PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043835

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043835

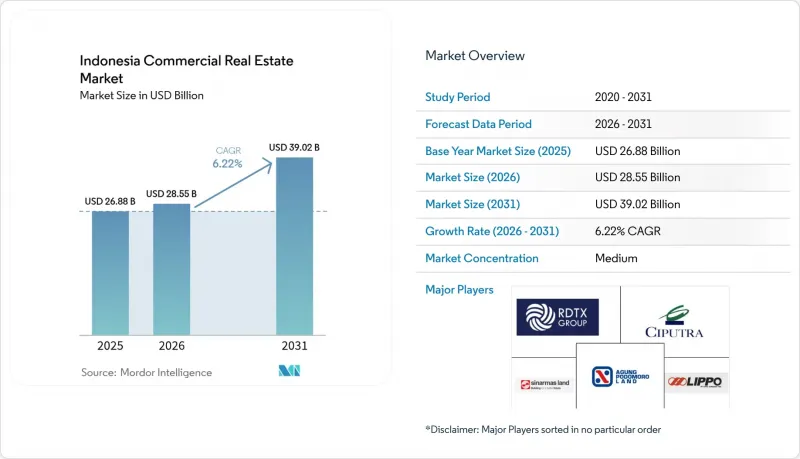

Indonesia Commercial Real Estate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Indonesia commercial real estate market size is projected to expand from USD 26.88 billion in 2025 and USD 28.55 billion in 2026 to USD 39.02 billion by 2031, registering a CAGR of 6.22% between 2026 and 2031.

Demand is rotating toward logistics warehouses, hyperscale data-center campuses, and mixed-use projects linked to the Nusantara capital relocation, while traditional Grade-A offices in Jakarta face double-digit vacancy. Developers are responding by converting underused towers into flexible workplaces, pursuing EDGE or LEED certifications to secure rental premiums, and partnering with energy providers to guarantee power resilience for digital-infrastructure tenants. Investment momentum is strongest along new toll-road corridors and in secondary cities where land remains inexpensive but accessibility has improved. Capital-market liquidity favors sale-leaseback and REIT structures that let sponsors recycle equity quickly into growth assets.

Indonesia Commercial Real Estate Market Trends and Insights

Relocation of National Capital to Nusantara Catalyzing Office and Mixed-Use Development

Government ministries plan to begin phased moves into Nusantara during late 2026, anchoring a pipeline of purpose-built Grade-A offices, hotels, and civic amenities. Land acquisition inside the 256,000-hectare core accelerated in early 2025, with leading developers locking in parcels at discounts that should crystallize once supporting ports and power grids are delivered. Pre-leasing reached 18% of planned inventory by December 2025, signaling cautious but real tenant commitment. Jakarta landlords are reacting by converting partially vacant floors into coworking suites to offset outflows. Taken together, the two cities will operate as a dual-hub system that increases total national office demand over the medium term.

Expansion of E-Commerce and 3PL Fueling Logistics and Warehouse Uptake

Indonesia's online-shopping GMV topped USD 77 billion in 2025, pushing 3PLs to add high-throughput cross-docks and city-edge fulfillment centers within two-day trucking distance of 200 million consumers. Average warehouse lease tenures now span 5-7 years, twice office norms, giving landlords predictable cash flows. Automated sortation hubs announced by SiCepat alone will raise national Grade-A logistics stock by nearly 450,000 m2 before 2027. Cold-chain footprints are expanding fastest, and facilities with pharma-grade temperature control secure up to 30% rent premiums over ambient space. Accelerated customs clearance, cut to 48 hours in 2024, further incentivizes merchants to keep inventory onshore rather than in Singapore.

Persistently High Vacancy and Falling Effective Rents in Jakarta CBD Offices

Grade-A vacancy in Jakarta's central business district climbed to 23.7% in December 2025, as multinational tenants compressed floorplates in response to hybrid work. Effective rents fell 9% year-on-year once inducements like rent-free periods were netted, eroding landlord yields. Older non-certified towers bear the brunt, prompting owners to repurpose top floors for serviced apartments or coworking spaces. Net absorption of 180,000 m2 per year implies the oversupply could persist until 2028. Investors now price a clear premium for green-compliant buildings that consistently post sub-12% vacancies.

Other drivers and restraints analyzed in the detailed report include:

- Connectivity Megaprojects Unlocking Peripheral Land Banks

- REIT Tax Incentives Accelerating Institutional Investment Flows

- FX Volatility and Higher USD Funding Costs Squeezing Developer Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Offices captured 39.45% of the Indonesia commercial real estate market share in 2025, maintaining numerical leadership even as leasing momentum tilts toward logistics parks. The Indonesia commercial real estate market size tied to office stock is stabilizing as owners convert excess floors into data-center shells or serviced workspaces. Logistics facilities, meanwhile, are forecast to grow at a 9.12% CAGR through 2031, lifted by e-commerce, regional trade pacts, and cold-chain mandates. Demand for hyperscale data-center land within industrial estates reveals how digital infrastructure is morphing the traditional industrial category.

Rapid cycle-time requirements have spawned micro-fulfillment "dark stores" embedded in residential districts, blurring lines between retail and logistics. Data-center campuses secure 10-15-year triple-net leases that shift operating risk to tenants, appealing to yield-hungry institutions. Retail footprints, though pressured by online shopping, are reinventing themselves through experiential formats such as food halls and entertainment hubs, which logged footfall-recovery rates above 90% of pre-pandemic levels by late 2025. Hospitality and cold-storage assets under the "Others" label benefit from tourism rebound and pharmaceutical distribution, respectively, providing diversification options for developers traditionally wedded to office pipelines.

The Indonesia Commercial Real Estate Market Report is Segmented by Property Type (Offices, Retail, Logistics, Others), by Business Model (Sales, Rental), by End-User (Individuals/Households, Corporates & SMEs, Others), and by Geography (Jakarta, Surabaya, Bandung, Semarang, Medan, Rest of Indonesia). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Sinarmas Land

- Agung Podomoro Land

- Lippo Karawaci

- Ciputra Development

- RDTX Group

- PP Properti

- Summarecon Agung

- Triniti Land

- Colliers Indonesia

- JLL Indonesia

- CBRE Indonesia

- Cushman & Wakefield Indonesia

- Knight Frank Indonesia

- Coldwell Banker Commercial ID

- CoHive

- GoWork

- UnionSpace

- Carigudang

- SpaceStock

- Pinhome

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Commercial Real-Estate Buying Trends - Socio-economic & Demographic Insights

- 4.3 Rental Yield Analysis

- 4.4 Capital-Market Penetration & REIT Presence

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Insights into Existing and Upcoming Projects

- 4.8 Market Drivers

- 4.8.1 Relocation of the national capital to Nusantara catalysing office & mixed-use development (mainstream)

- 4.8.2 Expansion of e-commerce & 3PL fuelling logistics / warehouse uptake (mainstream)

- 4.8.3 Connectivity megaprojects (toll-roads, ports & rail) unlocking peripheral land banks (mainstream)

- 4.8.4 Surging demand for hyperscale data-centre campuses and edge facilities (mainstream)

- 4.8.5 Stricter municipal green-building codes driving retrofit and premium-rent opportunities (under-reported)

- 4.8.6 Cold-chain & flexible manufacturing growth in secondary cities boosting specialised industrial parks (under-reported)

- 4.9 Market Restraints

- 4.9.1 Persistently high vacancy and falling effective rents in Jakarta CBD offices (mainstream)

- 4.9.2 FX volatility and higher USD funding costs squeezing developer margins (mainstream)

- 4.9.3 Uncertain funding timeline for Nusantara causing speculative land bubbles & investor hesitancy (under-reported)

- 4.9.4 Escalating climate-risk premiums (flooding & subsidence) on coastal assets elevating insurance & lender requirements (under-reported)

- 4.10 Value / Supply-Chain Analysis

- 4.10.1 Overview

- 4.10.2 Real-Estate Developers & Contractors - Key Quantitative and Qualitative Insights

- 4.10.3 Real-Estate Brokers & Agents - Key Quantitative and Qualitative Insights

- 4.10.4 Property-Management Companies - Key Quantitative and Qualitative Insights

- 4.10.5 Insights on Valuation Advisory & Other Real-Estate Services

- 4.10.6 State of the Building-Materials Industry and Partnerships with Key Developers

- 4.10.7 Insights on Key Strategic Real-Estate Investors / Buyers in the Market

- 4.11 Industry Attractiveness - Porter's Five-Forces Analysis

- 4.11.1 Threat of New Entrants

- 4.11.2 Bargaining Power of Buyers / Occupiers

- 4.11.3 Bargaining Power of Suppliers (Developers / Builders)

- 4.11.4 Threat of Substitutes

- 4.11.5 Competitive Rivalry Intensity

5 Market Size & Growth Forecasts (Value, USD Billion)

- 5.1 By Property Type

- 5.1.1 Offices

- 5.1.2 Retail

- 5.1.3 Logistics

- 5.1.4 Others

- 5.2 By Business Model

- 5.2.1 Sales

- 5.2.2 Rental

- 5.3 By End-user

- 5.3.1 Individuals / Households

- 5.3.2 Corporates & SMEs

- 5.3.3 Others

- 5.4 By Geography

- 5.4.1 Jakarta

- 5.4.2 Surabaya

- 5.4.3 Bandung

- 5.4.4 Semarang

- 5.4.5 Medan

- 5.4.6 Rest of Indonesia

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Sinarmas Land

- 6.4.2 Agung Podomoro Land

- 6.4.3 Lippo Karawaci

- 6.4.4 Ciputra Development

- 6.4.5 RDTX Group

- 6.4.6 PP Properti

- 6.4.7 Summarecon Agung

- 6.4.8 Triniti Land

- 6.4.9 Colliers Indonesia

- 6.4.10 JLL Indonesia

- 6.4.11 CBRE Indonesia

- 6.4.12 Cushman & Wakefield Indonesia

- 6.4.13 Knight Frank Indonesia

- 6.4.14 Coldwell Banker Commercial ID

- 6.4.15 CoHive

- 6.4.16 GoWork

- 6.4.17 UnionSpace

- 6.4.18 Carigudang

- 6.4.19 SpaceStock

- 6.4.20 Pinhome

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment