PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044242

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044242

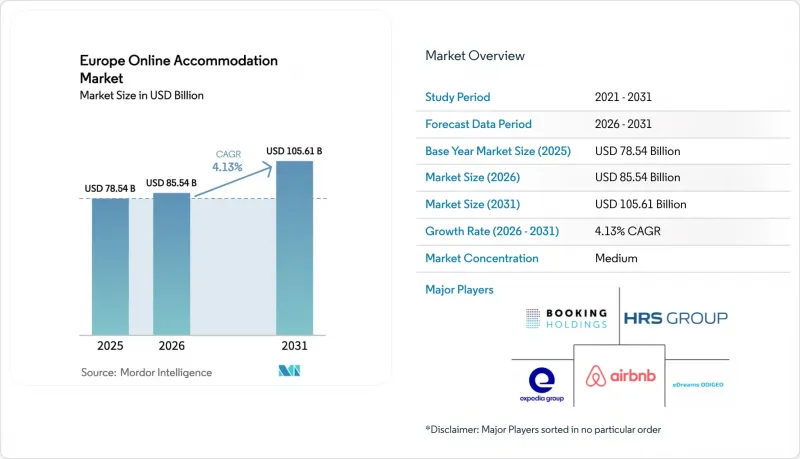

Europe Online Accommodation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe online accommodation market size is expected to grow from USD 78.54 billion in 2025 to USD 85.54 billion in 2026 and is forecast to reach USD 105.61 billion by 2031, reflecting a 4.13% CAGR through the forecast period.

As travel demand normalizes across the region, growth is increasingly driven by sustained digital adoption, high smartphone penetration, and strong cross-border mobility within Europe. The widespread use of mobile booking apps, price comparison tools, and digital payment systems continues to strengthen online channels, while the expansion of short-term rentals, serviced apartments, and hybrid lodging formats broadens the available inventory and attracts diverse traveler segments, including digital nomads and experience-focused tourists. Regulatory developments are also reshaping competitive dynamics within the market. Additionally, the Payment Services Regulation and PSD3, finalized in November 2025, introduce stronger authentication measures, IBAN and name verification requirements, and clearer liability frameworks to reduce fraud and harmonize cross-border digital payments. At the same time, platforms and hotel chains are increasingly integrating artificial intelligence into search algorithms, dynamic pricing, merchandising, and customer service operations, improving conversion rates and operational efficiency.

Europe Online Accommodation Market Trends and Insights

Surge in Smartphone-Led Mobile Bookings

Mobile devices captured 54.7% of booking volume in 2025 and led growth with platforms reporting higher in-app engagement, as evidenced by Airbnb's disclosure that 64% of Q4 2025 nights were booked via its app, up 400 basis points year over year. As of September 2025, Booking.com had 32 million listings, including 4.4 million active properties and 3.9 million alternative stays. The platform facilitated about 1.2 billion room nights over the year, with direct bookings around 65% of total nights. Alternative accommodations grew from 35% to 36%, highlighting rising demand for non-traditional stays and strong digital engagement in online accommodation. Data, privacy, and transparency baselines required by EU digital laws have prompted cleaner onboarding and consent flows that in turn support smoother mobile conversion journeys in the Europe online accommodation market. Product innovation in mobile checkout, including "Reserve Now, Pay Later," which Airbnb piloted in August 2025 and completed global rollout in February 2026, reinforces mobile's primacy by addressing liquidity constraints without disrupting host payouts.

Pent-Up Leisure Demand and Intra-Europe Travel Rebound

In 2025, the total number of nights spent in tourist accommodation establishments across the European Union reached a record high of approximately 3.08 billion, an increase of 61.5 million nights (+2%) compared with 2024. This growth reflects continued expansion in tourism activity across most EU Member States. European Travel Commission tracking showed that 77% of Europeans planned trips in the second half of 2025 despite economic headwinds, with a rising share seeking less crowded destinations, which expanded addressable demand across secondary and Central and Eastern European locations. Intra-regional travel remained a mainstay due to Schengen mobility and rail expansions, which together reduce friction and encourage shorter, more frequent trips that favor digital channels for accommodation search and booking. Southern and Mediterranean destinations absorbed a large share of peak-season activity in 2025 even as travelers diversified into Central and Eastern Europe, a pattern that sustains broad distribution of demand across the Europe online accommodation market. Aviation and maritime decarbonization policies entering into force in 2025 are raising operator compliance costs, which can redirect some demand to rail-accessible destinations and keep intra-Europe trips at the core of segment growth.

High OTA Commission Pressure on Supplier Margins

Commission structures in the OTA channel continue to weigh on supplier margins, and the merchant model's prominence has historically supported take rates that are difficult for smaller properties to offset via direct channels without scale in digital marketing or loyalty. As DMA enforcement curbs self-preferencing and parity provisions, some rate dispersion is emerging, but rebalancing remains gradual and uneven across markets in the Europe online accommodation market. Expedia's 2025 filings highlighted a notable divergence between its B2B business, which grew 24% year over year in Q4 2025, and B2C, which grew 5%, indicating a shift toward white-label partnerships that can alter distribution economics for suppliers and intermediaries. Tax and compliance headwinds also persist, as evidenced by Expedia's finalized USD 183 million settlement with Italian authorities for withholding tax obligations covering 2017-2023, which has implications for commission pass-through and visibility terms in several EU jurisdictions. Over the medium term, suppliers that scale AI-enabled revenue management and loyalty activation are better positioned to dilute commission exposure without sacrificing demand coverage within the Europe online accommodation market.

Other drivers and restraints analyzed in the detailed report include:

- EU Digital Markets Act: Unlocking Data-Driven Direct-Booking Innovation

- AI-Powered Dynamic Packaging and Personalized Offers Lift Conversion

- City-Level Clamp-Downs on Short-Term Rentals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hotels held 58.40% of the Europe online accommodation market in 2025, supported by ongoing additions from global chains and steady growth in loyalty programs that enhance both direct and indirect distribution across the region. Short-term and vacation rentals remain the fastest-growing accommodation type with a 6.81% CAGR projected through 2031, which reflects continued traveler appetite for residential space, flexible layouts, and neighborhood locations that complement traditional hotel use cases in the Europe online accommodation market. Regulatory changes are playing a crucial role, with new standardized registration requirements simplifying compliance for platforms and professional operators across EU member states. Leading platforms report a deep inventory of alternative accommodations, which adds variety and complements hotel options for mixed travel itineraries. Hotel chains are increasingly focusing on upscale and luxury segments to maintain their market share even as alternative accommodations continue to expand.

The growth of short-term rentals is balanced by increased compliance demands and operational complexity, encouraging greater professionalization and technology adoption among property managers and hosts. There is a noticeable shift toward leveraging AI-enhanced direct booking websites and revenue management tools, signaling a move from purely occupancy-driven growth to value creation through better operations and merchandising. Hotel brands are also gaining momentum, particularly in the luxury and lifestyle sectors, aligning with the preferences of premium travelers in major European cities. The dynamic between hotels and alternative stays remains positive, with each serving distinct customer needs while overlapping in areas like extended stays, family travel, and work-friendly accommodations. Overall, hotel loyalty programs, branded service quality, and mobile app conversions continue to sustain hotel market share even as alternative accommodations broaden consumer choice.

Online Travel Agencies held a 62.10% share in 2025 and are expected to post a 7.34% CAGR through 2031, as evolving regulations and the rise of direct distribution reshape booking patterns. The removal of parity clauses and increased transparency requirements under new regulations have allowed hotels and professional hosts greater flexibility to offer differentiated packages, loyalty rewards, and exclusive rates on their own platforms. OTAs are also adapting by expanding business-to-business partnerships and corporate travel solutions, complementing their consumer-facing channels. Mobile apps continue to be a key driver of bookings, with many travelers preferring the convenience and personalized experiences they provide. Moving forward, distribution strategies are expected to rely increasingly on AI-driven visibility and integrated travel solutions rather than traditional search rankings alone.

Direct booking channels are improving both customer experience and cost efficiency, supported by AI-powered revenue management tools that enhance pricing strategies and save operational time. New payment regulations introduce additional verification steps, which can complicate some intermediary processes but allow direct sites to offer smoother authentication and preferred payment options. Corporate and managed travel segments are becoming important sources of inventory as platforms strengthen business partnerships that extend reach beyond public search visibility. Metasearch engines are evolving to use AI personalization to improve the quality of traffic and bidding efficiency for both suppliers and OTAs. Overall, the market is moving toward a more balanced distribution environment where OTAs continue to play a critical role in reach and merchandising, while direct channels and corporate partnerships focus on improving margins and building customer loyalty.

The Europe Online Accommodation Market is Segmented by Accommodation Type (Hotels, Short-Term & Vacation Rentals, and More), Booking Channel (Online Travel Agencies (OTAs), Direct Supplier Websites & Apps, and More), Device Type (Mobile, Desktop/Laptop, and More), Traveler Type (Leisure, Business, and More), and Country (United Kingdom, Germany, France, and More). The Market Forecasts are Provided in Value (USD).

List of Companies Covered in this Report:

- Booking Holdings (Booking.com, Agoda)

- Expedia Group (Expedia, Hotels.com, Vrbo)

- Airbnb Inc.

- HRS Group

- eDreams ODIGEO (Opodo, GoVoyages)

- Trip.com Group (Ctrip)

- Trivago NV

- Hostelworld Group

- Lastminute.com Group

- TUI Group

- TripAdvisor (FlipKey, HouseTrip)

- Accor SA

- Marriott International

- Hilton Worldwide

- InterContinental Hotels Group (IHG)

- Radisson Hotel Group

- Melia Hotels International

- NH Hotel Group

- citizenM Hotels

- Whitbread PLC (Premier Inn)

- Travelodge UK

- Sykes Holiday Cottages

- Pierre & Vacances Center Parcs

- ALTIDO

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in smartphone-led mobile bookings

- 4.2.2 Pent-up leisure demand and intra-Europe travel rebound

- 4.2.3 OTA dominance creating transparent, price-competitive inventory

- 4.2.4 EU Digital Markets Act unlocking data-driven direct-booking innovation

- 4.2.5 AI-powered dynamic packaging & personalised offers lift conversion

- 4.2.6 Secondary-city tourism boom expands STR supply

- 4.3 Market Restraints

- 4.3.1 High OTA commission pressure on supplier margins

- 4.3.2 City-level clamp-downs on short-term rentals

- 4.3.3 Multi-scheme payments & PSD-3 compliance complexity

- 4.3.4 Revenue-tech talent shortages slow digital roll-outs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, 2020-2030)

- 5.1 Segmentation by Accommodation Type

- 5.1.1 Hotels

- 5.1.2 Short-term & Vacation Rentals

- 5.1.3 Hostels & Budget Stays

- 5.1.4 Campgrounds & Holiday Parks

- 5.1.5 Other Accommodation Types

- 5.2 Segmentation by Booking Channel

- 5.2.1 Online Travel Agencies (OTAs)

- 5.2.2 Direct Supplier Websites & Apps

- 5.2.3 Metasearch & Aggregators

- 5.2.4 Sharing-Economy Platforms

- 5.2.5 Corporate Travel Platforms

- 5.3 Segmentation by Device Type

- 5.3.1 Mobile

- 5.3.2 Desktop / Laptop

- 5.3.3 Tablet & Others

- 5.4 Segmentation by Traveler Type

- 5.4.1 Leisure

- 5.4.2 Business

- 5.4.3 Bleisure

- 5.4.4 Group & MICE

- 5.5 Segmentation by Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Spain

- 5.5.5 Italy

- 5.5.6 Netherlands

- 5.5.7 Nordics

- 5.5.8 Central & Eastern Europe

- 5.5.9 Benelux

- 5.5.10 Austria & Switzerland

- 5.5.11 Portugal

- 5.5.12 Greece

- 5.5.13 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Booking Holdings (Booking.com, Agoda)

- 6.4.2 Expedia Group (Expedia, Hotels.com, Vrbo)

- 6.4.3 Airbnb Inc.

- 6.4.4 HRS Group

- 6.4.5 eDreams ODIGEO (Opodo, GoVoyages)

- 6.4.6 Trip.com Group (Ctrip)

- 6.4.7 Trivago NV

- 6.4.8 Hostelworld Group

- 6.4.9 Lastminute.com Group

- 6.4.10 TUI Group

- 6.4.11 TripAdvisor (FlipKey, HouseTrip)

- 6.4.12 Accor SA

- 6.4.13 Marriott International

- 6.4.14 Hilton Worldwide

- 6.4.15 InterContinental Hotels Group (IHG)

- 6.4.16 Radisson Hotel Group

- 6.4.17 Melia Hotels International

- 6.4.18 NH Hotel Group

- 6.4.19 citizenM Hotels

- 6.4.20 Whitbread PLC (Premier Inn)

- 6.4.21 Travelodge UK

- 6.4.22 Sykes Holiday Cottages

- 6.4.23 Pierre & Vacances Center Parcs

- 6.4.24 ALTIDO

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment