Need help finding what you are looking for?

Contact Us

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692550

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1692550

India Seed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

PUBLISHED:

PAGES: 490 Pages

DELIVERY TIME: 2-3 business days

SELECT AN OPTION

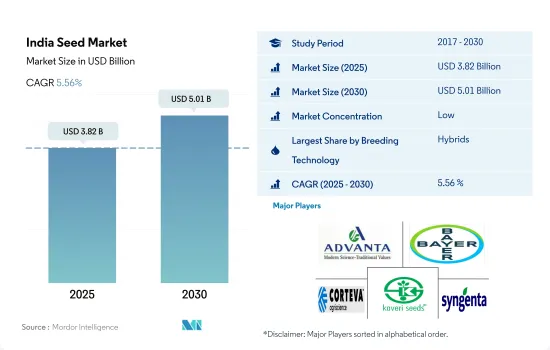

The India Seed Market size is estimated at 3.82 billion USD in 2025, and is expected to reach 5.01 billion USD by 2030, growing at a CAGR of 5.56% during the forecast period (2025-2030).

Hybrids dominate the seed market in the country with the increase in the concerns for higher yield

- In India, hybrids dominated over open-pollinated varieties, accounting for USD 2.3 billion in 2022. Farmers are adopting and using more hybrid seeds, considering the pest-resistant properties of these seeds that reduce the losses and cost of production.

- The per capita availability of arable land decreasing to 0.11 ha in 2020 from 0.12 ha in 2016 is considered a driver for India's commercial seed industry.

- In 2022, hybrid seed usage increased in the country by adopting transgenic cotton hybrids, single-cross corn hybrids, oil-rich oilseed hybrids, and hybrid vegetables. This increased demand for hybrid seeds has boosted the market for commercial seeds. This trend has encouraged farmers to shift their focus from conventional seed sources to packaged seeds that promise better yields.

- In commercial seed cultivation acreage in 2022, hybrids alone accounted for 80.6% of the area, whereas OPVs accounted for 19.4% in India. Therefore, the seed market is estimated to increase as hybrid usage grows in the country.

- The major breeding techniques include selecting plants based on natural variants, hybridizing, and choosing specific genes or marker profiles using molecular tools. The main objective of these techniques is the selection of better plant types among variants in terms of yield, quality, and pest resistance.

- The scenario post-adoption of hybrids and improved OPVs has resulted in many advantages, such as yield improvement, ensuring higher prices, and availability of seeds at an affordable price. These factors will drive the growth of the Indian seed market in the forecast period.

India Seed Market Trends

Rice is highly cultivated in India among row crops, primarily because of the favorable conditions for its cultivation and the consistent market demand

- India is geographically diverse, with various climates and different soil types. This diversity allows for cultivating various row crops throughout the year. As a result, the area under row crops reached 179.2 million in 2022, which increased by 2.7% between 2017 and 2022. This growth is associated with the introduction of modern agricultural technologies, including improved seed varieties and mechanized equipment, making it more feasible for farmers to cultivate row crops.

- Rice accounted for the major share of 25.8% of the Indian row crop acreage in 2022. This is because the country's diverse agro-climatic zones provide favorable conditions for rice cultivation. Additionally, the stability of the rice market, combined with its consistent demand, makes it an attractive option for many Indian farmers. As a result, the acreage for rice is estimated to reach 51.6 million ha in 2030.

- Wheat accounted for the second largest acreage in India, with a share of 17.0% of the overall country's row crop cultivation area in 2022. This is because wheat is a staple food for many Indian populations, and The Indian government supports wheat cultivation through policies such as minimum support prices (MSPs) and procurement programs, which in turn drive the cultivation of wheat.

- In 2022, Uttar Pradesh and Madhya Pradesh accounted for India's major cultivation land for grains and cereals, with a share of 17.2% (17.1 million ha) and 10.6% (10.5 million ha). This is because both states have the largest geographical area in India and have fertile soils, which are highly suitable for cereal and grain cultivation. The favorable government policies and stable demand for row crops in the domestic market are estimated to drive the acreage in the country.

Susceptibility to various diseases and demands for high-quality crop produce are driving the usage of cabbage and onion varieties with resistance to diseases, wider adaptability, and quality attributes

- Cabbage is widely cultivated in the country. The demand for high-value products is growing both in domestic and international markets. Popular traits available in the country are head weight, foliage color, adaptability to wide seasons (as cabbage is cold-specific), early maturity, and disease tolerance to foliar diseases. The size of heads and head weight are the major traits that have a significant demand, as they help increase yield productivity per hectare. Companies such as Syngenta AG and Bayer AG provide seeds with these traits to grow with high quality in adverse weather conditions.

- Onion is one of the major vegetable crops cultivated in the country. Globally, Indian onions are famous for pungency. Major traits such as disease tolerance, long shelf-life (helps in avoiding decay losses during long storage and long-distance transports), uniform size, the color of the onions (red, yellow, and white), tolerance to pest attacks, especially thrips, and early maturing varieties are promoting onion cultivation in the country. The major seed companies, such as Bayer AG, BASF SE, and Bejo Zaden BV, are developing varieties focusing on high yields, attractive colors, and winter adaptability traits. Varieties with disease resistance to purple blotch and downy mildew are widely cultivated, as they cause yield loss of 20%-60%. For instance, in 2021, Bejo and De Groot en Slot launched the first Downy-resistant shallot from seed named Innovator.

- High-quality crops with high disease resistance, increased shelf life, and product innovations with quality attribute traits are helping to increase the demand for these seeds during the forecast period.

India Seed Industry Overview

The India Seed Market is fragmented, with the top five companies occupying 28.95%. The major players in this market are Advanta Seeds - UPL, Bayer AG, Corteva Agriscience, Kaveri Seeds and Syngenta Group (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

Product Code: 92367

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Cultivation

- 4.1.1 Row Crops

- 4.1.2 Vegetables

- 4.2 Most Popular Traits

- 4.2.1 Cabbage & Onion

- 4.2.2 Rice & Corn

- 4.2.3 Tomato & Chilli

- 4.2.4 Wheat & Cotton

- 4.3 Breeding Techniques

- 4.3.1 Row Crops & Vegetables

- 4.4 Regulatory Framework

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Breeding Technology

- 5.1.1 Hybrids

- 5.1.1.1 Non-Transgenic Hybrids

- 5.1.1.2 Transgenic Hybrids

- 5.1.1.2.1 Insect Resistant Hybrids

- 5.1.2 Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1 Hybrids

- 5.2 Cultivation Mechanism

- 5.2.1 Open Field

- 5.2.2 Protected Cultivation

- 5.3 Crop Type

- 5.3.1 Row Crops

- 5.3.1.1 Fiber Crops

- 5.3.1.1.1 Cotton

- 5.3.1.1.2 Other Fiber Crops

- 5.3.1.2 Forage Crops

- 5.3.1.2.1 Alfalfa

- 5.3.1.2.2 Forage Corn

- 5.3.1.2.3 Forage Sorghum

- 5.3.1.2.4 Other Forage Crops

- 5.3.1.3 Grains & Cereals

- 5.3.1.3.1 Corn

- 5.3.1.3.2 Rice

- 5.3.1.3.3 Sorghum

- 5.3.1.3.4 Wheat

- 5.3.1.3.5 Other Grains & Cereals

- 5.3.1.4 Oilseeds

- 5.3.1.4.1 Canola, Rapeseed & Mustard

- 5.3.1.4.2 Soybean

- 5.3.1.4.3 Sunflower

- 5.3.1.4.4 Other Oilseeds

- 5.3.1.5 Pulses

- 5.3.2 Vegetables

- 5.3.2.1 Brassicas

- 5.3.2.1.1 Cabbage

- 5.3.2.1.2 Carrot

- 5.3.2.1.3 Cauliflower & Broccoli

- 5.3.2.1.4 Other Brassicas

- 5.3.2.2 Cucurbits

- 5.3.2.2.1 Cucumber & Gherkin

- 5.3.2.2.2 Pumpkin & Squash

- 5.3.2.2.3 Other Cucurbits

- 5.3.2.3 Roots & Bulbs

- 5.3.2.3.1 Garlic

- 5.3.2.3.2 Onion

- 5.3.2.3.3 Potato

- 5.3.2.3.4 Other Roots & Bulbs

- 5.3.2.4 Solanaceae

- 5.3.2.4.1 Chilli

- 5.3.2.4.2 Eggplant

- 5.3.2.4.3 Tomato

- 5.3.2.4.4 Other Solanaceae

- 5.3.2.5 Unclassified Vegetables

- 5.3.2.5.1 Asparagus

- 5.3.2.5.2 Lettuce

- 5.3.2.5.3 Okra

- 5.3.2.5.4 Peas

- 5.3.2.5.5 Spinach

- 5.3.2.5.6 Other Unclassified Vegetables

- 5.3.1 Row Crops

- 5.4 State

- 5.4.1 Bihar

- 5.4.2 Gujarat

- 5.4.3 Haryana

- 5.4.4 Karnataka

- 5.4.5 Madhya Pradesh

- 5.4.6 Maharashtra

- 5.4.7 Rajasthan

- 5.4.8 Telangana

- 5.4.9 Uttar Pradesh

- 5.4.10 West Bengal

- 5.4.11 Other States

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Advanta Seeds - UPL

- 6.4.2 BASF SE

- 6.4.3 Bayer AG

- 6.4.4 Corteva Agriscience

- 6.4.5 East-West Seed

- 6.4.6 Groupe Limagrain

- 6.4.7 Kaveri Seeds

- 6.4.8 Nuziveedu Seeds Ltd

- 6.4.9 Rijk Zwaan Zaadteelt en Zaadhandel BV

- 6.4.10 Syngenta Group

7 KEY STRATEGIC QUESTIONS FOR SEEDS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Global Market Size and DROs

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

Have a question?

SELECT AN OPTION

Have a question?

Questions? Please give us a call or visit the contact form.