PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044010

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044010

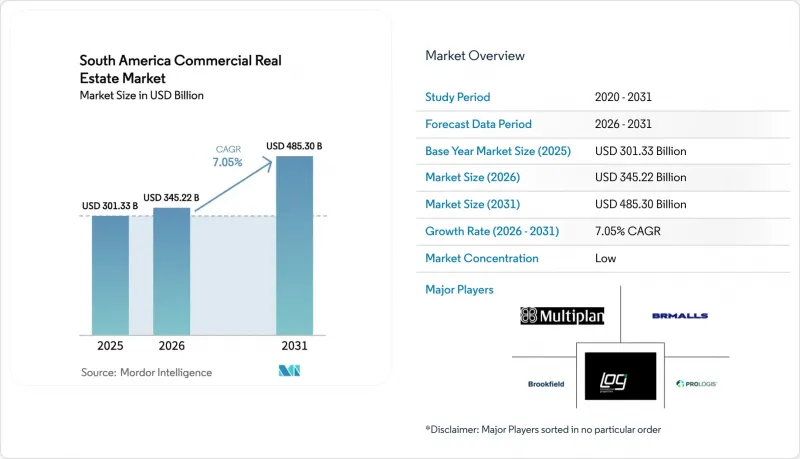

South America Commercial Real Estate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The South America commercial real estate market size was valued at USD 301.33 billion in 2025 and estimated to grow from USD 345.22 billion in 2026 to reach USD 485.3 billion by 2031, at a CAGR of 7.05% during the forecast period (2026-2031).

Supply-chain re-routing from Asia, sovereign data-residency rules, and national hydrogen strategies are reshaping investment flows toward ports, inland logistics corridors, and hyperscale data-center campuses. Institutional buyers continue to gravitate to income-producing logistics assets, while a resurgence in office leasing, supported by metro extensions and zoning reforms, has narrowed prime-CBD vacancy to the mid-teens. Rising catastrophe-insurance costs and double-digit local-currency interest rates remain the chief headwinds, but regulatory streamlining in Chile and Peru is starting to compress permitting calendars and unlock shovel-ready inventory.

South America Commercial Real Estate Market Trends and Insights

China-plus-one Manufacturing Shift Fuels New Logistics Clusters

Global automakers and electronics firms are redistributing capacity from coastal China to Brazil's Northeast and Chile's Central Region, driving conversion of farmland into Grade A cross-dock parks. Anchor tenants such as BYD (Bahia) and Great Wall Motors (Sao Paulo) have signed long-term leases, prompting speculative developers to pre-grade secondary sites that sit within two hours of deep-water ports. Vacancy in these corridors has fallen below 6%, and average take-up periods have shortened to six months, half the 2023 cycle time.

Accelerating E-commerce Lifts Warehouse and Cold-chain Demand

Online retail penetration exceeded 15% of overall South American sales in 2025, yet less than one-quarter of existing sheds offer clear heights above 12 m or automated sortation. Platforms such as Mercado Libre committed over USD 135 million to a new Santiago fulfillment hub able to process 75,000 parcels per hour. Parallel cold-chain investments from Emergent Cold LatAm are integrating export seafood and domestic grocery flows under single roofs, tightening the South America commercial real estate market for temperature-controlled space.

Macroeconomic Volatility and FX Swings Crimp Underwriting

Brazil's Selic reached 12.25% in early 2026 and may touch 15% by mid-year, widening debt-service coverage gaps for leveraged deals. The real lost 12% against the USD from 2024-2025, eroding unhedged equity returns. Foreign investors increasingly structure joint ventures with local operators that can access subsidized BNDES lines or peso-denominated debt to stabilize capital stacks.

Other drivers and restraints analyzed in the detailed report include:

- Tourism Rebound Revives Hospitality-anchored Mixed-use Schemes

- Port, Metro, and Highway Upgrades Unlock Developable Corridors

- Fragmented Permitting and Land-title Regimes Delay Starts

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Logistics and industrial parks retained a commanding 32.22% share of the South America commercial real estate market size in 2025. Prime last-mile facilities inside 30 km urban rings repeatedly traded at sub-7% stabilized yields, underscoring the scarcity premium. Office inventory, though smaller, is slated to post a 9.50% CAGR over 2026-2031 as vacancy in Sao Paulo's CBD fell from 20.8% in 2024 to 15.9% in 2025. Trophy towers near new metro stops achieved double-digit rent growth, signaling a flight to quality.

Developers are adding wellness features, biophilic terraces, and low-carbon materials to future office pipelines, differentiating them from retrofit-challenged stock. Meanwhile, cold-chain sub-segments inside the broader logistics slate command a 25-30% rental premium and often transact via long-term sale-and-leasebacks with grocery and pharma tenants, widening the investable universe within the South America commercial real estate market.

The South America Commercial Real Estate Market Report is Segmented by Property Type (Offices, Retail, Logistics and More), by Business Model (Sales, Rental/Leasing), by End-User (Individuals/Households, Corporates & SMEs and More), and by Geography (Brazil, Argentina, Chile, Colombia, Peru, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Brookfield Asset Management

- BR Malls Participacoes

- Multiplan Empreendimentos

- Prologis

- LOG Commercial Properties

- Cyrela Commercial Properties

- Iguatemi S.A.

- JHSF Participacoes

- Sonae Sierra Brasil

- Aliansce Sonae Shopping Centers

- Parque Arauco

- PLAZA S.A.

- Grupo Patio

- VivoCorp

- Terranum (PEI)

- Inversiones Centenario

- IRSA Propiedades Comerciales

- GLP (Global Logistic Properties)

- Tishman Speyer

- HSI (Hemisferio Sul Investimentos)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Commercial Real Estate Buying Trends - Socio-economic & Demographic Insights

- 4.3 Rental Yield Analysis

- 4.4 Capital-Market Penetration & REIT Presence

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Insights into Existing and Upcoming Projects

- 4.8 Market Drivers

- 4.8.1 China-plus-one reshoring wave lifting Brazilian & Andean logistics parks

- 4.8.2 E-commerce boom accelerating demand for modern warehousing & cold chain

- 4.8.3 Tourism rebound & experiential retail reviving hospitality / mixed-use assets

- 4.8.4 Infrastructure upgrades (ports, metros, highways) unlocking new corridors

- 4.8.5 Hyperscale & edge data-centre build-out in Sao Paulo/Santiago creating niche assets

- 4.8.6 Green-hydrogen export hubs (Chile, NE Brazil) spurring industrial clusters

- 4.9 Market Restraints

- 4.9.1 Macroeconomic volatility & FX swings complicating underwriting & funding

- 4.9.2 Regulatory, permitting & land-title complexity across countries & cities

- 4.9.3 Construction-cost inflation & high financing rates squeezing project IRRs

- 4.9.4 Climate-driven disaster risk (floods, droughts) raising insurance premiums

- 4.10 Value / Supply-Chain Analysis

- 4.10.1 Overview

- 4.10.2 Real Estate Developers and Contractors - Key Quantitative and Qualitative Insights

- 4.10.3 Real Estate Brokers and Agents - Key Quantitative and Qualitative Insights

- 4.10.4 Property Management Companies - Key Quantitative and Qualitative Insights

- 4.10.5 Insights on Valuation Advisory and Other Real Estate Services

- 4.10.6 State of the Building Materials Industry and Partnerships with Key Developers

- 4.10.7 Insights on Key Strategic Real Estate Investors/Buyers in the Market

- 4.11 Porters Five Forces

- 4.11.1 Threat of New Entrants

- 4.11.2 Bargaining Power of Suppliers

- 4.11.3 Bargaining Power of Buyers

- 4.11.4 Threat of Substitutes

- 4.11.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Property Type

- 5.1.1 Offices

- 5.1.2 Retail

- 5.1.3 Logistics

- 5.1.4 Others

- 5.2 By Business Model

- 5.2.1 Sales

- 5.2.2 Rental/Leasing

- 5.3 By End-user

- 5.3.1 Individuals / Households

- 5.3.2 Corporates & SMEs

- 5.3.3 Others

- 5.4 By Country

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Chile

- 5.4.4 Colombia

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Brookfield Asset Management

- 6.4.2 BR Malls Participacoes

- 6.4.3 Multiplan Empreendimentos

- 6.4.4 Prologis

- 6.4.5 LOG Commercial Properties

- 6.4.6 Cyrela Commercial Properties

- 6.4.7 Iguatemi S.A.

- 6.4.8 JHSF Participacoes

- 6.4.9 Sonae Sierra Brasil

- 6.4.10 Aliansce Sonae Shopping Centers

- 6.4.11 Parque Arauco

- 6.4.12 PLAZA S.A.

- 6.4.13 Grupo Patio

- 6.4.14 VivoCorp

- 6.4.15 Terranum (PEI)

- 6.4.16 Inversiones Centenario

- 6.4.17 IRSA Propiedades Comerciales

- 6.4.18 GLP (Global Logistic Properties)

- 6.4.19 Tishman Speyer

- 6.4.20 HSI (Hemisferio Sul Investimentos)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment