PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044019

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044019

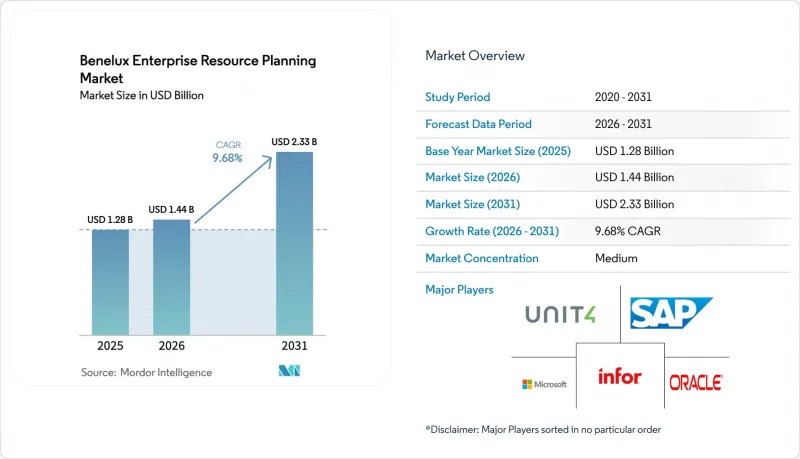

Benelux Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Benelux enterprise resource planning market size was valued at USD 1.28 billion in 2025 and is estimated to grow from USD 1.44 billion in 2026 to reach USD 2.33 billion by 2031, at a CAGR of 9.68% during the forecast period (2026-2031).

Demand is accelerating as e-invoicing mandates, EU recovery-fund grants, and embedded generative-AI copilots shorten replacement cycles and shift budgets toward cloud subscriptions. Belgium's Peppol e-invoicing mandate took effect on January 1, 2026, forcing thousands of suppliers to upgrade legacy accounting modules or risk losing public-sector contracts, while the Corporate Sustainability Reporting Directive (CSRD) is pushing enterprises to instrument ESG data flows directly within ERP backbones rather than relying on spreadsheet reconciliations.Mid-market manufacturers are adopting cloud suites to reduce total cost of ownership, while banks in Luxembourg prioritize cyber-resilient deployments that comply with the Digital Operational Resilience Act. Vendors are retiring on-premise support, widening the value gap between SaaS and perpetual licenses, and spurring two-tier architectures that link edge factories to central finance cores. Competitive intensity is highest in the Netherlands, where local champions Exact and Visma jostle with SAP and Microsoft, and lowest in Luxembourg, where regulatory complexity favors incumbents with deep financial-services templates.

Benelux Enterprise Resource Planning Market Trends and Insights

Cloud-Native Adoption Among Mid-Market Firms

SaaS total cost of ownership now undercuts perpetual licenses by roughly 20%, prompting firms with 100-999 full-time employees to replace decade-old systems rather than patch them. Faster patch cycles, predictable operating expense models, and easier integration with acquired subsidiaries have cut selection timetables from 18 months to 9 months. Vendors able to document payback in less than a year are winning against rivals still focused on bespoke customization. The market therefore tilts toward providers offering modular, API-first suites that enable rapid scale-up without infrastructure refreshes.

Growing Compliance Pressure on E-Invoicing and ESG Reporting

Belgium's Peppol framework obliges public-sector suppliers to transmit structured invoices, eliminating PDF workflows and forcing thousands of SMEs to modernize accounting modules. The Corporate Sustainability Reporting Directive adds a mandatory layer of emissions and labor-practice disclosure, making real-time data capture in finance and supply-chain ledgers a non-negotiable requirement. Early movers that embed sustainability metrics directly inside general-ledger structures reduce manual reconciliation by about 40% and lock in competitive advantage as audit deadlines near. The Benelux enterprise resource planning market is therefore expanding fastest where compliance risk is highest.

High Switching Costs from Legacy Custom Solutions

Localization investments in Belgian social security filings, Dutch payroll tax logic, and Luxembourg fund accounting rules often exceed USD 2 million per subsidiary. Enterprises face a dilemma between costly re-implementation and accepting functionality gaps that invite manual workarounds. Roughly half of ICT projects in the region report delays due to legacy complexity, so vendors offering automated code conversion and data migration tools accelerate deal velocity. Firms lacking such tooling lose momentum in the market because buyers now insist on capped migration risk.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Digitalization Incentives from EU Recovery Funds

- Rising Integration of AI Copilots Into ERP Suites

- Shortage of Skilled ERP Consultants in The Region

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-native suites accounted for 62.73% of 2025 revenue and will expand at a 10.48% CAGR, underpinned by vendor roadmaps that bundle finance, supply chain, and HCM into a single contract. The Benelux enterprise resource planning market for two-tier or edge ERP is currently smaller; however, it is experiencing rapid growth, as manufacturers increasingly deploy edge nodes on factory floors for latency-sensitive execution. Vendors re-platforming legacy code to multi-tenant architectures are racing to protect installed bases, while API-first challengers integrate easily with warehouse automation and e-commerce add-ons. Two-tier growth therefore enlarges, rather than cannibalizes, overall market share by unlocking new shop-floor and remote-site use cases.

Mobile-first ERP and social or collaborative suites add further momentum by extending workflows to frontline workers and project teams that operate outside the traditional back office. Field technicians in utilities and telecom companies now approve work orders and update inventory from smartphones, eliminating the lag that once plagued paper-based processes. Collaborative suites embed chat, document sharing, and workflow orchestration inside the ERP screen, shrinking email volume and reducing cycle time on proposal approvals, design reviews, and procurement exceptions. Because these user-experience upgrades raise daily engagement, they limit shelf-ware risk and improve renewal rates, which in turn supports the premium pricing that SaaS vendors command.

Finance and accounting modules delivered 53.47% of 2025 revenue, driven by real-time statutory reporting and cross-border VAT automation across three jurisdictions. Manufacturing execution applications add IoT sensor data and quality traceability, posting a 10.68% CAGR that outstrips every other function. Omnichannel retail strategies maintain a significant share for customer relationship and commerce, while human capital management is experiencing steady growth due to complex labor laws and the adoption of self-service workforce portals. Pre-integrated data models covering finance, supply chain, and HCM improve upsell velocity and expand the Benelux enterprise resource planning market for full-suite providers.

Supply-chain and operations modules are becoming the focal point of AI pilot projects that optimize safety-stock targets and reschedule transport in real time when ports experience congestion or strikes. Human capital teams are layering skills-taxonomy engines onto core HR data, building internal talent marketplaces that match open roles with employees trained on new production systems. Customer-facing teams, meanwhile, use unified product, inventory, and credit data to quote accurate delivery dates during live sales calls, reducing order cancellations.

The Benelux Enterprise Resource Planning Market Report is Segmented by Type (Cloud-Native Suite, Mobile-First ERP, and More), Business Function (Finance and Accounting, and More), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Industry Vertical (Manufacturing, BFSI, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- Infor Inc.

- Epicor Software Corporation

- The Sage Group plc

- TOTVS S.A.

- Odoo S.A.

- Deltek Inc.

- QAD Inc.

- Workday Inc.

- Unit4 N.V.

- Priority Software Ltd.

- SYSPRO (Pty) Ltd.

- IFS AB

- Acumatica Inc.

- Exact Holdings B.V.

- Visma A/S

- Ramco Systems Ltd.

- Cedesoft A.G.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-Native Adoption Among Mid-Market Firms

- 4.2.2 Growing Compliance Pressure (E-Invoicing and ESG Reporting)

- 4.2.3 Accelerated Digitalization Incentives from EU Recovery Funds

- 4.2.4 Rising Integration of AI Copilots Into ERP Suites

- 4.2.5 Vendor Push Toward Subscription Renewals and Upsell

- 4.2.6 Demographic Talent Crunch Driving Automation

- 4.3 Market Restraints

- 4.3.1 High Switching Costs From Legacy Custom Solutions

- 4.3.2 Shortage of Skilled ERP Consultants in the Region

- 4.3.3 Cyber-Sovereignty Concerns Over Public Cloud Hosting

- 4.3.4 Inflation-Driven IT Budget Caution Among SMEs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Cloud-Native Suite

- 5.1.2 Mobile-First ERP

- 5.1.3 Social / Collaborative ERP

- 5.1.4 Two-Tier / Edge ERP

- 5.2 By Business Function

- 5.2.1 Finance and Accounting

- 5.2.2 Supply-Chain and Operations

- 5.2.3 Human Capital Management

- 5.2.4 Customer Relationship and Commerce

- 5.2.5 Manufacturing Execution and Quality

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Retail and E-commerce

- 5.5.3 BFSI

- 5.5.4 Government and Public Sector

- 5.5.5 IT and Telecom

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Others Industry Vertical

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Infor Inc.

- 6.4.5 Epicor Software Corporation

- 6.4.6 The Sage Group plc

- 6.4.7 TOTVS S.A.

- 6.4.8 Odoo S.A.

- 6.4.9 Deltek Inc.

- 6.4.10 QAD Inc.

- 6.4.11 Workday Inc.

- 6.4.12 Unit4 N.V.

- 6.4.13 Priority Software Ltd.

- 6.4.14 SYSPRO (Pty) Ltd.

- 6.4.15 IFS AB

- 6.4.16 Acumatica Inc.

- 6.4.17 Exact Holdings B.V.

- 6.4.18 Visma A/S

- 6.4.19 Ramco Systems Ltd.

- 6.4.20 Cedesoft A.G.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment