PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044020

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044020

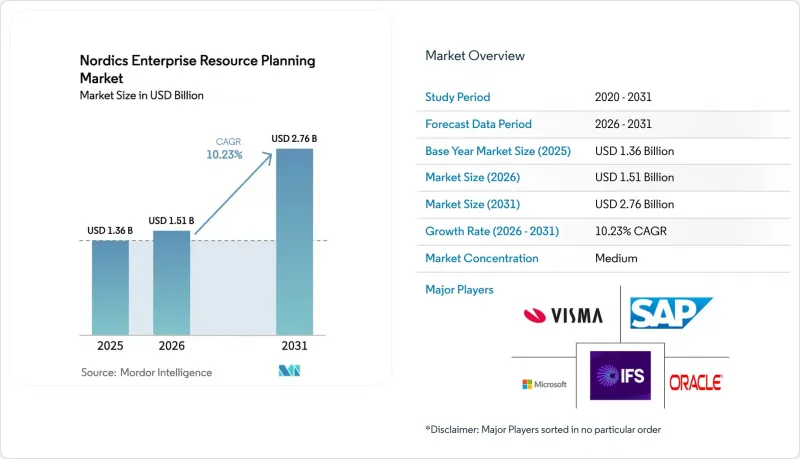

Nordics Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Nordic enterprise resource planning market size is projected to expand from USD 1.36 billion in 2025 and USD 1.51 billion in 2026 to USD 2.76 billion by 2031, registering a CAGR of 10.23% between 2026 to 2031.

Strong preference for cloud-native platforms, mandatory near-real-time value-added tax reporting, and sovereign-cloud rollouts are steering investment decisions. Vendors that deliver pre-certified tax engines, embedded sustainability analytics, and Nordic-specific payroll integrations are winning new logos even as older on-premise systems linger in public-sector and heavy-industry accounts. The Nordic enterprise resource planning market is also shaped by a deepening technology-talent shortage that pushes finance and operations leaders toward extensive process automation, while divergent interpretations of data residency under the Schrems II ruling keep procurement teams cautious about hyperscalers that cannot provide in-country key custody. Despite inflation-linked budget freezes across municipal buyers, private manufacturers and service firms continue to modernize to ensure uninterrupted regulatory compliance and the sharing of real-time data with suppliers, auditors, and lenders.

Nordics Enterprise Resource Planning Market Trends and Insights

Accelerated Cloud Migration Across Nordic SMEs

Small and medium enterprises redirected capital budgets during 2024-2025 toward subscription models that eliminate server maintenance and free up scarce IT personnel. Local champions such as Fortnox added real-time corporate-card feeds that write directly to ledgers, and Visma migrated 17 acquired payroll platforms onto a single multitenant stack. AI-first entrants like Done.ai embedded bookkeeping into banking apps, scaling to tens of thousands of users without standalone software rollouts. A March 2025 survey showed 91% of Nordic tax and finance leaders deem managed services vital for overcoming talent shortages, signaling sustained momentum for cloud conversions. Two-tier ERP pilots in Arctic supply chains further validate lightweight architectures that synchronize summary data to central systems during scheduled windows.

Government-Led Digital Transformation Initiatives

National digital-agency programs are underwriting multi-million-dollar replacements of fragmented municipal systems with interoperable suites. Examples include a nine-municipality contract in Kongsberg, Norway, and Stockholm City's adoption of cloud budgeting tools that integrate into an existing SAP ledger. Finland's Espoo expanded its integrator partnership to handle triple the ICT workload across its education and social service departments. Denmark's central procurement body elevated IT security above sustainability in bid evaluations, demonstrating heightened scrutiny of vendor lock-in and cross-border data flows. These public projects create reference architectures that private buyers emulate, compressing vendor shortlists and spurring the Nordic enterprise resource planning market toward common data models.

Legacy Custom-Built Systems with High Switching Costs

Many municipalities, universities, and conglomerates still rely on 1990s-era COBOL solutions welded to payroll and pension databases. Modernization entails multi-year parallel runs, costly data cleansing, and process re-engineering that can exceed annual maintenance fees by three times. Migrating these environments to commercial cloud platforms requires data cleansing, business-process reengineering, and parallel runs that can span 18 to 36 months and consume budgets three to five times the annual cost of maintaining the legacy system. Recent public-sector migrations illustrate 14-month timelines even for limited-scope deployments, encouraging organizations to extend support contracts rather than replace core ledgers. This inertia slows cloud growth among larger entities and segments the Nordic enterprise resource planning market between agile SME adopters and risk-averse incumbents.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for ESG-Linked Reporting Modules

- Near-Real-Time VAT Reporting Mandates

- Data-Residency Concerns Under Schrems II

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-native suites already account for 62.73% of the Nordic enterprise resource planning market in 2025, remain the cornerstone of modernization programs. Subscription pricing removes capital barriers for SMEs, while sovereign cloud regions address public-sector data-sovereignty concerns. Mobile-first offerings, which held a significant share, attract construction and logistics crews that work offline and sync later. Two-tier and edge deployments stand out in terms of growth, with an 11.03% CAGR, driven by rapid expansion as multinational manufacturers establish lightweight instances for Arctic subsidiaries.

Quarterly product releases illustrate rapid innovation. IFS Cloud 25R2 embedded generative planning, Oracle NetSuite Next unveiled conversational agents, and SIX ERP entered the scene with an AI-first platform promising EU-resident data by default. Pilot studies at Lulea University verify that edge nodes can operate over intermittent satellite links, lending credence to distributed architectures. Overall, deployment flexibility coupled with modular AI tools is reshaping vendor shortlists across the Nordic enterprise resource planning market.

Finance and accounting modules accounted for 53.47% of the Nordic enterprise resource planning market share in 2025, driven by statutory changes requiring invoice-level tax data and granular ESG cost allocation. Supply-chain suites follow as manufacturers connect warehousing, planning, and logistics to a single data fabric, with growth of 11.23% through 2031 underscoring an enduring priority. Meanwhile, manufacturing execution systems, although accounting for a smaller share of future revenues, are expected to grow at the fastest rate as Swedish and Norwegian factories integrate real-time shop-floor feeds to comply with CSRD traceability clauses.

AI-native add-ons such as MAKIRA's invoice-automation engine and Semine's payables bot deliver targeted productivity gains, slashing approval cycles and freeing accountants for advisory tasks. Healthcare providers, exemplified by Terveystalo, bridge electronic health records with payroll and procurement systems to comply with reimbursement rules. This convergence of clinical, operational, and financial data broadens the addressable scope for the Nordic enterprise resource planning industry while deepening integration complexity that favors vendors with robust platform ecosystems.

The Nordics Enterprise Resource Planning Market Report is Segmented by Type (Cloud-Native Suite, Mobile-First ERP, and More), Business Function (Finance and Accounting, and More), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Manufacturing, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- SAP SE

- Microsoft Corporation

- Oracle Corporation

- Unit4 N.V.

- IFS AB

- Infor Inc.

- Sag Group Plc

- Workday Inc.

- Visma AS

- Fortnox AB

- Jeeves Information Systems AB

- RamBase AS

- Epicor Software Corporation

- QAD Inc.

- Deltek Inc.

- Priority Software Ltd.

- Acumatica Inc.

- Odoo SA

- Katana Technologies OU

- Monitor ERP Systems AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Cloud Migration Across Nordic SMEs

- 4.2.2 Government-led Digital Transformation Initiatives

- 4.2.3 Tight Integration with Nordic Open-Banking APIs

- 4.2.4 Rising Demand for ESG-Linked Reporting Modules

- 4.2.5 Near-Real-Time VAT Reporting Mandates

- 4.2.6 Growing Shortage of Skilled Finance Talent Driving Automation

- 4.3 Market Restraints

- 4.3.1 Legacy Custom-Built Systems with High Switching Costs

- 4.3.2 Data-Residency Concerns Under Schrems

- 4.3.3 Limited 5G Coverage in Remote Nordic Regions

- 4.3.4 Inflation-Driven IT Budget Freezes in Public Sector

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Cloud-Native Suite

- 5.1.2 Mobile-First ERP

- 5.1.3 Social / Collaborative ERP

- 5.1.4 Two-Tier / Edge ERP

- 5.2 By Business Function

- 5.2.1 Finance and Accounting

- 5.2.2 Supply-Chain and Operations

- 5.2.3 Human Capital Management

- 5.2.4 Customer Relationship and Commerce

- 5.2.5 Manufacturing Execution and Quality

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Retail and E-commerce

- 5.5.3 BFSI

- 5.5.4 Government and Public Sector

- 5.5.5 IT and Telecom

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Other Industry Verticals

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Microsoft Corporation

- 6.4.3 Oracle Corporation

- 6.4.4 Unit4 N.V.

- 6.4.5 IFS AB

- 6.4.6 Infor Inc.

- 6.4.7 Sag Group Plc

- 6.4.8 Workday Inc.

- 6.4.9 Visma AS

- 6.4.10 Fortnox AB

- 6.4.11 Jeeves Information Systems AB

- 6.4.12 RamBase AS

- 6.4.13 Epicor Software Corporation

- 6.4.14 QAD Inc.

- 6.4.15 Deltek Inc.

- 6.4.16 Priority Software Ltd.

- 6.4.17 Acumatica Inc.

- 6.4.18 Odoo SA

- 6.4.19 Katana Technologies OU

- 6.4.20 Monitor ERP Systems AB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment