PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062423

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062423

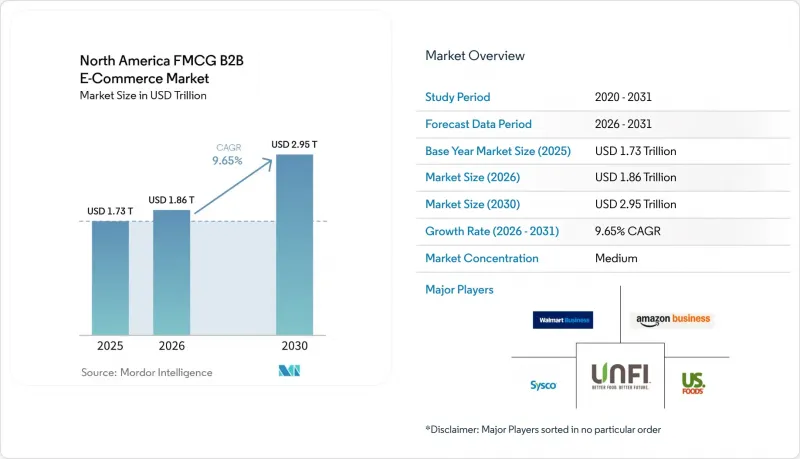

North America FMCG B2B E-Commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america fMCG b2B e-Commerce market size is projected to expand from USD 1.73 trillion in 2025 and USD 1.86 trillion in 2026 to USD 2.95 trillion by 2030, registering a CAGR of 9.65% between 2026 to 2030.

This report is Segmented by Buyer Type (Independent Retailers, Chain Supermarkets, Convenience Stores, Foodservice, Pharmacies, Quick-Commerce, Institutional Buyers), Product Category (Food & Beverage, Household, Personal Care, Health & Wellness, Pet, Baby Care), and More. Market Forecasts are in Value (USD).

North America FMCG B2B E-Commerce Market Trends and Insights

Automated Replenishment via Distributor EDI/API and E-procurement Integrations

Broadline distributors scaled digital order capture as customers replaced phone and fax with portal, EDI, and API flows, which now sustain higher on-time order rates and fewer invoice disputes. Sysco completed its SHOP rollout and reports that 80% of orders now flow through the platform, strengthening contract-price enforcement and boosting purchase frequency through order guides . Procurement suites expanded Punch-in and Punchout features so buyers can discover items in external catalogs and return cart data to native approval and PO creation, reducing rogue spend without shrinking SKU access. API-native EDI accelerates partner onboarding and improves real-time validation, reducing mapping errors before transmission and enabling event-driven updates for PO, ASN, and invoice milestones. These integrations reduce labor time, stabilize procurement controls, and increase reorder adherence at the point of need, supporting the North America FMCG B2B e-commerce market as chain and independent buyers scale digital routines across locations.

Traceability/Serialization Mandates Speeding Digital Procurement (FSMA 204, DSCSA, CFIA)Traceability/Serialization Mandates Speeding Digital Procurement (FSMA 204, DSCSA, CFIA)

The FDA's Food Traceability Rule requires electronic records of critical tracking events and key data elements for foods on the traceability list, with 24-hour retrieval, which is driving EPCIS-compliant capture, case-level identifiers, and searchable audit trails for high-risk items . EPCIS 2.0 improves standardized data exchange across suppliers, distributors, and retailers, and market-leading buyers are aligning serialization events with inbound receiving and outbound proof of delivery. Walmart's EPCIS Events API processes and publishes serialization events, enabling suppliers to transmit packing, shipping, and transformation events into a tamper-evident ledger that supports faster recalls and root-cause analysis. The DSCSA enhanced dispenser and wholesaler deadlines in 2025 pushed package-level verification and authorized trading partner checks, while recent industry datasets and notices show uneven readiness among tracked entities. Heightened enforcement activity, including published warning letters in early 2026 for lack of serialization and slow verification response, is accelerating EPCIS adoption and transaction-data readiness across drug supply chains. Canada's SFCR licensing and traceability requirements for food importers reinforce electronic documentation readiness and early license planning, which in turn influence how cross-border distributors plan renewals and compliance reviews.

Cold-Chain MOQs and Handling Fees Constrain Small-Basket Economics

Cold-chain distribution imposes minimum order quantities and accessorial fees that limit the viability of small baskets, which discourages digital replenishment for low-volume buyers. Common surcharges for multi-stop routes include layover, detention, truck-order-not-used, and extra stop fees that quickly add to landed costs for perishable shipments. Warehouse storage rates vary by temperature band and service level, with premium pricing for the frozen and ultra-low temperature ranges that put pressure on margins for sensitive categories. Reefer rates fluctuate with seasonality and equipment availability, and summer harvest windows tend to raise per-mile costs relative to winter baselines, narrowing the ROI on long-tail SKUs. Dock appointment bottlenecks compound the risk of temperature excursions during high-volume periods, potentially shortening shelf life and increasing spoilage claims for buyers and distributors. Pilots that automate appointment booking with AI agents show improved slot coverage and material time savings, which lowers dwell time and improves cold-chain reliability for order cycles.

Other drivers and restraints analyzed in the detailed report include:

- Convenience and Independent Retail Shift to Distributor Portals for SKU Breadth and Labor Savings

- Retail Media and Trade-Promo Activation Embedded in B2B Checkout

- Fragmented EDI/API Standards Across Wholesalers Slow Integrations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Foodservice operators accounted for 55.37% of buyer-type share in 2025 as digital adoption by independent restaurants and multi-location chains drove higher order cadence and fuller baskets, while convenience retailers are projected to grow at 12.76% CAGR to 2031 as mobile ordering and portal access expand assortments beyond core staples. Sysco, which completed its SHOP rollout, reports that 80% of orders are now placed through its digital platform. This level reinforces contract governance and simplifies repeat purchasing for operators that manage rotating menus and seasonality. Dispensers and pharmacies continue to align with DSCSA milestones, which sustains investments in EPCIS-based verification and ATP checks across wholesale and dispenser networks . Large institutions consolidate food, beverage, and facility needs into unified orders to reduce receiving windows and simplify accounts payable, which encourages more buyers to adopt e-procurement punchout and approval flows that keep purchases within policy. These shifts support stability in repeat categories and better long-tail access for independent retailers that rely on distributor portals to substitute for in-person cash-and-carry trips in the North America FMCG B2B e-commerce market.

Independent retail and foodservice buyers value full-catalog visibility, real-time pricing, and tighter receivables workflows, which bring control and speed without reducing selection. Pharmacy and healthcare buyers increasingly rely on item-level serialization, which heightens the need for secure data exchange and compliant audit trails across trading partners. Institutional purchasers pull facility and pantry items into the same carts used for fresh, frozen, and ambient food procurement. This pattern pushes platforms to standardize master data across categories and improve unified category navigation. These account patterns amplify network effects for platforms that serve chains and independents across foodservice, convenience, and specialty retail, which strengthens the North America FMCG B2B e-commerce industry's baseline of recurring digital spend.

List of Companies Covered in this Report:

- Amazon Business

- Walmart Business

- Costco Business Center

- Sam's Club Business

- Sysco (Sysco Shop)

- US Foods

- Gordon Food Service

- Core-Mark (Performance Food Group)

- McLane Company

- Performance Foodservice (PFG)

- C&S Wholesale Grocers

- United Natural Foods (UNFI)

- KeHE Distributors

- SpartanNash

- PepsiCo Partners

- Coca-Cola (myCoke)

- Nestle Professional

- Kraft Heinz Foodservice

- General Mills Foodservice

- Mondel?z International Foodservice

- Kimberly-Clark Professional

- Procter & Gamble Professional

- CloroxPro (The Clorox Company)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Automated replenishment via distributor EDI/API and e-procurement integrations

- 4.2.2 Traceability/serialization mandates speeding digital procurement (FSMA 204, DSCSA, CFIA)

- 4.2.3 Convenience and independent retail shift to distributor portals for SKU breadth and labor savings

- 4.2.4 Retail media and trade-promo activation embedded in B2B checkout

- 4.2.5 GS1/EPCIS 2.0 product data sharing improving case-level visibility

- 4.2.6 Automated B2B tax-exemption/resale certificate workflows reducing onboarding friction

- 4.3 Market Restraints

- 4.3.1 Cold-chain MOQs and handling fees constrain small-basket economics

- 4.3.2 Fragmented EDI/API standards across wholesalers slow integrations

- 4.3.3 SKU data quality and item-master inconsistencies cut B2B search and conversion

- 4.3.4 Tight net-terms and credit underwriting throttling SMB buyer conversion

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape (North America)

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 E-procurement integration landscape (Ariba, Coupa, SAP, Oracle, NetSuite punchout)

- 4.9 Cold-chain capacity, appointment scheduling, and slotting constraints

- 4.10 Cross-border United States-Canada-Mexico documentation and bilingual labeling

5 Market Size & Growth Forecasts (Value and Volume)

- 5.1 By Buyer Type

- 5.1.1 Independent grocery & specialty retailers

- 5.1.2 Chain supermarkets & mass merchandisers

- 5.1.3 Convenience stores & gas stations

- 5.1.4 Foodservice/HoReCa (restaurants, cafes, catering)

- 5.1.5 Pharmacies & drugstores

- 5.1.6 Online-only and quick-commerce resellers

- 5.1.7 Institutional, office & janitorial buyers

- 5.1.8 Other Buyers

- 5.2 By Product Category

- 5.2.1 Food & beverage

- 5.2.2 Household & cleaning

- 5.2.3 Personal care & beauty

- 5.2.4 OTC health & wellness

- 5.2.5 Pet care

- 5.2.6 Baby & family care

- 5.2.7 Other Products

- 5.3 By Sales Channel/Platform Type

- 5.3.1 Distributor-managed portals

- 5.3.2 CPG/supplier-direct portals

- 5.3.3 Third-party B2B marketplaces

- 5.3.4 E-procurement/API/EDI-integrated

- 5.4 By Geography (North America)

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Amazon Business

- 6.4.2 Walmart Business

- 6.4.3 Costco Business Center

- 6.4.4 Sam's Club Business

- 6.4.5 Sysco (Sysco Shop)

- 6.4.6 US Foods

- 6.4.7 Gordon Food Service

- 6.4.8 Core-Mark (Performance Food Group)

- 6.4.9 McLane Company

- 6.4.10 Performance Foodservice (PFG)

- 6.4.11 C&S Wholesale Grocers

- 6.4.12 United Natural Foods (UNFI)

- 6.4.13 KeHE Distributors

- 6.4.14 SpartanNash

- 6.4.15 PepsiCo Partners

- 6.4.16 Coca-Cola (myCoke)

- 6.4.17 Nestle Professional

- 6.4.18 Kraft Heinz Foodservice

- 6.4.19 General Mills Foodservice

- 6.4.20 Mondel?z International Foodservice

- 6.4.21 Kimberly-Clark Professional

- 6.4.22 Procter & Gamble Professional

- 6.4.23 CloroxPro (The Clorox Company)

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment