PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044017

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044017

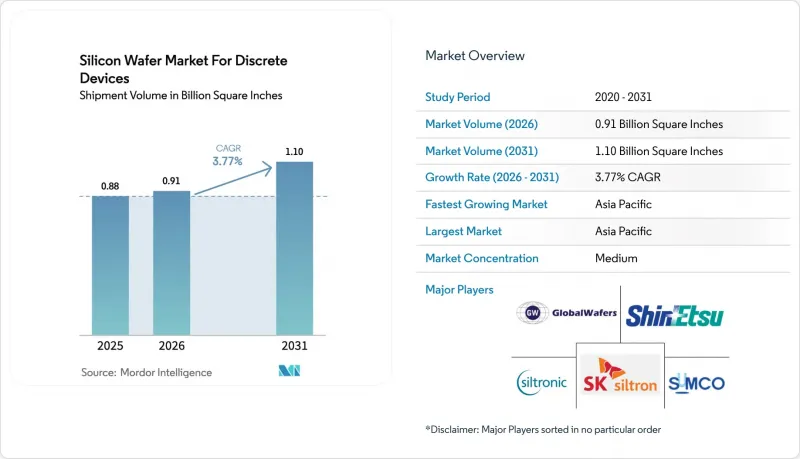

Silicon Wafer For Discrete Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The silicon wafer market size for discrete devices was valued at 0.88 billion square inches in 2025 and is estimated to grow from 0.91 billion square inches in 2026 to reach 1.10 billion square inches by 2031, at a CAGR of 3.77% during the forecast period (2026-2031).

Demand pivots toward power-oriented substrates as battery-electric vehicles, renewable-energy inverters, and factory-automation drives require higher current ratings than legacy consumer electronics. Government subsidies under the United States CHIPS and Science Act, the European Chips Act, and China's third Integrated Circuit Fund are accelerating 200 millimeter line additions, compressing equipment payback periods and intensifying supplier competition. Polysilicon spot-price recovery to USD 8-9 per kilogram in early 2025 injected margin volatility, prompting wafer suppliers to embed index-based escalators in long-term contracts. Automotive electrification now anchors substrate allocation, with per-vehicle discrete content tripling to more than 1 200 units in battery-electric platforms, and industrial-motor-drive retrofits add a second structural leg to volume growth. Simultaneously, export-control regimes that restrict advanced deposition and lithography tools to China are bifurcating supply chains, extending lead times for non-Chinese buyers, and motivating multinational OEMs to dual-source wafers across regions.

Insights and Trends of Silicon Wafer Market For Discrete Devices

Expansion Of EV Fast-Charging Infrastructure Requiring High-Current Diodes

Ultra-fast chargers rated at 350 kilowatts now dominate highway corridors in China, Europe, and the United States, and each installation consumes 8-12 discrete diodes rated for 1 200-1 700 volts and more than 100 amperes. Wolfspeed unveiled a 200 millimeter SiC-on-silicon epitaxial platform in February 2025 that targets these rectifier stages and demonstrates how wafer metrics such as bow, warp, and defect density must tighten when surge-current requirements rise. China's State Grid added 120 000 ultra-fast chargers in 2025, translating to incremental demand for roughly 15-20 million square inches of high-current-diode substrates. The European Union's Alternative Fuels Infrastructure Regulation mandates interoperable charging networks by 2027, locking in discrete-heavy Combined Charging System protocols. Higher switching frequencies above 50 kilohertz are shifting preference toward SiC Schottky diodes on high-resistivity silicon, a trend that lifts specialty-substrate volumes ahead of prime polished grades.

Adoption Of GaN/SiC Hybrid Modules Increasing Demand For High-Resistivity Silicon Substrates

Hybrid power modules that co-package GaN HEMTs with SiC diodes on high-resistivity silicon offer cost-per-watt metrics 30-40% below monolithic SiC, enabling automakers to meet USD 0.15 per watt system targets. Infineon's CoolSiC devices, released in March 2024, ride this architecture and already ship on 200 millimeter wafers specified at 1 000-10 000 ohm-centimeters. STMicroelectronics reported a 28% revenue jump in hybrid modules during 2024, with 65% of units sold to automotive customers, underscoring the commercial traction of these substrates. Japan's Ministry of Economy, Trade and Industry allocated JPY 45 billion (USD 307 million) in fiscal 2025 to subsidize domestic production of high-resistivity silicon, explicitly linking national policy to automotive power electronics. GaN on silicon for 650 volt devices requires 111 crystal orientation with threading-dislocation density under 10^6 cm-2, capabilities delivered only by specialty-wafer suppliers, reinforcing supply-chain entry barriers.

Price Volatility Of Polysilicon And Energy Costs

Polysilicon prices swung from USD 6 to USD 35 per kilogram between 2022 and 2025, and although early-2025 spot levels rebounded to USD 8-9 per kilogram, long-term contracts hover at USD 11-13, squeezing merchant wafer margins. European producers face electricity tariffs averaging EUR 0.18 per kilowatt-hour (USD 0.20 per kilowatt-hour), triple 2019 levels, and crystal growth consumes roughly 225 kilowatt-hours per kilogram of ingot, magnifying exposure. Chinese provinces offset energy intensity with subsidized industrial rates as low as CNY 0.35 per kilowatt-hour (USD 0.05), while the United States Inflation Reduction Act's production credit refunds USD 0.03 per kilowatt-hour for clean-energy use. Supply concentration among five polysilicon vendors amplifies volatility, forcing wafer suppliers to incorporate pass-through clauses or risk negative gross margins during spikes.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives For Domestic Discrete Component Manufacturing

- Mature Power Semiconductor Replacement With High-Voltage Discrete Devices

- Prolonged Downcycles In Consumer Electronics Affecting Low-Power Discrete Consumption

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 200 millimeter slice held 59.66% of the silicon wafer market share in 2025, anchored by fully depreciated fab assets whose cost-per-die remains unbeatable for discrete transistors and diodes. Automotive-qualified fabs in Japan, Czech Republic, and Malaysia run 90%-plus utilization because this diameter balances throughput with product-mix flexibility. 300 millimeter substrates account for only 24% of the silicon wafer market size but are forecast to grow 4.52% annually through 2031 as integrated power-management ICs and multi-chip analog modules migrate to larger wafers to spread lithography overhead across hundreds of die. Texas Instruments will dedicate 40% of its Richardson Fab output to analog and power, backstopping demand for 300 millimeter supply.

The up-to-150 millimeter tier persists in niche RF-diode, thyristor, and sensor markets where exotic crystal orientations justify smaller diameters. SEMI projects 200 millimeter shipments across all semiconductor segments to decline 1.2% annually through 2028, yet discrete-device demand partially offsets this bleed by absorbing capacity vacated by memory and MCU production. Supply-chain resiliency concerns are also pushing automotive OEMs to dual-source 200 millimeter wafers from both Japan and China, creating regional hedges against seismic or geopolitical events.

The Silicon Wafer Market for Discrete Devices Report is Segmented by Wafer Diameter (Up To 150mm, 200mm, and 300mm), Wafer Type (Prime Polished, Epitaxial, Silicon-On-Insulator, and Specialty Silicon), End-User (Consumer Electronics, Industrial, Telecommunications, Automotive, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Volume (Square Inches).

Geography Analysis

Asia-Pacific commanded 81.84% of 2025 volume and is expected to grow at a 4.79% CAGR through 2031 as Japan, Taiwan, and China scale 200 millimeter capacity. Shin-Etsu Chemical and SUMCO shipped more than 450 million square inches combined in 2024, leveraging proprietary Czochralski techniques for resistivity uniformity within +-5%. Taiwan's GlobalWafers dedicated 35% of 2024 output to discrete customers, using long-term contracts with onsemi and Vishay to run utilization above 85%. Chinese suppliers NSIG and Zhonghuan added 80 million square inches of 200 millimeter capacity during 2024-2025, bolstered by CNY 8 billion (USD 1.1 billion) in provincial subsidies.

North America accounted for 8% in 2025. CHIPS Act funding of USD 400 million is underwriting GlobalWafers' new Texas fab that will reserve 40% of its 300 millimeter output for power discretes starting 2027. Hemlock Semiconductor's USD 325 million polysilicon expansion in Michigan further localizes upstream supply and insulates U.S. wafer lines from Chinese feedstock risk, though ramp will not complete until 2029.

Europe held 6% of output, with Siltronic AG and Soitec serving automotive hubs in Germany and France via epitaxial and SOI lines. Important Project of Common European Interest approval enabled EUR 700 million (USD 791 million) for a power-discrete pilot line supporting STMicroelectronics, Infineon, and onsemi, but commercial production is unlikely before 2028. South America and the Middle East and Africa combined for less than 5%, relying on imported wafers for assembly and test facilities.

The heavy concentration of substrate production within 100 kilometers of Taiwan's west coast exposes the silicon wafer market to earthquake and geopolitical disruptions. Automotive OEMs increasingly mandate dual-regional sourcing, pairing Japanese or Taiwanese supply with backup capacity in the United States or Europe to mitigate single-point-of-failure risk.

- Shin-Etsu Chemical Co Ltd

- SUMCO Corporation

- GlobalWafers Co Ltd

- Siltronic AG

- SK siltron Co Ltd

- Soitec SA

- Wafer Works Corporation

- Okmetic Oy

- National Silicon Industry Group Co Ltd

- Hangzhou Semiconductor Wafer Co Ltd

- Beijing ESWIN Semiconductor Technology Co Ltd

- Ferrotec Holdings Corporation

- Hebei Puxing Electronic Technology Co Ltd

- Fujian Jinghui Semiconductor Co Ltd

- Wafertech International

- Mitsubishi Materials Corporation

- Topsil Semiconductor Materials A/S

- Zhonghuan Advanced Semiconductor Materials Co

- Tianjin Huanou International Silicon Technology

- Linton Crystal Technologies

- Siltronix ST

- GRINM Semiconductor Materials Co Ltd

- Zhejiang Jinruihong Technology Co Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Impact of Macroeconomic Factors

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Market Drivers

- 4.6.1 Mature Power Semiconductor Replacement with High-Voltage Discrete Devices

- 4.6.2 Expansion of EV Fast-Charging Infrastructure Requiring High-Current Diodes

- 4.6.3 Adoption of GaN/SiC Hybrid Modules Increasing Demand for High-Resistivity Silicon Substrates

- 4.6.4 Government Incentives for Domestic Discrete Component Manufacturing

- 4.6.5 Rising Demand for Power Management ICs in IoT Edge Devices

- 4.6.6 Supply Chain Localization Mandates in Automotive Sector

- 4.7 Market Restraints

- 4.7.1 Prolonged Downcycles in Consumer Electronics Affecting Low-Power Discrete Consumption

- 4.7.2 Price Volatility of Polysilicon and Energy Costs

- 4.7.3 Technical Limits of Silicon for Ultra-High Voltage Switching (>10 kV)

- 4.7.4 Geopolitical Export Controls on Advanced Wafer Manufacturing Equipment

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Wafer Diameter

- 5.1.1 Up to 150mm

- 5.1.2 200 mm

- 5.1.3 300 mm

- 5.2 By Wafer Type

- 5.2.1 Prime Polished

- 5.2.2 Epitaxial

- 5.2.3 Silicon-on-Insulator (SOI)

- 5.2.4 Specialty Silicon (High-Resistivity, Power, Sensor-Grade)

- 5.3 By End-user

- 5.3.1 Consumer Electronics

- 5.3.1.1 Mobile and Smartphones

- 5.3.1.2 PCs and Servers

- 5.3.2 Industrial

- 5.3.3 Telecommunications

- 5.3.4 Automotive

- 5.3.5 Other End-user Applications

- 5.3.1 Consumer Electronics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Taiwan

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Shin-Etsu Chemical Co Ltd

- 6.4.2 SUMCO Corporation

- 6.4.3 GlobalWafers Co Ltd

- 6.4.4 Siltronic AG

- 6.4.5 SK siltron Co Ltd

- 6.4.6 Soitec SA

- 6.4.7 Wafer Works Corporation

- 6.4.8 Okmetic Oy

- 6.4.9 National Silicon Industry Group Co Ltd

- 6.4.10 Hangzhou Semiconductor Wafer Co Ltd

- 6.4.11 Beijing ESWIN Semiconductor Technology Co Ltd

- 6.4.12 Ferrotec Holdings Corporation

- 6.4.13 Hebei Puxing Electronic Technology Co Ltd

- 6.4.14 Fujian Jinghui Semiconductor Co Ltd

- 6.4.15 Wafertech International

- 6.4.16 Mitsubishi Materials Corporation

- 6.4.17 Topsil Semiconductor Materials A/S

- 6.4.18 Zhonghuan Advanced Semiconductor Materials Co

- 6.4.19 Tianjin Huanou International Silicon Technology

- 6.4.20 Linton Crystal Technologies

- 6.4.21 Siltronix ST

- 6.4.22 GRINM Semiconductor Materials Co Ltd

- 6.4.23 Zhejiang Jinruihong Technology Co Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment