to be USD 140 billion by 2040, public-private partnerships and blended project financing to finance infrastructure construction are firmly focused on the goals of NIP 2050.

- There are over 570 construction projects estimated to be worth USD 450 billion in Africa. The second-largest African sector, after the energy sector, is the transport sector, which includes road, airport, and rail projects totaling more than USD 280 billion.

Africa Construction Market Trends

Infrastructure Construction Projects Driving the Market

African cities are changing with several significant projects, ranging from magnificent skyscrapers to megacities built from scratch. These multimillion-dollar construction projects in Africa are giving its cities a much-needed transformation.

Developing infrastructure has been a focus of many governments to meet the needs and requirements of a growing population, making construction the largest sector in Africa. There are over 570 construction projects in Africa worth USD 450 billion. The energy sector has projects worth over USD 370 billion, followed by the transportation sector, with projects that include roads, airports, and railways worth USD 280 billion.

Egypt leads the African market with over 300 active projects worth USD 338 billion. With active projects worth around USD 207 billion, South Africa comes second, followed by Nigeria, which has ongoing and upcoming projects worth USD 200 billion.

Nigerian refineries are dismal, leaving one of Africa's biggest crude oil producers dependent on petroleum imports. However, Dangote is changing that narrative with an indigenous refinery capable of processing 650,000 barrels daily, making it the largest single-train refinery in the world. The refinery spans 2,635 hectares in the Lekki Free Trade Zone, Lekki, Lagos State. It is said to cost more than USD 12 billion.

Konza Technopolis is Kenya's smart city project, a few kilometers from Nairobi. The Kenyan government has allocated 2,000 hectares of land for the project. The city is part of the government's vision for 2030 and may serve as the central hub for technology, science, telecom, and education. The estimated cost of this smart city is USD 14.5 billion, and it may generate about 20,000 jobs when completed. The first phase of the project's horizontal infrastructure works was wrapped up in 2022.

Northern Africa Dominating the Market

North African countries such as Egypt and Morocco have seen significant construction growth driven by large-scale infrastructure projects, tourism development, and urbanization.

The Egyptian government has made significant investments in the building industry. Additionally, the government is modernizing transportation systems, ports, and airports. The Ministry of Transportation is currently working on about 25 projects related to the railroad industry. The development of roads and providing enough transit between cities are the government's primary priorities.

Egypt has revealed plans to build a high-speed train connecting the entire nation. As the prime contractor, Siemens was given a contract for this project worth USD 8.7 billion. According to the country's plans, up to 14 new smart towns could be built in Egypt. The Ministry of Housing claims that in less than two years, Egypt finished infrastructure projects valued at about EGP 1.7 trillion (about USD 106.25 billion).

The New Urban Communities Authority (NUCA) intends to construct more cities with integrated educational, medical, retail, and leisure services. This organization is in charge of creating these new cities and tying them to existing infrastructure.

Morocco's National Investment Committee approved 17 projects with a total budget of MAD 76.7 billion (USD 7.4 billion) in May 2023. In January 2023, the Moroccan government approved 26 projects with an investment of MAD 28.5 billion (USD 2.7 billion) for five years.

According to Morocco's Energy Transition and Sustainable Development Ministry, in July 2023, the Kingdom of Morocco was to allocate MAD 55 billion (USD 5.3 billion) during the next four years with a view to improving its national economy through cost-effectiveness and clean energy until 2027.

Africa Construction Industry Overview

The African construction market is less competitive, with major international players holding large market shares. The African construction market presents growth potential during the forecast period, which is expected to boost market competition. With a few players holding a significant share, the market has an observable level of consolidation. The major players are Vinci, Bouygues, TechnipFMC, China Communications Construction Group Ltd, and China Railway Construction Corp. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS AND DYNAMICS

- 4.1 Current Economic and Construction Market Scenarios

- 4.2 Technological Innovations in the Construction Industry

- 4.3 Impact of Government Regulations and Initiatives on the Industry

- 4.4 Review and Commentary on the Impact of International Construction Market and Growth Potential for the Industry in Major African Economies

- 4.5 Review and Commentary on Chinese Infrastructure Projects and the BRI Initiative

- 4.6 Comparison of Key Industry Metrics of African Countries (Analyst View)

- 4.7 Comparison of Construction Cost Metrics of African Countries (Analyst View)

- 4.8 Impact of COVID-19 on the Market

- 4.9 Market Dynamics

- 4.9.1 Drivers

- 4.9.1.1 Rapid Urbanization Driving the Market

- 4.9.1.2 Economic Development

- 4.9.2 Restraints

- 4.9.2.1 Political and Regulatory Challenges

- 4.9.2.2 Skills and Labor Shortages

- 4.9.3 Opportunities

- 4.9.3.1 Affordable Housing

- 4.9.3.2 Renewable Energy

- 4.9.1 Drivers

- 4.10 Industry Attractiveness - Porter's Five Forces Analysis

- 4.10.1 Bargaining Power of Suppliers

- 4.10.2 Bargaining Power of Buyers/Consumers

- 4.10.3 Threat of New Entrants

- 4.10.4 Threat of Substitute Products

- 4.10.5 Intensity of Competitive Rivalry

- 4.11 Industry Value Chain Analysis

5 MARKET SEGMENTATION

- 5.1 By Sector

- 5.1.1 Commercial Construction

- 5.1.2 Residential Construction

- 5.1.3 Industrial Construction

- 5.1.4 Infrastructure (Transportation) Construction

- 5.1.5 Energy and Utilities Construction

- 5.2 By Construction Type

- 5.2.1 Additions

- 5.2.2 Demolition

- 5.2.3 New Constructions

- 5.3 By Region

- 5.3.1 Eastern Africa

- 5.3.2 Western Africa

- 5.3.3 Southern Africa

- 5.3.4 Northern Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 China Communications Construction Group Ltd

- 6.2.2 China Railway Construction Corp. Ltd

- 6.2.3 Sikhumba Construction (Pty) Ltd

- 6.2.4 Sonatrach

- 6.2.5 Dumez Nigeria PLC

- 6.2.6 General Nile Company For Roads & Bridges

- 6.2.7 China National Machinery Industry Corp.

- 6.2.8 TechnipFMC

- 6.2.9 Vinci

- 6.2.10 Bouygues*

- 6.3 Other Companies

7 FUTURE OF THE MARKET

8 APPENDIX