PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911804

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1911804

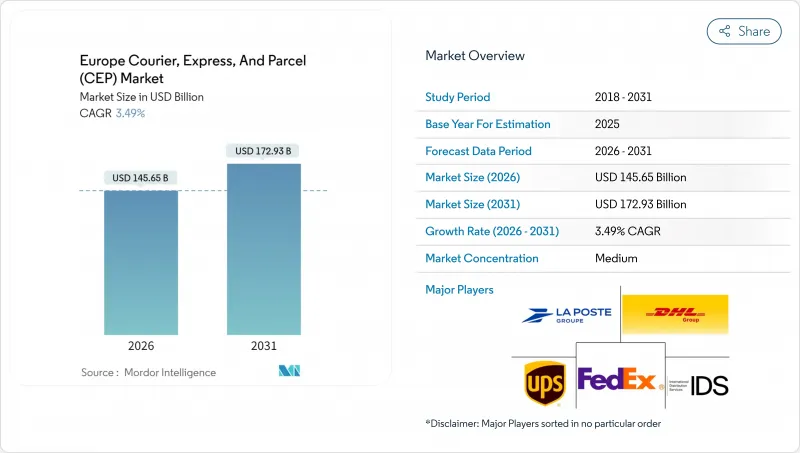

Europe Courier, Express, And Parcel (CEP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe courier, express, and parcel (CEP) market size in 2026 is estimated at USD 145.65 billion, growing from 2025 value of USD 140.74 billion with 2031 projections showing USD 172.93 billion, growing at 3.49% CAGR over 2026-2031.

This moderate trajectory masks deeper structural shifts as e-commerce expansion, regulatory harmonization, and technology adoption reshape last-mile networks across the continent. Retailers are prioritizing delivery-experience differentiation because 81% of European shoppers abandon baskets when preferred options are unavailable, tilting competitive focus from price to service quality. EU-level VAT in the Digital Age (ViDA) reforms, phased through 2035, are standardizing cross-border data flows, favoring scale players with advanced compliance systems. Meanwhile, a driver shortfall exceeding 500,000 openings has accelerated automation investment as operators grapple with labor scarcity. Heightened sustainability mandates and city-center zero-emission zones, notably in the Netherlands, add urgency for electric fleets and parcel-locker density, reinforcing consolidation among carriers that can fund green assets.

Europe Courier, Express, And Parcel (CEP) Market Trends and Insights

Explosive E-Commerce and Omnichannel Retail Boom

Social-commerce momentum is steering parcel flows toward unpredictable, trend-driven peaks rather than traditional seasonality, requiring flexible capacity planning across the Europe courier, express, and parcel (CEP) market. German e-commerce packaging spend reached USD 3.99 billion in 2025, reflecting 14.03% CAGR (2025-2030) expectations through 2034, underlining the packaging intensity of this growth. Reverse-logistics sophistication is turning from add-on to core capability, as 79% of shoppers cancel purchases when returns appear difficult. Healthcare parcels are piggybacking on this omnichannel wave; DHL's EUR 2 billion (USD 2.20 billion) health-logistics rollout funds specialized cold-chain services aligned with rising e-pharmacy penetration. Volume concentration around influencer promotions compels carriers to design dynamic routing algorithms to absorb traffic surges without impairing service-level compliance.

Liberalized Intra-EU Cross-Border Trade and VAT Reforms

ViDA's e-invoicing mandate arriving in July 2030 will standardize EN16931 formats for all intra-EU B2B trades, shrinking manual paperwork and accelerating customs clearances. The July 2028 expansion of the One-Stop Shop lets merchants maintain a single VAT ID across member states, a boon for the Europe courier, express, and parcel (CEP) market handling millions of cross-border parcels daily. Advanced IT retrofits are required because declarations must be filed within 10 days of chargeable events, favoring operators that already run integrated data lakes. Concurrently, Import Control System 2 obliges detailed entry summaries before crossing EU borders, tightening security and tilting the playing field to carriers with rich product-level data pipelines. Together, these measures reduce friction in sales expansion while raising digital-compliance thresholds, shaping a long-run shift toward international consolidation.

Margin Squeeze from Price Wars and Dimension-Based Tariffs

Post-pandemic overcapacity has resurrected discounting as operators defend share, eroding yields despite volume growth in the Europe courier, express, and parcel (CEP) market. Dimensional-weight pricing, meant to reflect cubic consumption, often gets waived for strategic accounts, compressing margins faster than cost-line efficiencies. InPost's acquisitions of Yodel and Sending highlight the pivot toward inorganic density to dilute fixed overhead. Carriers add peak or fuel surcharges but shippers push back, leveraging multicarrier software to arbitrage rates. The tug-of-war limits near-term price recovery while stoking further consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Parcel Lockers and PUDO Networks

- Automation and AI-Driven Operational Efficiency

- Acute Driver and Warehouse-Labor Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

E-commerce retained a 34.45% share in 2025, yet healthcare parcels are set to rise fastest at 3.79% CAGR between 2026-2031. Aging populations and e-pharmacy expansion make temperature-controlled last-mile a priority.

DHL's EUR 2 billion (USD 2.20 billion) program funds GDP-compliant facilities, cool-chain packaging, and dedicated control towers. Manufacturers require part-express lanes, and financial-services documents sustain secure-courier niches. Carriers cross-sell same-day biomedical pickup to monetize vehicle downtime during retail off-peak cycles.

Cross-border parcel flows accounted for 34.28% of revenues in 2025 as domestic services retained the remainder of Europe courier, express, and parcel (CEP) market share. International consignments are forecast to climb at a 3.73% CAGR between 2026-2031, outpacing domestic growth as ViDA simplifies VAT settlement and merchants centralize fulfillment.

European shoppers increasingly purchase from neighboring states once delivery times align with domestic benchmarks. InPost's November 2024 network activation across eight EU countries uses a locker-to-locker model that bypasses manual sorting and customs delays. ICS2 data prerequisites initially elongate lead-times for goods sourced outside the bloc, but EU-internal routes face fewer friction points. Improved service predictability attracts SME exporters, prompting postal incumbents to upgrade track-and-trace and push into premium cross-border offerings.

The Europe Courier, Express, and Parcel (CEP) Market Report is Segmented by End User Industry (E-Commerce and More), Destination (Domestic and International), Speed of Delivery (Express and Non-Express), Shipment Weight (Heavy Weight Shipments, and More), Mode of Transport (Air, Road, and Others), and Model (Business-To-Business, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- DHL Group

- FedEx

- GEODIS

- International Distributions Services (including GLS)

- La Poste Group

- Logista

- Otto GmbH & Co. KG

- Post NL

- Poste Italiane

- Sterne Group

- United Parcel Service (UPS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Logistics Performance

- 4.12 Infrastructure

- 4.13 Regulatory Framework

- 4.13.1 Central and Eastern Europe (CEE)

- 4.13.2 France

- 4.13.3 Germany

- 4.13.4 Italy

- 4.13.5 Netherlands

- 4.13.6 Nordics

- 4.13.7 Russia

- 4.13.8 Spain

- 4.13.9 Switzerland

- 4.13.10 United Kingdom

- 4.14 Value Chain and Distribution Channel Analysis

- 4.15 Market Drivers

- 4.15.1 Explosive E-Commerce and Omnichannel Retail Boom

- 4.15.2 Liberalized Intra-EU Cross-Border Trade and VAT Reforms

- 4.15.3 Expansion of Parcel Lockers and PUDO Networks

- 4.15.4 Automation and AI-Driven Operational Efficiency

- 4.15.5 Carbon-Cost Internalization Favouring Green CEP Fleets

- 4.15.6 Rise of Multicarrier Parcel-Management Platforms

- 4.16 Market Restraints

- 4.16.1 Margin Squeeze from Price Wars and Dimension-Based Tariffs

- 4.16.2 Acute Driver and Warehouse-Labor Shortages

- 4.16.3 Country-Level Courier Wage-Floor Legislation

- 4.16.4 Rising Cyber-Security and Data-Sovereignty Compliance Costs

- 4.17 Technology Innovations in the Market

- 4.18 Porter's Five Forces Analysis

- 4.18.1 Threat of New Entrants

- 4.18.2 Bargaining Power of Buyers

- 4.18.3 Bargaining Power of Suppliers

- 4.18.4 Threat of Substitutes

- 4.18.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 Destination

- 5.1.1 Domestic

- 5.1.2 International

- 5.2 Speed of Delivery

- 5.2.1 Express

- 5.2.2 Non-Express

- 5.3 Model

- 5.3.1 Business-to-Business (B2B)

- 5.3.2 Business-to-Consumer (B2C)

- 5.3.3 Consumer-to-Consumer (C2C)

- 5.4 Shipment Weight

- 5.4.1 Heavy Weight Shipments

- 5.4.2 Light Weight Shipments

- 5.4.3 Medium Weight Shipments

- 5.5 Mode of Transport

- 5.5.1 Air

- 5.5.2 Road

- 5.5.3 Others

- 5.6 End User Industry

- 5.6.1 E-Commerce

- 5.6.2 Financial Services (BFSI)

- 5.6.3 Healthcare

- 5.6.4 Manufacturing

- 5.6.5 Primary Industry

- 5.6.6 Wholesale and Retail Trade (Offline)

- 5.6.7 Others

- 5.7 Country

- 5.7.1 Albania

- 5.7.2 Bulgaria

- 5.7.3 Croatia

- 5.7.4 Czech Republic

- 5.7.5 Denmark

- 5.7.6 Estonia

- 5.7.7 Finland

- 5.7.8 France

- 5.7.9 Germany

- 5.7.10 Hungary

- 5.7.11 Iceland

- 5.7.12 Italy

- 5.7.13 Latvia

- 5.7.14 Lithuania

- 5.7.15 Netherlands

- 5.7.16 Norway

- 5.7.17 Poland

- 5.7.18 Romania

- 5.7.19 Russia

- 5.7.20 Slovak Republic

- 5.7.21 Slovenia

- 5.7.22 Spain

- 5.7.23 Sweden

- 5.7.24 Switzerland

- 5.7.25 United Kingdom

- 5.7.26 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 FedEx

- 6.4.3 GEODIS

- 6.4.4 International Distributions Services (including GLS)

- 6.4.5 La Poste Group

- 6.4.6 Logista

- 6.4.7 Otto GmbH & Co. KG

- 6.4.8 Post NL

- 6.4.9 Poste Italiane

- 6.4.10 Sterne Group

- 6.4.11 United Parcel Service (UPS)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment