Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693474

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1693474

Africa Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 448 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

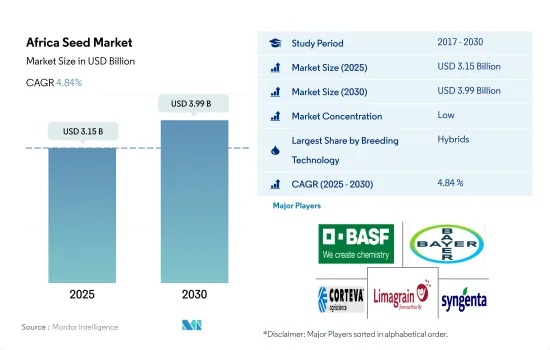

The Africa Seed Market size is estimated at 3.15 billion USD in 2025, and is expected to reach 3.99 billion USD by 2030, growing at a CAGR of 4.84% during the forecast period (2025-2030).

Hybrids dominated the African seed market due to high yield and pest-resistance characteristics

- In 2022, hybrids had a higher share in the African seed market, accounted for 60.2% of the market. The high share of hybrids is due to the high yield and pest resistance.

- Non-transgenic hybrids accounted for 34.2% of the total seed market value in 2022. The non-transgenic hybrids' share increased by 3.4% in 2022 from the previous year.

- GMOs are gradually becoming a part of modern agriculture in Africa. Only 5 of 47 countries have approved the cultivation of GMO crops, including South Africa, Burkina Faso, Sudan, Egypt, and Nigeria.

- In an overall transgenic hybrid, herbicide-tolerant accounted for 42.7% of the African seed market in 2022. South Africa is the only country that allows herbicide-tolerant varieties. Soybean dominated the herbicide-tolerant transgenic seed market in South Africa, with a market share of 71.3% in terms of value, followed by corn (27.1%) and cotton (1.6%). In Africa, the area under herbicide tolerance was 297,607 hectares in 2022.

- In Africa, insect-resistant transgenic hybrids dominated the transgenic seed market by holding 57.3% of the market share value in 2022. South Africa had the largest insect-resistant transgenic seed market, with a market share of 92.1%, followed by Egypt with 6.8% in 2022.

- In 2022, out of the total seed market in Africa, the open-pollinated varieties and hybrid derivatives seed market accounted for 39.8% in terms of value. The area under open-pollinated varieties and hybrid derivatives in Africa was 30 million hectares in 2022, an increase of 8.1% since 2017 because of the low cost and usage of seeds for the next season. Moreover, the region has a high number of small-scale farmers, they mainly depend on local seeds such as OPVs for farming. Therefore, the demand for OPV's seeds is projected to increase in coming years.

Nigeria dominates the African seed market due to a high level of technological adoption and large cultivation land.

- In 2022, the seed market of Africa reached USD 2.81 billion. The surge in the adoption of innovative technologies is a significant driver in this segment. Row crops hold a dominant position in Africa's seed market. It accounted for 78.0% of the market value, primarily due to the extensive cultivation area and high consumption of these crops.

- Nigeria held a major market share of 40.7% in Africa's seed market in 2022 because the country has a high level of technological adoption in agriculture. This includes precision farming techniques, the use of genetically modified crops, and advanced irrigation systems. Therefore, it is anticipated that the seed market value will grow during the forecast period, registering a CAGR of 4.9%.

- South Africa accounted for the second largest share in the African seed market, with a value of USD 772.2 million in 2022. This was because row crops such as corn, wheat, sorghum, and other row crops are highly grown due to high consumption and demand from processing industries.

- The area under cultivation increased by 7.3% between 2017 and 2022, reaching 275.2 million hectares. This growth was driven by favorable climate conditions, such as adequate rainfall or improved soil fertility, which encouraged the expansion of agricultural land in the region.

- In Africa, the protected cultivation segment had a share value of less than 0.01% of the total seed market in 2022 due to less government support for setting up new greenhouse structures, lack of technical support and skills, and limited access to investment funding is a major obstacle to the adoption of protected cultivation techniques by African growers.

- The rise in cultivation land and growth in adopting innovative technologies are estimated to drive the African seed market during the forecast period.

Africa Seed Market Trends

Grains and cereals dominated the row crops segment, with corn as the major contributor driven by high demand from processing industry

- In Africa, row crops dominated the acreage under cultivation, accounting for more than 81.3% of the cultivated area, i.e., 275.2 million hectares in 2022. The major row crops cultivated in the region are corn, oilseeds, sorghum, and rice. In 2022, corn held a major share of 19.2% in the row crops segment. Additionally, the area under row crops increased by 6.3% between 2017 and 2022 due to an increase in the region's corn and soybean demand. Corn is the region's main food source for over 300 million people. Sorghum is one of the major row crops cultivated in the region. The cultivation area of sorghum decreased in Africa from 29 million ha in 2017 to 27.4 million ha in 2022. Producers preferred to plant more profitable crops, like corn and oilseed.

- Nigeria was the major country cultivating different field crops such as grains, cereals, and oilseeds. It accounted for 14.3% of the region's area used to cultivate row crops in 2022. The higher area under row crops is due to the increased demand from processing industries and the higher consumption demand of grains and cereals in the country. Furthermore, corn was the major crop cultivated in the country. It accounted for 19.9% of the country's area under row crops in 2022. There was a 10% increase in the cultivated area for corn between 2020 and 2022 as it is one of the most consumed crops globally due to an increase in the demand from corn-based oil-generating industries.

- The higher demand for grains and cereals as staple crops and increased demand for bio-fuel generation in the global market is increasing the area of cultivation for field crops during the forecast period.

Disease resistance is a highly preferred trait in cabbage and peas cultivation because it can combat prevalent diseases such as black rot in cabbages and floral diseases in peas

- Cabbage is one of Africa's most widely cultivated exotic leafy vegetables. The demand from restaurants for fresh salads, soups, sautees, and typical summer vegetables drives the demand for cabbage. Farmers cultivate cabbage using high-quality seeds with multiple desirable traits due to the growing demand for high-quality foods.

- Seed varieties with traits such as uniformity in head size, foliage color, adaptability to different growing conditions, early maturity, and disease tolerance are boosting the market's growth due to higher preference by the growers in the region. In cabbage, black rot is the major disease in the region caused by Xanthomonas campestris PV. Campestris (XCC) results in 10-50% yield losses. Major players in the market, such as Bayer AG, BASF SE, Sakata Seeds Corporation, and Syngenta Group, offer cultivars that resist diseases, including black rot, mildews, and other leaf diseases, along with higher productivity. These seed varieties are witnessing high demand to prevent crop losses.

- Peas are an important crop in many parts of the African region. Farmers cultivate pea seeds that resist fungal, viral, and nematode infections. These seeds are also known for their wider adaptability to different growing conditions, especially stressful conditions. They possess high peas per pod and desirable pod shape and size.

- Therefore, introducing new seed varieties with traits such as disease resistance, wider adaptability, etc., along with high yield, is projected to boost the growth of the seed market during the forecast period.

Africa Seed Industry Overview

The Africa Seed Market is fragmented, with the top five companies occupying 20.42%. The major players in this market are BASF SE, Bayer AG, Corteva Agriscience, Groupe Limagrain and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92537

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.1.2 Vegetables

- 4.2 Most Popular Traits

- 4.2.1 Cabbage & Peas

- 4.2.2 Corn & Wheat

- 4.2.3 Sorghum & Soybean

- 4.2.4 Tomato & Chilli

- 4.3 Breeding Techniques

- 4.3.1 Row Crops & Vegetables

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Herbicide Tolerant Hybrids

- 5.1.1.2.2 Insect Resistant Hybrids

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Cultivation Mechanism

- 5.2.1 Open Field

- 5.2.2 Protected Cultivation

- 5.3 Crop Type

- 5.3.1 Row Crops

- 5.3.1.1 Fiber Crops

- 5.3.1.1.1 Cotton

- 5.3.1.1.2 Other Fiber Crops

- 5.3.1.2 Forage Crops

- 5.3.1.2.1 Alfalfa

- 5.3.1.2.2 Forage Corn

- 5.3.1.2.3 Forage Sorghum

- 5.3.1.2.4 Other Forage Crops

- 5.3.1.3 Grains & Cereals

- 5.3.1.3.1 Corn

- 5.3.1.3.2 Rice

- 5.3.1.3.3 Sorghum

- 5.3.1.3.4 Wheat

- 5.3.1.3.5 Other Grains & Cereals

- 5.3.1.4 Oilseeds

- 5.3.1.4.1 Canola, Rapeseed & Mustard

- 5.3.1.4.2 Soybean

- 5.3.1.4.3 Sunflower

- 5.3.1.4.4 Other Oilseeds

- 5.3.1.5 Pulses

- 5.3.2 Vegetables

- 5.3.2.1 Brassicas

- 5.3.2.1.1 Cabbage

- 5.3.2.1.2 Carrot

- 5.3.2.1.3 Cauliflower & Broccoli

- 5.3.2.1.4 Other Brassicas

- 5.3.2.2 Cucurbits

- 5.3.2.2.1 Cucumber & Gherkin

- 5.3.2.2.2 Pumpkin & Squash

- 5.3.2.2.3 Other Cucurbits

- 5.3.2.3 Roots & Bulbs

- 5.3.2.3.1 Garlic

- 5.3.2.3.2 Onion

- 5.3.2.3.3 Potato

- 5.3.2.3.4 Other Roots & Bulbs

- 5.3.2.4 Solanaceae

- 5.3.2.4.1 Chilli

- 5.3.2.4.2 Eggplant

- 5.3.2.4.3 Tomato

- 5.3.2.4.4 Other Solanaceae

- 5.3.2.5 Unclassified Vegetables

- 5.3.2.5.1 Asparagus

- 5.3.2.5.2 Lettuce

- 5.3.2.5.3 Okra

- 5.3.2.5.4 Peas

- 5.3.2.5.5 Spinach

- 5.3.2.5.6 Other Unclassified Vegetables

- 5.3.1 Row Crops

- 5.4 Country

- 5.4.1 Egypt

- 5.4.2 Ethiopia

- 5.4.3 Ghana

- 5.4.4 Kenya

- 5.4.5 Nigeria

- 5.4.6 South Africa

- 5.4.7 Tanzania

- 5.4.8 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 Enza Zaden

- 6.4.6 Groupe Limagrain

- 6.4.7 Rijk Zwaan Zaadteelt en Zaadhandel B.V.

- 6.4.8 Sakata Seeds Corporation

- 6.4.9 Syngenta Group

- 6.4.10 Takii and Co.,Ltd.

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.