PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061620

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061620

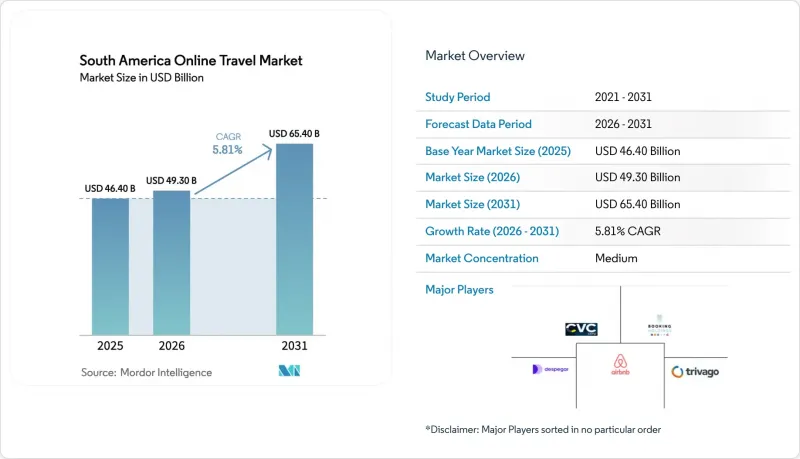

South America Online Travel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the south america online travel market size is USD 46.4 billion in 2025, expected to reach USD 49.30 billion in 2026 and USD 65.40 billion in 2031, reflecting a 5.81% CAGR.

This report is Segmented by Service Type (Transportation, Accommodation, Vacation Packages, Others), Device Type (Desktop, Mobile), Platform Type (Direct Booking Via Supplier-Direct Digital Channels, Online Travel Agencies), and Geography (Brazil, Argentina, Chile, Colombia, Peru, Others). The Market Forecasts are Provided in Terms of Value (USD).

South America Online Travel Market Trends and Insights

Mobile-First Access And App-Based Booking Adoption Surge Conversion

Airbnb's Q4 2025 financial results show how mobile-first access and app-centric innovations are driving higher conversion and booking growth globally, a trend that is highly relevant to the South America online travel market. In the quarter, nights and seats booked grew about 10% year-over-year, while gross booking value increased 16%, reflecting strong consumer engagement with the platform's digital channels. A key factor was the continued shift to mobile: app-based bookings rose roughly 20% year-over-year and accounted for 64% of total nights booked, up from 60% previously, indicating that more travelers are completing reservations through mobile apps rather than desktop or web interfaces. . This mobile dominance is supported by product enhancements such as improved search, flexible features like "Reserve Now, Pay Later," updated cancellation policies, and deeper AI integration within the app, all of which reduce friction and make mobile checkout more appealing. Growth in expansion markets including particularly strong performance in Brazil and acceleration in first-time bookers further suggest that a mobile-first strategy is widening the customer base, especially in regions with rising smartphone penetration. These trends underscore that seamless app experiences, localized features, and flexible payment options are key drivers of conversion in the digital travel landscape.

Instant And Alternative Payments Lift Conversion And Lower Merchant Costs

Instant payments now underpin the South America online travel market with lower-cost authorization and faster settlement than traditional card flows. In Latin America, fast-payment systems are accelerating digital adoption across consumer and merchant segments, a shift that reduces friction and expands inclusion for underbanked groups that rely on wallets instead of cards. Real-time rails enable immediate fund capture and support instant refunds during disruptions, improving trust and conversion for larger transactions. Cross-border expansion is underway as PagBrasil enables PIX payments for tourists and merchants with roaming and direct integrations for Argentine banks and wallets to scan QR codes and settle in local currency while merchants receive funds instantly. Wallet ecosystems in Brazil and across the region tie together stored balances, local acceptance, and installment options that align to travel use cases. As initiation services scale under open-finance frameworks, larger OTAs may partner with licensed providers rather than build from scratch, given compliance and security requirements that favor scale.

Elevated Fraud And Chargeback Costs Compress Margins And Limit Scale

Travel merchants face the highest global average chargeback value among consumer sectors, and total costs per dispute can be several times the original transaction once fees and operational overhead are included. Industry groups also document rising attack volumes and describe friendly fraud as a dominant vector, which is particularly painful for high-ticket categories like flights and multi-day packages. Conversion suffers when authentication adds friction, yet the long-run payoff from tokenization, biometrics, and real-time alerts is lower dispute exposure and fewer write-offs. Larger OTAs deploy behavioral scoring and identity orchestration at scale, while smaller firms rely on third-party tools and must absorb higher unit costs for fraud management. The net effect is a direct drag on growth for the South America online travel market as resources shift from marketing and product to fraud containment.

Other drivers and restraints analyzed in the detailed report include:

- OTA Penetration And Super-App Ecosystems Expand Addressable Market

- Airline Capacity Recovery And NDC Enable Richer Retailing

- FX Volatility Erodes Predictability And Distorts Regional Demand Flows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation accounted for 42.1% of bookings in 2025 and remains the largest segment across the South America online travel market, while accommodation is the fastest riser with a 5.93% CAGR projected through 2031 for the South America online travel market size. Airline capacity and punctuality metrics improved across the region in 2025, which supported reliable schedules and increased consumer confidence in booking flights through OTAs and supplier apps. Airlines with strong financials expanded premium offerings and delivered margin gains, while carriers exiting restructuring restored capacity and rebalanced networks that had previously constrained some origin and destination pairs. Bus-ticketing digitization added meaningful incremental supply, with new marketplace entrants using lower commissions, PIX acceptance, and app-based discovery to increase reach among value-focused travelers. Accommodation growth is accelerating as vacation rentals scale and boutique properties leverage OTAs for discovery, with Airbnb's 2025 results signaling strong regional demand and a healthy host pipeline.

The economics of transportation in the South America online travel market reflect divergent airline balance sheets and content strategies, with NDC adoption enabling richer bundles that can improve conversion and ancillary attach rates for integrated distributors. OTAs deepen their mix of vacation packages to improve margins, while supplier-direct channels push loyalty to strengthen share of wallet. Bus aggregators invest in AI to personalize itineraries and drive conversion at lower basket sizes, extending digital travel's reach into secondary corridors. Accommodation players promote flexible payments, including installments and instant pay, which aligns with wallet adoption and shortens checkout on mobile. Over the forecast, accommodation narrows the gap with transportation as more rentals, boutique inventory, and packaged experiences improve choice and value for travelers across the South America online travel market.

List of Companies Covered in this Report:

- Despegar.com Corp (includes Decolar brand)

- Booking Holdings Inc. (Booking.com)

- Airbnb, Inc.

- CVC Corp

- Trivago N.V.

- Hurb (Hotel Urbano)

- Expedia Group, Inc.

- KAYAK

- Trip.com Group (Trip.com, Skyscanner)

- ClickBus

- Rappi Travel

- Rentcars.com

- Almundo

- Buser

- MakeMyTrip Ltd.

- Agoda

- Tripadvisor

- Lastminute.com

- Kiwi.com

- eDreams ODIGEO

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mobile-first access and app-based booking adoption

- 4.2.2 Instant and alternative payments (Pix, wallets) lift conversion

- 4.2.3 OTA penetration and super-app travel ecosystems scale reach

- 4.2.4 Airline capacity recovery and NDC-driven retailing

- 4.2.5 Bus-ticketing digitization across markets

- 4.2.6 Open banking and instant-refund rails reduce friction

- 4.3 Market Restraints

- 4.3.1 Elevated fraud/chargebacks and dispute win-rate gaps

- 4.3.2 FX volatility and policy/tax headwinds on cross-border

- 4.3.3 Parity/MFN enforcement shifts and regulatory scrutiny

- 4.3.4 Route/slot constraints and consolidation risk in air

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Supplier Power

- 4.7.2 Buyer Power

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Trends & Innovations Influencing the Market

- 4.9 COVID-19 and Geo-Political Impact Assessment

5 Market Size & Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Transporation

- 5.1.2 Accommodation

- 5.1.3 Vacation Packages

- 5.1.4 Others

- 5.2 By Device Type

- 5.2.1 Desktop

- 5.2.2 Mobile

- 5.3 By Platform Type

- 5.3.1 Direct Booking (Supplier-direct digital channels)

- 5.3.2 Online Travel Agencies (OTAs)

- 5.4 By Country

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Chile

- 5.4.4 Colombia

- 5.4.5 Peru

- 5.4.6 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Despegar.com Corp (includes Decolar brand)

- 6.4.2 Booking Holdings Inc. (Booking.com)

- 6.4.3 Airbnb, Inc.

- 6.4.4 CVC Corp

- 6.4.5 Trivago N.V.

- 6.4.6 Hurb (Hotel Urbano)

- 6.4.7 Expedia Group, Inc.

- 6.4.8 KAYAK

- 6.4.9 Trip.com Group (Trip.com, Skyscanner)

- 6.4.10 ClickBus

- 6.4.11 Rappi Travel

- 6.4.12 Rentcars.com

- 6.4.13 Almundo

- 6.4.14 Buser

- 6.4.15 MakeMyTrip Ltd.

- 6.4.16 Agoda

- 6.4.17 Tripadvisor

- 6.4.18 Lastminute.com

- 6.4.19 Kiwi.com

- 6.4.20 eDreams ODIGEO

7 Market Opportunities & Future Outlook

- 7.1 Rapid Digital Adoption & Expanding Market Growth

- 7.2 Diversification of Travel Products & Enhanced Digital Services