PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044091

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044091

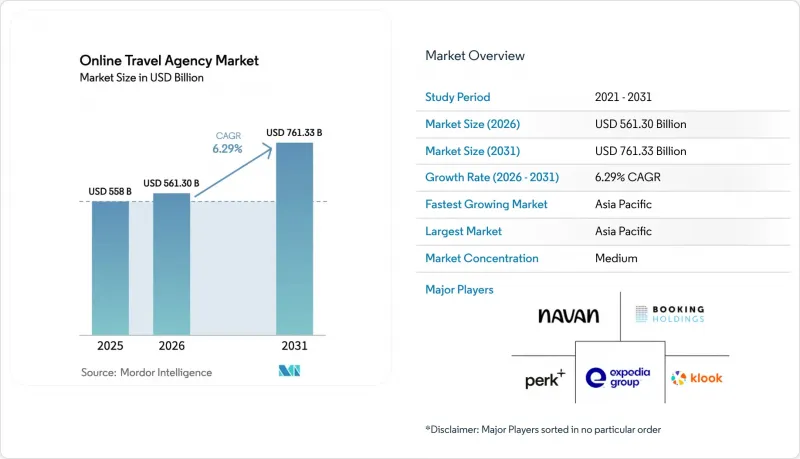

Online Travel Agency - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The online travel agency market size is USD 561.30 billion in 2026 and is projected to reach USD 761.33 billion by 2031 at a 6.29% CAGR.

Travelers increasingly use digital channels for trip discovery, booking, and management, with mobile-first designs surpassing desktop interfaces. Mobile platforms gained significant transactional traffic by 2025, driven by biometric logins, offline itinerary access, and real-time alerts. Asia-Pacific led app-centric bookings, supported by superapp ecosystems integrating travel with payments, ride-hailing, and food delivery. Transportation dominates volumes, while accommodation grows rapidly due to alternative stays boosting inventory and margins. These trends shape strategies in the online travel agency market, aligning with ongoing upgrades in app infrastructure and embedded payment solutions.

Global Online Travel Agency Market Trends and Insights

Mobile-first booking and app adoption

App-native booking functions are reshaping product roadmaps and cost structures in the online travel agency market. Airbnb reported that 64% of its Q4 2025 bookings were made via mobile apps, with mobile volumes growing double digits year-over-year as web traffic lagged. Trip.com Group stated that over 70% of its transactions originate on mobile devices, with higher conversion rates due to biometric checkout and real-time push alerts. Platforms now focus on real-time inventory accuracy, latency control, and dynamic repricing to capture intent quickly. In Southeast Asia, platforms such as Klook prioritize app experiences before extending features to web interfaces. Incumbents face a multi-year shift toward app-centric architectures to enhance booking and servicing operations.

International travel recovery and Asia-Pacific-led growth

Asia-Pacific international arrivals reached 331 million in 2025, recovering to 92.6% of 2019 levels by January 2026. Outbound travel from China grew in 2025, while inbound and intra-Asia travel strengthened in Japan, South Korea, and Southeast Asia. India saw a sharp rise in booked nights on major platforms, highlighting the need for localized payments, loyalty, and content strategies. Trip.com Group reported strong international booking growth in Q3 2025, driven by inventory depth and regional supply-sharing relationships. Visa's efforts in cross-border payment acceptance and localized checkout experiences underscore the importance of settlement infrastructure and risk control as key differentiators in the region's online travel agency market expansion.

Dependence on Google/AI search raises CAC volatility

AI-generated travel summaries on large search platforms are reducing clicks to OTA sites, creating budget uncertainties in performance channels for the online travel agency market. This impacts both cost per click and predictability, as model updates and UI changes occur more frequently than quarterly. Larger players are reallocating budgets from auction-based intent capture to brand-led awareness, boosting direct traffic. Smaller and mid-sized OTAs face challenges due to weaker brand search volumes and limited ability to outbid larger competitors. This dynamic creates a divide, with global platforms and niche providers maintaining steadier traffic funnels, while mid-market generalists experience increased pressure.

Other drivers and restraints analyzed in the detailed report include:

- Embedded fintech and BNPL lift conversion and AOV

- AI-powered personalization and dynamic pricing optimization

- Regulatory scrutiny and rate-parity bans (European Union DMA)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation bookings accounted for 43.8% of the online travel agency market share in 2025. Accommodation bookings are projected to grow at a 6.4% CAGR through 2031, driven by expanded alternative stays and improved cross-selling into packages. Supplier-side investments reflect this shift, with alternative accommodations scaling inventory and attracting longer-stay demand with better unit economics. Booking Holdings added 8.6 million alternative accommodation listings in 2025, an 8% year-over-year increase that supported higher-margin categories. Airlines' New Distribution Capability adoption fragmented content across proprietary APIs, while look-to-book ratios above 1,000:1 in 2025 strained infrastructure and servicing costs for flight-only transactions. Platforms focusing on accommodations and experiences benefit from richer content, stronger margins, and improved loyalty engagement.

Flights remain critical for cross-selling. Booking.com processed 68 million flight bookings in 2025, a 37% year-over-year increase, though flights still represent a small portion of its room-night base, highlighting growth potential with better air content. Tours and activities are consolidating into branded marketplaces. Klook listed over 100,000 bookable experiences across 300+ destinations, capitalizing on experiential demand in leisure trips. IATA's NDC framework advances content modernization, but servicing remains complex due to heterogeneity among 300+ airlines. Vertically integrated platforms combining supply, distribution, and payments mitigate these challenges, aligning with the market's medium-term value concentration.

The Global Online Travel Agency Market Report is Segmented by Service Type (Accommodation, Transportation, Vacation Packages, Others), Device (Desktop, Mobile), Traveler Type (Leisure Travelers, Business Travelers), and Geography (North America, South America, Asia-Pacific, Europe, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 38.3% of the online travel agency market share in 2025 and is projected to grow at 6.8% through 2031, driven by mobile-first consumer behavior and superapp ecosystems integrating travel, payments, and mobility. International arrivals in the region reached 331 million in 2025, recovering to 92.6% of 2019 levels by January 2026. Payment localization and language support are critical in markets like India, Indonesia, and Vietnam, where app-native consumers demand flexible options and quick confirmations. Trip.com Group reported strong international booking growth through Q3 2025, supported by regional inventory partnerships and localized operations. Visa's cross-border acceptance tools highlight the importance of aligning checkouts with local preferences to improve conversions.

North America and Europe accounted for a significant share of the global online travel agency market in 2025, with growth varying by corridor and policy environment. The United States experienced a 14% drop in international arrivals in March 2025 and a growing travel trade deficit, influencing marketing strategies for inbound tourism. Europe recorded 793 million international tourists in 2025, with high online booking penetration requiring differentiation beyond pricing. The DMA's regulations on Booking.com add compliance challenges, potentially altering commission structures, data sharing, and parity clause enforcement in European Union markets. These changes emphasize the need for brand loyalty to reduce reliance on paid media.

The Middle East, Africa, and South America offer growth opportunities but require tailored strategies. Visa liberalization and destination investments in Gulf states drive demand, though online penetration remains below global averages, necessitating efforts in payment and language support. Currency volatility and inflation in South America increase the need for dynamic pricing, multi-currency transactions, and strong refund policies to maintain consumer confidence. Regional players integrate travel services into broader ecosystems like e-commerce, fostering trust and familiarity among new users. These strategies focus on value chain control and local credibility for sustainable growth.

- Booking Holdings (Booking.com, Priceline, Agoda)

- Navan (Reed & Mackay, Comtravo, Resia, Atlanta Events & Corporate Travel Consultants)

- Perk (Formerly TravelPerk)

- Expedia Group (Expedia, Hotels.com, Vrbo)

- Klook

- GetYourGuide

- Trip.com Group

- eDreams ODIGEO (eDreams, Opodo, GoVoyages)

- AsiaYo

- Secret Escapes

- TUI Musement

- Yatra

- MakeMyTrip

- Omio

- Prosus

- Traveloka

- lastminute.com

- On the Beach

- Hostelworld

- Universal Travels & Tourism LLC

- Hopper

- Webjet

- Rome2Rio

- Headout

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mobile-first booking and app adoption

- 4.2.2 International travel recovery and Asia-Pacific-led growth

- 4.2.3 Embedded fintech and BNPL lift conversion and AOV

- 4.2.4 Airline NDC enables richer air retailing and ancillaries

- 4.2.5 Superapp and mini-program integrations expand OTA reach

- 4.2.6 AI-powered personalization and dynamic pricing optimization

- 4.3 Market Restraints

- 4.3.1 Dependence on Google/AI search raises CAC volatility

- 4.3.2 Regulatory scrutiny and rate-parity bans (European Union DMA)

- 4.3.3 NDC-driven content fragmentation and servicing complexity

- 4.3.4 Rising fraud/chargebacks in cross-border payments

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value - Gross Bookings/GMV)

- 5.1 By Service Type

- 5.1.1 Accommodation (Hotels, Alternative Accommodations)

- 5.1.2 Transportation

- 5.1.3 Vacation Packages

- 5.1.4 Others

- 5.2 By Device

- 5.2.1 Desktop

- 5.2.2 Mobile

- 5.3 By Traveler Type

- 5.3.1 Leisure Travelers

- 5.3.2 Business Travelers

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 Europe

- 5.4.4.1 United Kingdom

- 5.4.4.2 Germany

- 5.4.4.3 France

- 5.4.4.4 Spain

- 5.4.4.5 Italy

- 5.4.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.4.8 Rest of Europe

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Booking Holdings (Booking.com, Priceline, Agoda)

- 6.4.2 Navan (Reed & Mackay, Comtravo, Resia, Atlanta Events & Corporate Travel Consultants)

- 6.4.3 Perk (Formerly TravelPerk)

- 6.4.4 Expedia Group (Expedia, Hotels.com, Vrbo)

- 6.4.5 Klook

- 6.4.6 GetYourGuide

- 6.4.7 Trip.com Group

- 6.4.8 eDreams ODIGEO (eDreams, Opodo, GoVoyages)

- 6.4.9 AsiaYo

- 6.4.10 Secret Escapes

- 6.4.11 TUI Musement

- 6.4.12 Yatra

- 6.4.13 MakeMyTrip

- 6.4.14 Omio

- 6.4.15 Prosus

- 6.4.16 Traveloka

- 6.4.17 lastminute.com

- 6.4.18 On the Beach

- 6.4.19 Hostelworld

- 6.4.20 Universal Travels & Tourism LLC

- 6.4.21 Hopper

- 6.4.22 Webjet

- 6.4.23 Rome2Rio

- 6.4.24 Headout

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment