PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934660

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1934660

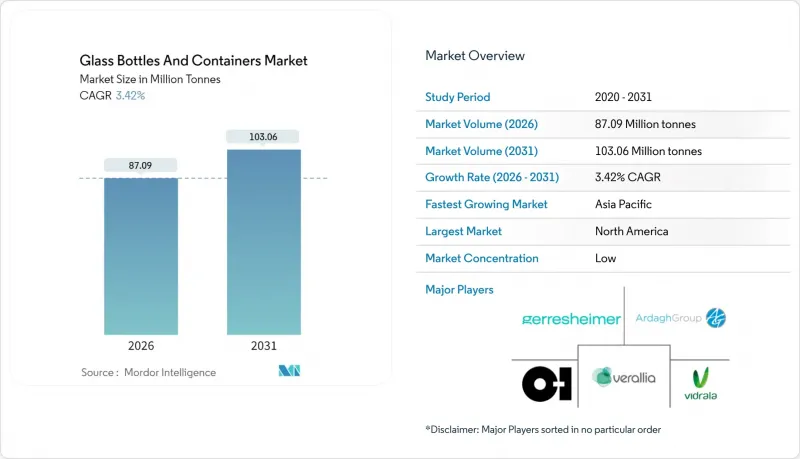

Glass Bottles And Containers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Glass Bottles and Containers market is expected to grow from 84.21 million tonnes in 2025 to 87.09 million tonnes in 2026 and is forecast to reach 103.06 million tonnes by 2031 at 3.42% CAGR over 2026-2031.

Heightened regulatory pressure on single-use plastics, premiumization in beauty and spirits, and pharmaceutical fill-finish expansion are steering steady gains despite energy-price headwinds. California's 65% plastic-reduction mandate and France's polystyrene ban have already swung demand toward infinitely recyclable glass.Hybrid furnaces, oxy-fuel combustion, and high-cullet recipes are mitigating cost exposure, while lightweighting breakthroughs such as Vidrala's 260-gram 75 cl bottle trim material intensity without sacrificing shelf appeal. Producers also leverage color differentiation, especially amber, to protect light-sensitive drugs and craft beverages, reinforcing value over lighter substitutes.

Global Glass Bottles And Containers Market Trends and Insights

Plastic Bans Drive Shift to Recyclable Glass Packaging

California's SB 54 mandates a 65% cut in single-use plastic packaging by 2032, while France has barred expanded polystyrene food containers from January 2025, propelling brand owners to switch to glass. The European Union's pending bisphenol-A restrictions further reinforce conversion in food contact segments. Because glass maintains an endless closed loop and established curb-side collection, converters are capturing new volumes even as they absorb retooling costs. The ripple effect is evident in beverage and condiment lines moving back to glass at big-box retailers. Though cullet supply tightens temporarily, hybrid furnaces and lightweighting partially offset margin compression, paving a sustained uplift through the forecast horizon.

Prestige Beauty "Glassification" Trend Lifts Jar and Bottle Volumes

Luxury skincare and fragrance brands increasingly adopt glass to signal premium quality and environmental stewardship. Verallia's 100% post-consumer-recycled (PCR) Vista bottles cut energy use by 40% versus virgin production, proving that circularity can coexist with high-end aesthetics.Embossing, color gradations, and refillable designs amplify shelf differentiation and justify higher price points. Since packaging cost is a small share of retail value in beauty, brands absorb higher unit costs more easily than mass-market beverages. The trend scales globally but is most pronounced in North America and Western Europe, reinforcing long-tail demand for custom molds and short production runs.

Energy Price Volatility Threatens Furnace Economics

Electricity prices in the United Kingdom spiked to record levels in 2024, compelling glassmakers to idle lines during peak tariffs. Energy constitutes roughly 18% of production costs, so volatility can erase margins faster than price adjustments reach the market. Carbon-pricing schemes further penalize fossil-fuel consumption, intensifying capital commitments toward hybrid furnaces and on-site renewables. In contrast, O-I Glass secured USD 125 million in federal funding for decarbonization, but smaller regional plants face liquidity strains, potentially curbing short-term supply.

Other drivers and restraints analyzed in the detailed report include:

- Pharma Fill-Finish Expansion Boosts Demand for Glass Vials

- Craft Alcohol Boom Spurs Custom Glass Container Demand

- rPET Bottle Adoption Undercuts Glass in Logistics-Sensitive Channels

For complete list of drivers and restraints, kindly check the Table Of Contents.

Geography Analysis

North America captured 55.18% of the container glass packaging market in 2025, leveraging mature curbside collection and corporate sustainability goals that encourage high-cullet recipes. The Glass Packaging Institute's roadmap to reach a 50% recycling rate by 2030 underpins the long-term feedstock base. Yet energy-price swings and growing rPET penetration in value beverages temper volume gains, shifting strategic emphasis toward premium spirits and beauty care.

Europe trails but benefits from the EU's 80.8% recycling rate, which secures cullet and lowers furnace energy demand. Ardagh and Verallia are investing in electric-boost and hydrogen-ready furnaces to hedge carbon-pricing exposure while maintaining output. However, power-price stress and environmental levies suppress near-term margins, sparking collaboration on shared renewable micro-grids and cross-border cullet trade.

Asia Pacific is the fastest-growing region, expanding 4.76% CAGR through 2031 and rapidly closing the gap in the container glass packaging market. India and China build greenfield pharmaceutical plants that require sterile vials, while South Korea and Japan import premium cosmetic glass for luxury skincare. O-I Glass's USD 120 million upgrade in Zipaquira, Colombia, signals how producers replicate best-in-class technology in emerging regions to capture demand while aligning with ESG mandates. Limited cullet infrastructure in parts of Southeast Asia constrains recycled content, creating cost penalties versus Western peers; nevertheless, rising incomes and regulatory push for circularity promise robust long-term demand.

- O-I Glass, Inc.

- Verallia S.A.

- Ardagh Group S.A.

- Vidrala S.A.

- Vetropack Holding AG

- Gerresheimer AG

- SGD S.A.

- Stoelzle Oberglas GmbH

- Wiegand-Glas Holding GmbH

- Hindusthan National Glass & Industries Limited

- Piramal Glass Private Limited

- Nihon Yamamura Glass Co., Ltd.

- Sisecam

- Compagnie de Saint-Gobain S.A. (Packaging division)

- Heinz-Glas GmbH & Co. KGaA

- Vitro, S.A.B. de C.V.

- BA Glass B.V.

- Ciner Glass Holdings Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Plastic Bans Drive Shift to Recyclable Glass Packaging

- 4.2.2 Prestige Beauty "Glassification" Trend Lifts Jar and Bottle Volumes

- 4.2.3 Pharma Fill-Finish Expansion Boosts Demand for Glass Vials

- 4.2.4 Craft Alcohol Boom Spurs Custom Glass Container Demand

- 4.2.5 FDI-Funded Hybrid Furnaces Expand Green Glass Capacity

- 4.2.6 ESG Compliance Spurs Shift to High-Cullet Glass for Export Markets

- 4.3 Market Restraints

- 4.3.1 Energy Price Volatility Threatens Furnace Economics

- 4.3.2 rPET Bottle Adoption Undercuts Glass in Logistics-Sensitive Channels

- 4.3.3 Weak Cullet Collection Infrastructure Limits Recycled Content

- 4.3.4 Breakage Losses in Long-Haul Shipping Discourage Glass Use

- 4.4 Industry Supply-Chain Analysis

- 4.5 Container Glass Furnace Capacity and Locations in Global

- 4.5.1 Plant Locations and Year of Commencement

- 4.5.2 Production Capacities

- 4.5.3 Types of Furnaces

- 4.5.4 Color of Glass Produced

- 4.6 Export-Import Data of Container Glass - Covering Key Import and Export Destinations

- 4.6.1 Import Volume and Value, 2021-2024

- 4.6.2 Export Volume and Value, 2021-2024

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Raw Material Analysis

- 4.9 Recycling Trends for Glass Packaging

- 4.10 Demand vs Supply Analysis for Glass Packaging

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By End-user

- 5.1.1 Beverages

- 5.1.1.1 Alcoholic

- 5.1.1.1.1 Beer

- 5.1.1.1.2 Wine

- 5.1.1.1.3 Spirits

- 5.1.1.1.4 Other Alcoholic Beverages (Cider and Other Fermented Drinks)

- 5.1.1.2 Non-Alcoholic

- 5.1.1.2.1 Juices

- 5.1.1.2.2 Carbonated Drinks (CSDs)

- 5.1.1.2.3 Dairy Product Based Drinks

- 5.1.1.2.4 Other Non-Alcoholic Beverages

- 5.1.1.1 Alcoholic

- 5.1.2 Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles)

- 5.1.3 Cosmetics and Personal Care

- 5.1.4 Pharmaceuticals (excluding Vials and Ampoules)

- 5.1.5 Perfumery

- 5.1.1 Beverages

- 5.2 By Color

- 5.2.1 Green

- 5.2.2 Amber

- 5.2.3 Flint

- 5.2.4 Other Colors

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 United Kingdom

- 5.3.3.2 Germany

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 Asia Pacific

- 5.3.4.1 China

- 5.3.4.2 Japan

- 5.3.4.3 India

- 5.3.4.4 South Korea

- 5.3.4.5 Australia

- 5.3.4.6 Rest of Asia Pacific

- 5.3.5 Middle East and Africa

- 5.3.5.1 Middle East

- 5.3.5.1.1 United Arab Emirates

- 5.3.5.1.2 Saudi Arabia

- 5.3.5.1.3 Turkey

- 5.3.5.1.4 Rest of Middle East

- 5.3.5.2 Africa

- 5.3.5.2.1 South Africa

- 5.3.5.2.2 Nigeria

- 5.3.5.2.3 Rest of Africa

- 5.3.5.1 Middle East

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Company Market Share Analysis, (Based on Latest Production Capacity)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 O-I Glass, Inc.

- 6.4.2 Verallia S.A.

- 6.4.3 Ardagh Group S.A.

- 6.4.4 Vidrala S.A.

- 6.4.5 Vetropack Holding AG

- 6.4.6 Gerresheimer AG

- 6.4.7 SGD S.A.

- 6.4.8 Stoelzle Oberglas GmbH

- 6.4.9 Wiegand-Glas Holding GmbH

- 6.4.10 Hindusthan National Glass & Industries Limited

- 6.4.11 Piramal Glass Private Limited

- 6.4.12 Nihon Yamamura Glass Co., Ltd.

- 6.4.13 Sisecam

- 6.4.14 Compagnie de Saint-Gobain S.A. (Packaging division)

- 6.4.15 Heinz-Glas GmbH & Co. KGaA

- 6.4.16 Vitro, S.A.B. de C.V.

- 6.4.17 BA Glass B.V.

- 6.4.18 Ciner Glass Holdings Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment