PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1445770

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1445770

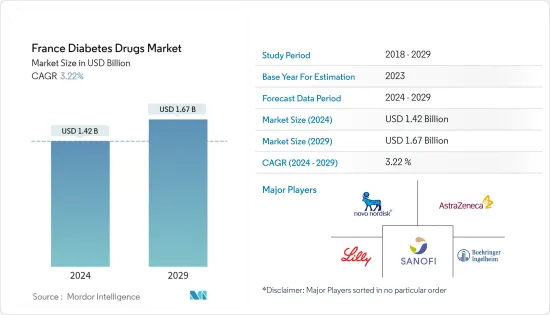

France Diabetes Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The France Diabetes Drugs Market size is estimated at USD 1.42 billion in 2024, and is expected to reach USD 1.67 billion by 2029, growing at a CAGR of 3.22% during the forecast period (2024-2029).

One of the most significant risk factors for a severe course of COVID-19 is diabetes mellitus. This risk is believed to be influenced by several variables that are frequently present in diabetes mellitus, such as advanced age, a proinflammatory and hypercoagulable condition, hyperglycemia, and underlying comorbidities (hypertension, cardiovascular disease, chronic kidney disease, and obesity). Diabetes was quickly recognized as a risk factor for bad results during the COVID-19 pandemic. That's why managing or delaying cases of type 2 diabetes became more important than ever before. Several studies have confirmed that chronic diseases like diabetes are associated with adverse outcomes in COVID-19 patients

Diabetic drugs are medicines developed to stabilize and control blood glucose levels amongst people with diabetes. Diabetic drugs have been potential candidates for treating diabetic patients affected by SARS-CoV-2 infection during the COVID-19 pandemic. Diabetes has the highest prevalence among all chronic conditions covered 100% by France's statutory health insurance (SHI), and the number of covered patients has doubled in the past 10 years. France is one of the major countries in the Europe region.

According to the World Health Organization (WHO), about a million are diagnosed with diabetes in France. The prevalence of diabetes is growing among all ages in France, which can be attributed to the growing obese population, along with unhealthy diets and sedentary lifestyles of people. Thus, the rising prevalence of diabetes and obesity, growing awareness, regarding diabetic care, healthcare expenditure, and technological advancements are a few factors that are further driving the market for diabetes drugs in France. In France, there is a centralized health care system their all the reimbursement decisions are taken at a national level and then applies to all the countries.

Therefore, owing to the aforementioned factors the studied market is anticipated to witness growth over the analysis period.

France Diabetes Drugs Market Trends

The oral anti-diabetic drugs segment holds the highest market share in the France Diabetes Drugs Market in the current year

The oral anti-diabetic drugs segment holds the highest market share of about 55.8% in the France Diabetes Drugs Market in the current year.

Oral Anti-Diabetic Drugs are available internationally and are recommended for use when escalation of treatment for type 2 diabetes is required along with lifestyle management. Oral agents are typically the first medications used in treating type 2 diabetes due to their wide range of efficacy, safety, and mechanisms of action. Anti-diabetic drugs help diabetes patients control their condition and lower the risk of diabetes complications. People with diabetes may need to take anti-diabetic drugs for their whole lives to control their blood glucose levels and avoid hypoglycemia and hyperglycemia.

The disease's growing incidence, prevalence, and progressive nature encouraged the development of new drugs to provide additional treatment options for diabetic patients. Over the past decade, two important classes entered this market: dipeptidyl peptidase-4 inhibitors (DPP-4) and sodium-glucose cotransporter-2 inhibitors (SGLT-2). Oral anti-diabetic agents work in various ways to reduce blood sugar levels in people with type 2 diabetes. Some stimulate insulin secretion by the pancreas, and others improve the cell responsiveness to insulin or prevent glucose production by the liver. Others slow the absorption of glucose after meals.

Oral anti-diabetic agents present the advantages of easier management and lower cost. So they became an attractive alternative to insulin with better acceptance, which enhances adherence to the treatment. The French health benefit basket plays an important role. Diabetes is one of the 30 chronic diseases covered 100% by statutory health insurance (SHI) under the ALD scheme (affections de longue duree). For those not covered under ALD, the patient pays a share of the official health care tariff, which varies depending on the category of goods and care.

Owing to the above factors, the market will likely continue to grow.

Glucagon-like Peptide-1 Receptor Agonist Segment holds the highest market share in the France Diabetes Drugs Market in the current year

Glucagon-like Peptide-1 Receptor Agonist Segment holds the highest market share of more than 25.5% in the France Diabetes Drugs Market in the current year.

Glucagon-like peptide-1 receptor agonists (GLP-1RAs) are a class of medications used for treating type 2 diabetes, and some drugs are also approved for obesity. One of the benefits of this class of drugs over older insulin secretagogues, such as sulfonylureas or meglitinides, is that they include a lower risk of causing hypoglycemia. Besides being important glucose-lowering agents, GLP-1RAs contain significant anti-inflammatory and pulmonary protective effects and benefit gut microbes' composition.

According to a survey by the EU Commission, the number of persons in France who include chronic diabetes is the largest, and one in 10 people in France suffers from diabetes. The prevalence of diabetes is significant in France, although the rules' target of 80% compliance with advised healthcare consultations isn't always met. To promote proactive therapy adjustment and decrease therapeutic inertia, new techniques that focus on patient and physician education and information are necessary to lessen the burden of diabetes.

The disease's growing incidence, prevalence, and progressive nature encouraged the development of new drugs to provide additional treatment options for diabetic patients. The roll-out of many new products, increasing international research collaborations in technology advancement, and increasing awareness about diabetes among the people are some of the market opportunities for the players in the France diabetes drugs market.

France Diabetes Drugs Industry Overview

The France Diabetes Drugs Market is moderately fragmented, with major manufacturers, namely Eli Lilly, Sanofi, Novo Nordisk, and AstraZeneca, holding a presence in the region. A major share of the market is held by manufacturers concomitant with strategy-based M&A operations and constantly entering the market to generate new revenue streams and boost existing ones. These measures taken by the market players will ensure a competitive marketplace, forcing companies to experiment with new technologies.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Insulins

- 5.1.1 Basal or Long Acting Insulins

- 5.1.1.1 Lantus (Insulin Glargine)

- 5.1.1.2 Levemir (Insulin Detemir)

- 5.1.1.3 Toujeo (Insulin Glargine)

- 5.1.1.4 Tresiba (Insulin Degludec)

- 5.1.1.5 Basaglar (Insulin Glargine)

- 5.1.2 Bolus or Fast Acting Insulins

- 5.1.2.1 NovoRapid/Novolog (Insulin Aspart)

- 5.1.2.2 Humalog (Insulin Lispro)

- 5.1.2.3 Apidra (Insulin Glulisine)

- 5.1.3 Traditional Human Insulins

- 5.1.3.1 Novolin/Actrapid/Insulatard

- 5.1.3.2 Humulin

- 5.1.3.3 Insuman

- 5.1.4 Biosimilar Insulins

- 5.1.4.1 Insulin Glargine Biosimilars

- 5.1.4.2 Human Insulin Biosimilars

- 5.1.1 Basal or Long Acting Insulins

- 5.2 Oral Anti-diabetic drugs

- 5.2.1 Biguanides

- 5.2.1.1 Metformin

- 5.2.2 Alpha-Glucosidase Inhibitors

- 5.2.2.1 Alpha-Glucosidase Inhibitors

- 5.2.3 Dopamine D2 receptor agonist

- 5.2.3.1 Bromocriptin

- 5.2.4 SGLT-2 inhibitors

- 5.2.4.1 Invokana (Canagliflozin)

- 5.2.4.2 Jardiance (Empagliflozin)

- 5.2.4.3 Farxiga/Forxiga (Dapagliflozin)

- 5.2.4.4 Suglat (Ipragliflozin)

- 5.2.5 DPP-4 inhibitors

- 5.2.5.1 Onglyza (Saxagliptin)

- 5.2.5.2 Tradjenta (Linagliptin)

- 5.2.5.3 Vipidia/Nesina(Alogliptin)

- 5.2.5.4 Galvus (Vildagliptin)

- 5.2.6 Sulfonylureas

- 5.2.6.1 Sulfonylureas

- 5.2.7 Meglitinides

- 5.2.7.1 Meglitinides

- 5.2.1 Biguanides

- 5.3 Non-Insulin Injectable drugs

- 5.3.1 GLP-1 receptor agonists

- 5.3.1.1 Victoza (Liraglutide)

- 5.3.1.2 Byetta (Exenatide)

- 5.3.1.3 Bydureon (Exenatide)

- 5.3.1.4 Trulicity (Dulaglutide)

- 5.3.1.5 Lyxumia (Lixisenatide)

- 5.3.2 Amylin Analogue

- 5.3.2.1 Symlin (Pramlintide)

- 5.3.1 GLP-1 receptor agonists

- 5.4 Combination drugs

- 5.4.1 Insulin combinations

- 5.4.1.1 NovoMix (Biphasic Insulin Aspart)

- 5.4.1.2 Ryzodeg (Insulin Degludec and Insulin Aspart)

- 5.4.1.3 Xultophy (Insulin Degludec and Liraglutide)

- 5.4.2 Oral Combinations

- 5.4.2.1 Janumet (Sitagliptin and Metformin)

- 5.4.1 Insulin combinations

6 MARKET INDICATORS

- 6.1 Type-1 Diabetic Population

- 6.2 Type-2 Diabetic Population

7 COMPETITIVE LANDSCAPE

- 7.1 COMPANY PROFILES

- 7.1.1 Novo Nordisk A/S

- 7.1.2 Takeda

- 7.1.3 Pfizer

- 7.1.4 Eli Lilly

- 7.1.5 Janssen Pharmaceuticals

- 7.1.6 Astellas

- 7.1.7 Boehringer Ingelheim

- 7.1.8 Merck and Co.

- 7.1.9 AstraZeneca

- 7.1.10 Bristol Myers Squibb

- 7.1.11 Novartis

- 7.1.12 Sanofi Aventis

- 7.2 COMPANY SHARE ANALYSIS

- 7.2.1 Novo Nordisk A/S

- 7.2.2 Sanofi Aventis

- 7.2.3 Eli Lilly

- 7.2.4 Merck and Co.

- 7.2.5 Others

8 MARKET OPPORTUNITIES AND FUTURE TRENDS