PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035126

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035126

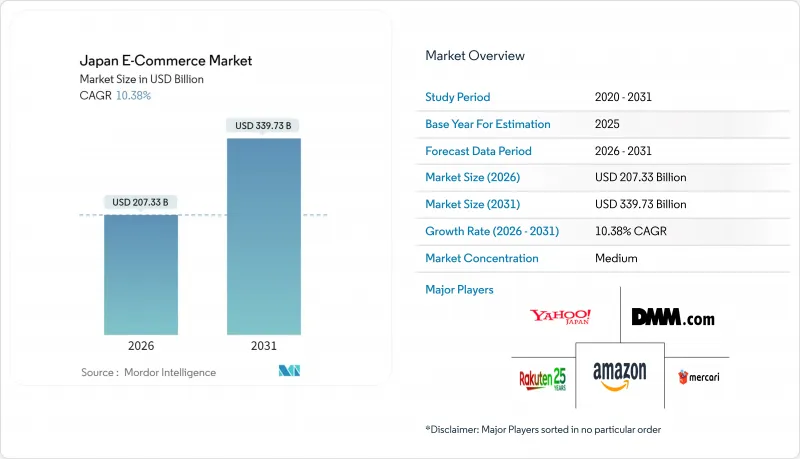

Japan E-Commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan e-commerce market size stands at USD 207.33 billion in 2026 and is projected to reach USD 339.73 billion by 2031, reflecting a robust 10.38% CAGR.

Consumer migration from cash to digital payments, government incentives that extend cashless subsidies to 2027, and logistics networks capable of sub-one-hour fulfillment in major cities are amplifying the addressable base. Structural tailwinds include rising smartphone penetration among seniors, accelerated adoption of buy-now-pay-later (BNPL) by Gen-Z females, and platform investments in generative-AI merchandising that compress browsing and checkout into a single mobile session. Enterprise digitization lags the retail curve, yet tax incentives for electronic invoicing and procurement card programs signal a sizable future inflection. Competitive behavior continues to revolve around ecosystem lock-in: Rakuten pairs loyalty points with financial services, Amazon Japan uses Prime to secure repeat orders, and Yahoo Japan leverages the PayPay super-app to widen daily engagement.

Japan E-Commerce Market Trends and Insights

Rising Silver-Economy Digital Spend in Urban Prefectures

Japan's over-65 demographic reached 29.3% of the population in 2024, yet internet usage among seniors climbed into the mid-80% range in Tokyo, Osaka, and Nagoya. Voice-assisted navigation, family-linked accounts, and same-day delivery windows designed around retiree schedules have removed usability friction. Household savings averaging JPY 24.3 million (USD 162,000) combined with lower price sensitivity mean each new senior adopter delivers higher lifetime value than younger cohorts. Retailers are re-architecting mobile checkout to a three-tap flow and layering prescription-management modules for health supplements, thereby widening the Japan e-commerce market beyond traditional tech-savvy users. Platform loyalty schemes that allow family members to pool points further stimulate discretionary spend. The result is incremental volume rather than channel substitution, raising revenue density in metropolitan prefectures and improving logistical route economics.

Consolidation of 1-Hour Hyper-Local Delivery Networks in Tokyo and Osaka

Micro-fulfillment centers within 3 km of dense residential clusters now underpin one-hour grocery and convenience deliveries. Same-day or next-day preferences for online grocery in Tokyo rose to 62% in 2025, a 14-point gain over three years. Uber Eats, Wolt, and DoorDash lock in customers by bundling dark-store exclusives, while Rakuten Seiyu Netsuper defends share with automated picking lines inside legacy supermarket backrooms. Yamato Transport's 2025 introduction of cargo flights between Haneda and regional hubs was a direct hedge against driver shortages yet simultaneously enabled faster restocks for these urban nodes. As localized density grows, service-level differentiation eclipses price competition, raising barriers to entry and lengthening the customer-lifetime window for established players.

Logistics Labour Shortage Beyond 2026 (Yamato "2024 Problem")

Annual driver overtime caps set at 960 hours from April 2024 have tightened parcel-handling capacity, forcing Yamato to refuse peak-season loads and lift commercial rates by double digits. Forty percent of drivers are already over 50, while recruitment classes shrink year on year, creating a structural deficit that ripples through fulfillment costs. Parcel carriers prioritize high-density urban routes, leaving rural prefectures exposed to longer lead times that chill order volumes. Platforms experimenting with cargo flights and autonomous delivery corridors may blunt the worst impacts, but labor scarcity remains a medium-term drag on service levels and margins inside the Japan e-commerce market.

Other drivers and restraints analyzed in the detailed report include:

- Government Cashless-Subsidy Extension to 2027

- Surge in In-game and Livestream-Commerce Monetization

- Digital-Platform Fair-Trading Act Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Business-to-consumer activity represented 86.76% of transaction value in 2025, cementing its lead after decades of platform investment. Despite this dominance, business-to-business flows are forecast to rise at a 12.03% CAGR through 2031, the highest of any model inside the Japan e-commerce market. MonotaRO booked JPY 288.1 billion (USD 1.92 billion) in 2024 sales, yet still captured under 3% of the wider maintenance-repair-operations universe, revealing massive offline whitespace. Procurement-system integrations jumped 27.9%, signaling that mid-sized manufacturers now plug e-catalogs directly into ERP workflows, thereby slashing manual data entry. Rakuten Card's March 2025 initiative to chase JPY 1,100 trillion (USD 7.33 trillion) in corporate spend underscores the strategic pivot toward enterprise payments. As tax incentives for electronic invoicing kick in, digitized procurement is set to tilt the revenue mix, expanding the Japan e-commerce market size while compressing processing errors.

The upside is tempered by cultural inertia in indirect spend, where fax orders persist. Yet macro forces, corporate decarbonization reporting and supply-chain traceability mandates, necessitate digital audit trails, indirectly nudging firms onto e-procurement rails. Service providers now bundle spend analytics with compliance dashboards, making platform adoption a governance hedge. Combined with looming succession issues at small manufacturers, where digital fluency is a hiring criterion, enterprise e-commerce has moved from optional to inevitable. Consequently, capital allocation within leading platforms now balances consumer retention with aggressive moves into industrial categories, reshaping competitive priorities across the Japan e-commerce market.

Smartphones accounted for 64.76% of 2025 transaction value and are projected to grow at 11.48% annually, expanding both share and total spend. Seniors adopting voice-assisted search and Gen-Z treating phones as a primary computer underpin this surge. Desktop's role is narrowing to high-consideration purchases such as premium electronics where screen real estate aids feature comparison. Voice-enabled devices and wearables begin to register meaningful volume, aided by natural-language payment authentication. Generative-AI try-on tools accelerate mobile conversion by collapsing discovery and purchase steps into a single interaction. Perfect Corp.'s May 2025 launch cut fashion return rates by 18% among early adopters. These gains feed directly into gross merchandise value, lifting the Japan e-commerce market size for mobile-originated sales.

Investment priorities now emphasize thumb-optimized UX, biometric login, and latency reduction to beat the five-second abandonment threshold. Parallel upgrades to desktop sites focus on AR overlays for large-ticket items, preserving relevance where visual fidelity matters. The strategic payoff is a wider funnel: previously offline seniors join via simplified mobile interfaces, while younger users deepen engagement through social-media-linked storefronts. This two-pronged expansion reinforces the primacy of mobile without amputating desktop revenue streams inside the Japan e-commerce market.

The Japan E-Commerce Market Report is Segmented by Business Model (B2C, and B2B), Device Type for B2C (Smartphone/Mobile, Desktop and Laptop, and More), Payment Method for B2C (Credit and Debit Cards, Digital Wallets, BNPL, and More), Product Category for B2C (Beauty and Personal Care, Consumer Electronics, Fashion and Apparel, Furniture and Home, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Rakuten Group, Inc.

- Amazon Japan G.K.

- Yahoo Japan Corporation

- Mercari, Inc.

- DMM.com LLC

- ZOZO Inc. (ZOZOTOWN)

- Apple Japan Inc.

- au PAY Market (KDDI Corp.)

- Maruetsu Co., Ltd.

- Qoo10 Japan KK

- Yodobashi Camera Co., Ltd.

- Nitori Holdings Co., Ltd.

- Oisix ra daichi Inc.

- Askul Corporation

- MonotaRO Co., Ltd.

- Caddi Inc.

- Kakaku.com Inc. (PayPay Mall)

- Shein Japan Co., Ltd.

- Shopify Japan KK

- Yamato Transport Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Silver-Economy Digital Spend in Urban Prefectures

- 4.2.2 Consolidation of 1-Hour Hyper-Local Delivery Networks in Tokyo and Osaka

- 4.2.3 Government Cashless-Subsidy Extension to 2027

- 4.2.4 Corporate Tax Incentives for B2B E-procurement Platforms

- 4.2.5 Surge in In-game and Livestream-Commerce Monetisation

- 4.2.6 Rapid Uptake of BNPL among Gen-Z Females

- 4.3 Market Restraints

- 4.3.1 Logistics Labour Shortage Beyond 2026 (Yamato "2024 Problem")

- 4.3.2 Persistent Preference for Cash-on-Delivery in Rural Shoppers

- 4.3.3 Digital-Platform Fair-Trading Act Compliance Costs

- 4.3.4 Ageing IT Infrastructure of SME Sellers

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook (Generative-AI Merchandising, AR Try-On)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on the Market

- 4.9 Key Market Trends and Share of E-commerce in Total Retail

- 4.10 Demographic Analysis (Population, Internet, Age, Income)

- 4.11 Cross-Border E-commerce Size and Trends

- 4.12 Japan's Positioning in the Asia-Pacific E-commerce Industry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Business Model

- 5.1.1 B2C

- 5.1.2 B2B

- 5.2 By Device Type (B2C)

- 5.2.1 Smartphone / Mobile

- 5.2.2 Desktop and Laptop

- 5.2.3 Other Device Types

- 5.3 By Payment Method (B2C)

- 5.3.1 Credit and Debit Cards

- 5.3.2 Digital Wallets

- 5.3.3 Buy Now Pay Later (BNPL)

- 5.3.4 Other Payment Methodss

- 5.4 By Product Category (B2C)

- 5.4.1 Beauty and Personal Care

- 5.4.2 Consumer Electronics

- 5.4.3 Fashion and Apparel

- 5.4.4 Food and Beverages

- 5.4.5 Furniture and Home

- 5.4.6 Toys, DIY and Media

- 5.4.7 Other Product Categories

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Rakuten Group, Inc.

- 6.4.2 Amazon Japan G.K.

- 6.4.3 Yahoo Japan Corporation

- 6.4.4 Mercari, Inc.

- 6.4.5 DMM.com LLC

- 6.4.6 ZOZO Inc. (ZOZOTOWN)

- 6.4.7 Apple Japan Inc.

- 6.4.8 au PAY Market (KDDI Corp.)

- 6.4.9 Maruetsu Co., Ltd.

- 6.4.10 Qoo10 Japan KK

- 6.4.11 Yodobashi Camera Co., Ltd.

- 6.4.12 Nitori Holdings Co., Ltd.

- 6.4.13 Oisix ra daichi Inc.

- 6.4.14 Askul Corporation

- 6.4.15 MonotaRO Co., Ltd.

- 6.4.16 Caddi Inc.

- 6.4.17 Kakaku.com Inc. (PayPay Mall)

- 6.4.18 Shein Japan Co., Ltd.

- 6.4.19 Shopify Japan KK

- 6.4.20 Yamato Transport Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment