PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062422

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2062422

Germany FMCG B2B E-Commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

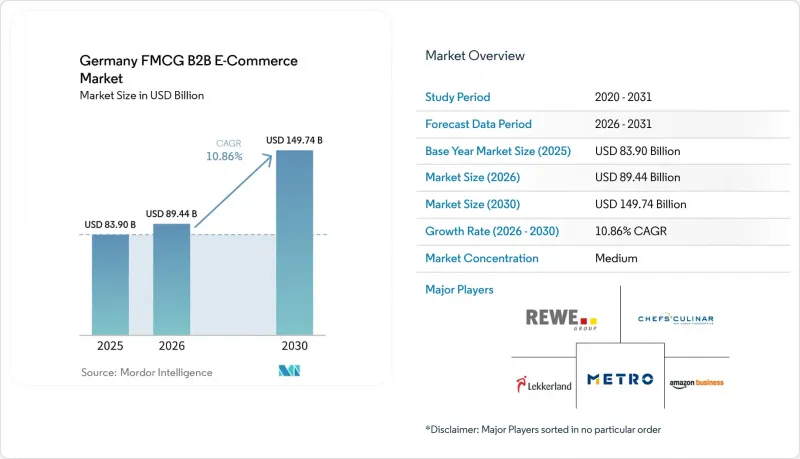

According to Mordor Intelligence, the germany fMCG b2B e-Commerce market size was valued at USD 83.90 billion in 2025 and is estimated to grow from USD 89.44 billion in 2026 to reach USD 149.74 billion by 2030, at a CAGR of 10.86% during the forecast period (2026-2030).

This report is Segmented by Buyer Type (Independent Grocery & Specialty Retailers, Chain Supermarkets & Mass Merchandisers, and More), Product Category (Food & Beverage, Household & Cleaning, and More), Sales Channel/Platform Type (Distributor-Managed Portals, and More), and Geography (Berlin, Rest of Germany). The Market Forecasts are Provided in Terms of Value (USD).

Germany FMCG B2B E-Commerce Market Trends and Insights

Mandatory B2B E-invoicing Accelerates Digitized Ordering-to-Cash and E-Procurement Integration

Germany's phased B2B e-invoicing mandate is anchoring the shift from email-PDF to structured, machine-readable formats and harmonizing invoice data quality across buyers and suppliers. The Peppol network's rapid growth, as measured by KoSIT, confirms mainstream adoption, with monthly transmissions exceeding 300,000 in early 2026, tightening validation workflows and payment approvals across large buyer ERPs. As more enterprises standardize on EN 16931-conformant formats, dispute rates fall, and receivables cycles compress, enabling suppliers to convert working capital faster while procurement gains transaction-level transparency. Momentum is reinforced by the EU's VAT in the Digital Age program, which promotes cross-border interoperability and supports transactional reporting foundations that Germany is preparing to leverage. The net effect for the Germany FMCG B2B e-commerce market is a lower-friction onboarding environment where Peppol-ready suppliers and API-first portals see higher RFP conversion and share-of-wallet wins among enterprise buyers. Early movers that invested in scalable invoice validation and metadata routing are positioned to gain recurring compliance advantages as more buyers mandate Peppol connectivity in 2026 sourcing cycles.

GS1 Germany DQX/GDSN Enforcement Raises Product Data Quality, Enabling API Catalogs and Richer B2B Search/Conversion

GS1 Germany's Data Quality Excellence (DQX) service has become a de facto gatekeeper for new consumer units syndicated via GDSN in Food and Near-Food, with broad supplier adoption and a large base of validated GTINs by mid-2025. Category coverage levels signal where distributors can expect clean, API-ready attributes, with strong penetration in detergents and confectionery and more room to grow in meat, sausage, and poultry. Release updates to the DQX Kompendium broaden visual validation and enforce mandatory communication-channel attributes in select categories, reducing manual audits and mismatches between product images and structured metadata. As distributors and marketplaces programmatically filter by certified attributes, including allergen declarations and packaging marks within GDSN payloads, B2B search relevance improves, and return rates decrease as product misunderstandings decline. Large catalogs require automated mapping to GS1 standards, as shown by AI-led attribute normalization that reconciles thousands of supplier-specific terms into target schemas at scale. For the Germany FMCG B2B e-commerce market, this codifies a quality-data premium where DQX-cleared SKUs surface higher in portal search and gain distributor preference within curated assortments.

CO2-Based Lkw-Maut and Broader Toll Scope Increase Delivery Costs, Pushing MOQs and Delivery-Fee Thresholds

Adjustments to Germany's truck toll regime and the extension to lighter commercial vehicles have raised route costs, pushing distributors to raise minimum order quantities or introduce delivery-fee thresholds to protect margins. CO2 pricing adds to fuel costs and creates additional volatility that is difficult to hedge under fixed buyer contracts, increasing the need for dynamic pricing and careful route optimization. Urban cores can absorb these costs more efficiently due to higher route density. Still, smaller cities and rural areas face longer lead times or higher delivery thresholds as runs are consolidated. Distributors have responded by embedding backhaul optimization and, where feasible, centralized pickup of deposit-bearing beverage containers, though additional toll costs can limit the economic payoff of longer detours. In practice, this has driven buyers in lower-density zones to batch orders, which impacts replenishment cycles for fast-moving perishables and requires more precise inventory planning. The short-term effect on the Germany FMCG B2B e-commerce market is a redistribution of delivery services toward dense areas, while distributors recalibrate price floors and delivery windows.

Other drivers and restraints analyzed in the detailed report include:

- Pharmacy E-Prescription (E-Rezept) Mainstreaming Increases Digital OTC/Near-Pharmacy B2B Replenishment

- API/EDI/Peppol Readiness Among Larger Buyers Reduces Onboarding Frictions and Shifts Spend to Digital Channels

- SME Digitization Gaps (Structured E-Invoice Reception, Clean Master Data) Slow Long-Tail Digital Uptake

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Foodservice and HoReCa buyers accounted for 54.37% of the 2025 value, reflecting the scale and order frequency that restaurants, hotels, and caterers drive in B2B replenishment across ambient, chilled, and frozen staples. This buyer set also uses structured e-invoicing and portal-based ordering more often than the long tail, which increases order accuracy and compresses receivables cycles for distributors that can expose real-time inventory and pricing via APIs. In parallel, online-only and quick-commerce resellers are projected to post an 11.55% CAGR through 2031 as dark-store networks originally built for consumer grocery expand their professional-buyer assortments and delivery time windows. Pharmacies and drugstores benefit from E-Rezept adoption and associated platform integrations, which improve signal fidelity for OTC replenishment and drive higher digital order shares across adjacent personal care and wellness categories. Larger retail chains standardize purchasing through API, EDI, or Peppol connections and expect machine-readable endpoints, while independent stores and kiosks adopt at a slower pace, which sustains the need for hybrid, phone-to-portal workflows during the transition. These patterns combine to deepen the Germany FMCG B2B e-commerce market's reliance on digital-first buyer cohorts, even as distributors maintain analog order capture for late adopters.

The Germany FMCG B2B e-commerce market share held by Foodservice and HoReCa in 2025 underscores how route density, product breadth, and portal adoption reinforce one another in this buyer group. For quick-commerce operators, the Germany FMCG B2B e-commerce market size for professional buyers is set to rise alongside new buyer services, such as consolidated invoicing and curated wholesale packs, which improve economics at case and pallet quantities. Pharmacy cooperatives and larger drugstore formats are using e-prescription volumes to tune demand models and raise the productivity of wholesale interfaces, with evidence from national platforms that aggregate e-prescriptions and integrate with medication lists. Across buyer types, Peppol-connected procurement and API catalogs reduce onboarding friction and error rates, encouraging buyers to consolidate suppliers onto a smaller set of compliant portals and marketplaces. As coverage expands, distributors that can validate invoices, surface certified attributes, and align delivery promises by buyer segment will capture a greater share of wallet in the Germany FMCG B2B e-commerce market.

List of Companies Covered in this Report:

- METRO Deutschland

- Transgourmet Deutschland (food@service/Warenshop)

- EDEKA Foodservice

- Lekkerland (REWE)

- CHEFS CULINAR

- Amazon Business Germany

- PHOENIX Pharmahandel

- NOWEDA

- Sanacorp

- Service-Bund

- Intergast network

- Hamberger Grobmarkt

- Rullko

- Bartels-Langness/bela c+c

- Unite/Mercateo

- Wucato Marketplace GmbH

- zentrada

- Faire

- Ankorstore

- Nestle Professional

- Unilever Food Solutions

- Coca-Cola Europacific Partners

- Nespresso Professional

- Essity Tork EasyOrder

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory B2B e-invoicing (2025-2028) accelerates digitized ordering-to-cash and e-procurement integration

- 4.2.2 GS1 Germany DQX/GDSN enforcement raises product data quality, enabling API catalogs and richer B2B search/conversion

- 4.2.3 Pharmacy e-prescription (E?Rezept) mainstreaming increases digital OTC/near?pharmacy B2B replenishment

- 4.2.4 Distributor portals' dominance and marketplace expansion in B2B internet trade lift FMCG e?commerce penetration

- 4.2.5 API/EDI/Peppol readiness among larger buyers reduces onboarding frictions and shift spend to digital channels

- 4.2.6 Supplier-direct professional portals (foodservice, beverages, hygiene) widen SKUs and promos for B2B buyers

- 4.3 Market Restraints

- 4.3.1 CO2-based Lkw-Maut and broader toll scope increase delivery costs, pushing MOQs and delivery-fee thresholds

- 4.3.2 SME digitization gaps (structured e-invoice reception, clean master data) slow long?tail digital uptake

- 4.3.3 Reverse logistics and compliance complexity for DPG deposit handling in beverages strains small buyers

- 4.3.4 Cold-chain/HACCP operational constraints limit delivery windows and same?day expansion for perishables

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Food Safety & Cold-Chain Compliance

- 4.8 Logistics & Last-mile Considerations

- 4.9 Porter's Five Forces

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Buyer Type

- 5.1.1 Independent grocery & specialty retailers

- 5.1.2 Chain supermarkets & mass merchandisers

- 5.1.3 Convenience stores & gas stations

- 5.1.4 Foodservice/HoReCa (restaurants, cafes, catering)

- 5.1.5 Pharmacies & drugstores

- 5.1.6 Online-only and quick-commerce resellers

- 5.1.7 Institutional, office & janitorial buyers

- 5.1.8 Other Products

- 5.2 By Product Category

- 5.2.1 Food & beverage

- 5.2.2 Household & cleaning

- 5.2.3 Personal care & beauty

- 5.2.4 OTC health & wellness

- 5.2.5 Pet care

- 5.2.6 Baby & family care

- 5.2.7 Other Products

- 5.3 By Sales Channel/Platform Type

- 5.3.1 Distributor-managed portals

- 5.3.2 CPG/supplier-direct portals

- 5.3.3 Third-party B2B marketplaces

- 5.3.4 E-procurement/API/EDI-integrated

- 5.4 By Geography

- 5.4.1 Berlin

- 5.4.2 Hamburg

- 5.4.3 Nordrhein-Westfalen

- 5.4.4 Rest of Germany

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 METRO Deutschland

- 6.4.2 Transgourmet Deutschland (food@service/Warenshop)

- 6.4.3 EDEKA Foodservice

- 6.4.4 Lekkerland (REWE)

- 6.4.5 CHEFS CULINAR

- 6.4.6 Amazon Business Germany

- 6.4.7 PHOENIX Pharmahandel

- 6.4.8 NOWEDA

- 6.4.9 Sanacorp

- 6.4.10 Service-Bund

- 6.4.11 Intergast network

- 6.4.12 Hamberger Grobmarkt

- 6.4.13 Rullko

- 6.4.14 Bartels-Langness/bela c+c

- 6.4.15 Unite/Mercateo

- 6.4.16 Wucato Marketplace GmbH

- 6.4.17 zentrada

- 6.4.18 Faire

- 6.4.19 Ankorstore

- 6.4.20 Nestle Professional

- 6.4.21 Unilever Food Solutions

- 6.4.22 Coca-Cola Europacific Partners

- 6.4.23 Nespresso Professional

- 6.4.24 Essity Tork EasyOrder

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment