PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065436

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065436

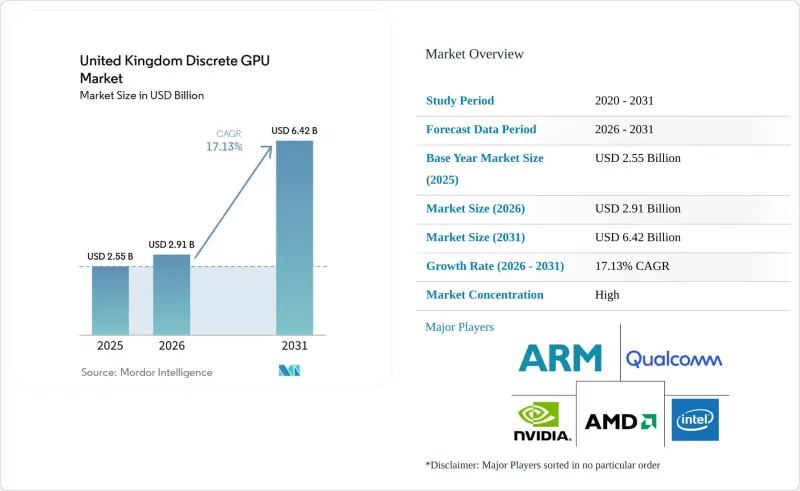

United Kingdom Discrete GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united kingdom discrete GPU market size is expected to grow from USD 2.55 billion in 2025 to USD 2.91 billion in 2026 and is forecast to reach USD 6.42 billion by 2031 at a 17.13% CAGR over 2026-2031.

This report is Segmented by Device Application (Mobile Devices and Tablets, Pcs and Workstations, Servers and Datacenter Accelerators, and More), Memory Type (GDDR-Based GPUs and HBM-Based GPUs), and Performance Tier (Low-Cost GPUs, Mainstream GPUs, High-Performance Consumer GPUs, and More). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Discrete GPU Market Trends and Insights

Explosive Growth in UK AI Start-Ups Demanding High-End GPUs

Venture funding peaked in 2025 as Nscale closed GBP 1.6 billion (USD 2.0 billion) to deploy GPU-dense clusters that serve foundation-model developers. Capital concentration in London and Cambridge triggers localized rack-space shortages, pushing datacenter utilization above the industry norm of 60%. Fractile AI's low-precision arithmetic reduces power draw by up to 90%, widening the addressable base for cost-sensitive training workloads. NVIDIA pledged to deliver more than 120,000 H200 and Blackwell Ultra units to UK customers by late 2026, locking in supply despite global shortages.

Government Supercomputing Investments

The GBP 2 billion Compute Roadmap scales national AI Research Resource twenty-fold by 2027, anchored by Isambard-AI and the Edinburgh International Data Facility. Isambard-AI has already delivered one million GPU hours to Nightingale AI's federated learning pilot across 14 NHS. Regulatory guidance from the AI Safety Institute requires transparent model risk assessments, rewarding hardware vendors that offer turnkey compliance tooling.

Supply Chain Exposure to Taiwan Foundries

UK customers source a significant portion of their advanced GPUs from Taiwan Semiconductor Manufacturing Company, a reliance that officials deem "very exposed" to geopolitical upheavals. Due to Brexit's rules of origin thresholds, partially assembled boards face hurdles to achieving duty-free status, resulting in customs delays and straining inventory buffers. Even with plans for diversification through EU fabs, relief isn't expected until 2028.

Other drivers and restraints analyzed in the detailed report include:

- Rising Cloud Gaming Adoption Across the UK

- Automotive OEMs Shift to Centralized ADAS Compute Platforms

- High Electricity Costs Limiting On-Prem GPU Farms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Servers and Datacenter Accelerators controlled 39.59% of the United Kingdom discrete GPU market in 2025, eclipsing all other categories as CoreWeave earmarked GBP 1 billion (USD 1.27 billion) for London facilities powered by H200 silicon. The United Kingdom's discrete GPU market for server-class boards is projected to grow at a 17.55% CAGR to 2031, driven by AI sovereignty mandates. PCs and Workstations, once the shipment leader, slipped to about 28% share as enterprises stream desktop environments from GPU-enabled virtual machines. Gaming Consoles and Handhelds contributed to the total revenue. Meanwhile, Automotive and ADAS devices secured a share, bolstered by Jaguar Land Rover's adoption of the DRIVE Orin silicon.

Datacenter build-outs funnel demand toward power-hungry, HBM-equipped cards, tilting the mix toward premium average selling prices. NHS diagnostic pilots, however, prefer mid-tier boards that balance watt draw with sufficient tensor throughput, signaling pockets of diversified adoption. As London rack space tightens, hyperscalers are positioning new clusters in Scotland and the North to exploit shorter wait times for grid connections, redistributing regional card allocations without denting national volume growth.

List of Companies Covered in this Report:

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Qualcomm Technologies Inc.

- Samsung Electronics Co. Ltd.

- ARM Ltd.

- Imagination Technologies Ltd.

- Graphcore Ltd.

- Apple Inc.

- MediaTek Inc.

- Alibaba Group Holding Ltd. (T-Head)

- Baidu Inc. (Kunlun)

- Huawei Technologies Co. Ltd. (HiSilicon)

- Tenstorrent Inc.

- ASUSTeK Computer Inc.

- Zotac Technology Ltd.

- Sapphire Technology Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive Growth in UK AI Start-Ups Demanding High-End GPUs

- 4.2.2 Government Supercomputing Investments (e.g., Frontier AI Taskforce)

- 4.2.3 Rising Cloud Gaming Adoption Across the UK

- 4.2.4 Automotive OEMs' Shift to Centralized ADAS Compute Platforms

- 4.2.5 Consumer Demand for 4K/8K and VR-Ready Gaming Experiences

- 4.2.6 Expansion of Edge AI Inference in NHS Diagnostics

- 4.3 Market Restraints

- 4.3.1 Supply Chain Exposure to Taiwan Foundries

- 4.3.2 High Electricity Costs Limiting On-Prem GPU Farms

- 4.3.3 Skills Shortage in Parallel-Programming Talent Pool

- 4.3.4 Import Tariff Uncertainty Post Brexit Trade Deals

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Application

- 5.1.1 Mobile Devices and Tablets

- 5.1.2 PCs and Workstations

- 5.1.3 Servers and Datacenter Accelerators

- 5.1.4 Gaming Consoles and Handhelds

- 5.1.5 Automotive / ADAS

- 5.1.6 Other Embedded and Edge Devices

- 5.2 By Memory Type

- 5.2.1 GDDR-Based GPUs

- 5.2.2 HBM-Based GPUs

- 5.3 By Performance Tier

- 5.3.1 Low-Cost GPUs (Less than USD 100)

- 5.3.2 Mainstream GPUs (USD 100-USD 400)

- 5.3.3 High-Performance Consumer GPUs (USD 400-USD 1,200)

- 5.3.4 Data Center / AI Accelerator GPUs (Greater than USD 1,200)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies Inc.

- 6.4.5 Samsung Electronics Co. Ltd.

- 6.4.6 ARM Ltd.

- 6.4.7 Imagination Technologies Ltd.

- 6.4.8 Graphcore Ltd.

- 6.4.9 Apple Inc.

- 6.4.10 MediaTek Inc.

- 6.4.11 Alibaba Group Holding Ltd. (T-Head)

- 6.4.12 Baidu Inc. (Kunlun)

- 6.4.13 Huawei Technologies Co. Ltd. (HiSilicon)

- 6.4.14 Tenstorrent Inc.

- 6.4.15 ASUSTeK Computer Inc.

- 6.4.16 Zotac Technology Ltd.

- 6.4.17 Sapphire Technology Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment