PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044174

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044174

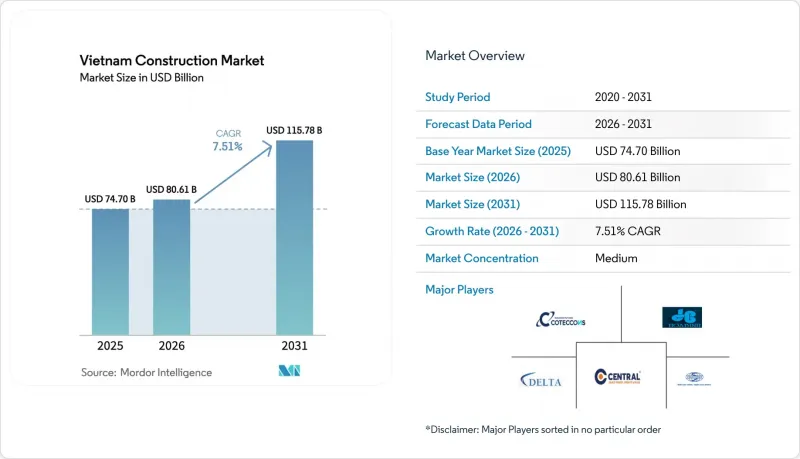

Vietnam Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Vietnam construction market size is USD 80.61 billion in 2026 and is projected to reach USD 115.78 billion by 2031 at a 7.51% CAGR.

The current upcycle is anchored by a government-led infrastructure program, a rebound in foreign direct investment to a five-year high in 2025, and the implementation of new real estate laws that together improve project bankability and execution visibility. Regulatory changes that took effect in 2024 are unlocking stalled projects and enabling more predictable permitting, which supports faster private capital mobilization into transportation, energy, and urban development. Public investment commitments for 2025 are sizable relative to GDP and are being channeled into expressways, airports, and rail corridors that prioritize national connectivity. Lower mortgage rates and a large social housing mandate are stabilizing residential demand, while manufacturing-led FDI continues to pull through industrial and logistics construction.

Vietnam Construction Market Trends and Insights

Rapid Urbanization and Housing Demand

Urbanization and new real estate laws are improving supply timelines in 2026, yet affordability and location dynamics are shaping a segmented recovery. The Ministry of Construction recorded a large affordable housing gap and reported that 102,633 social housing units were completed in 2025 toward the nationwide program, while mortgage rates remained in the 5% to 6% range to support end-user demand. Major pipeline additions are concentrated in Hanoi and Ho Chi Minh City, with several large projects moving forward post-2026, while select northern provinces are drawing new residential investment linked to manufacturing corridors. Real estate FDI picked up in 2024 and included commitments from established Asian developers such as Nomura Real Estate and local partners, reinforcing long-term housing and township plans near industrial zones. A rising share of projects target green certification pathways, which can command price premiums but also require supply chain readiness for low-carbon materials in line with Vietnam's net-zero ambitions.

Government Infrastructure and PPP Pipeline

Vietnam has enhanced its PPP framework with higher viability gap funding and revenue-sharing provisions to improve project bankability for transport, urban, and energy assets. Implementation still hinges on demand certainty for user-pay projects, and large rail proposals require substantial state support alongside private participation to proceed at scale. The model functions as co-financing in practice, with state-owned enterprises and diversified conglomerates providing anchor sponsorship on priority corridors and airports to manage delivery risk. Transit-oriented development requirements attached to new metro sections are intended to improve asset monetization, but value realization often lags until operations stabilize, which can create timing gaps for investors. Regulatory constraints on land and security interests for foreign lenders also shape financing structures and can raise all-in costs unless mitigated through local banking partnerships. Emerging green financing standards from multilaterals are pushing projects to adopt environmental management systems and product carbon verification for eligible supply chains.

Skilled-Labour Shortage and Aging Workforce

A limited pool of certified trades and steady outflows of workers to overseas markets are tightening labor availability for complex builds. The share of workers with formal vocational credentials remains low, which raises on-site training needs for contractors and lengthens mobilization for specialized scopes. Wage inflation for certified welders and specialized crews increased in 2025, and leading contractors reported margin pressure despite healthy order books. Youth underemployment and societal preferences for university tracks over technical pathways add friction to replenishing core trades. Policy measures to expand high-tech training incentives take effect in 2026 and are intended to accelerate skill localization for advanced projects.

Other drivers and restraints analyzed in the detailed report include:

- Rising FDI-led Industrial Construction

- Expansion of Renewable-Energy Projects

- Construction-Material Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential construction held a 39.10% share of the Vietnam construction market in 2025, while infrastructure recorded the fastest trajectory with an 8.88% CAGR expected through 2031. The housing program for one million social units, combined with mortgage rates at 5% to 6%, stabilizes end-user activity even as affordability limits weigh on mid-tier segments in certain provinces. Large-scale infrastructure builds include the North-South high-speed railway plan, the Long Thanh International Airport program, and expressway expansion toward a 2030 target, which together lift engineering and construction workloads. The industrial and logistics subsegment is benefiting from realized manufacturing FDI in 2025, which is the main driver for new factories, ready-built facilities, and supplier parks. Developers and EPC firms that align with tenant sustainability requirements and cleanroom or high-bay specifications are capturing the higher-value scopes.

Transportation is the central node within infrastructure, as new road, rail, and airport capacity is prioritized on economic corridors that link northern and southern regions. New rail links from border provinces to seaports and wider metro plans in both Hanoi and Ho Chi Minh City are moving through phased execution as land clearance and funding packages are sequenced. Energy and utilities require capital at scale under PDP VIII, with LNG power, wind, solar, and storage needs translating into a broad EPC opportunity set. Transmission grid projects are a critical unlock for new renewable capacity, and designated 500 kV backbones remain a priority in the current plan period. Compliance with international standards for turbines, safety systems, and monitoring is increasingly a prerequisite for financing and procurement, shaping vendor selection across energy packages.

New construction accounted for 68.10% of the Vietnam construction market in 2025, and renovation is projected to grow at a 7.99% CAGR to 2031 as owners prioritize retrofit strategies. Public investment is supporting greenfield expressways, airports, and rail, while the manufacturing pipeline sustains new industrial builds across core regions. Renovation demand is rising with the need to upgrade state-built assets and private portfolios to meet energy performance, digital infrastructure, and compliance expectations. Housing support mechanisms for social and workers' housing and policies to improve the quality and safety of older apartment stock are reinforcing the retrofit trend. Financial incentives that lower borrowing costs for eligible housing projects also encourage upgrades alongside new supply additions.

Within new construction, capital and order books are concentrated in projects above the USD 38 million threshold for transport and mega mixed-use, which account for a large value share despite a smaller project count. Renovation specialists with capabilities in adaptive reuse, energy-efficient MEP upgrades, and digital retrofits are securing premium pricing where they can lock in delivery certainty for operational sites. The policy push to digitize real estate transactions and assign digital IDs to properties will nudge owners to lift documentation, safety, and performance standards before listing or refinancing assets. The Vietnam construction industry is also seeing data infrastructure upgrades in offices, parks, and campuses to support connectivity and edge computing workloads. Projects that align with environmental management standards are better positioned to access international financing linked to climate objectives.

The Vietnam Construction Market Report is Segmented by Sector (Residential, Commercial, Infrastructure), by Construction Type (New Construction, Renovation), by Construction Method (Conventional On-Site, Modern Methods), by Investment Source (Public, Private), and by Geography (Ho Chi Minh City, Hanoi, Da Nang, Rest of Vietnam). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Coteccons Construction JSC

- Hoa Binh Construction Group JSC

- Central Construction JSC (Central Cons)

- Delta Construction Group

- Vinaconex JSC

- Unicons Investment Construction Co., Ltd.

- Ricons Construction Investment Group JSC

- Newtecons JSC

- Ecoba Vietnam JSC

- Fecon Corp JSC

- Licogi 16 JSC

- CIENCO4 Group JSC

- Deo Ca Group JSC

- An Phong Construction JSC

- Phuc Hung Holdings JSC

- CJSC - Construction Application & Transfer of Technologies JSC

- Viteccons Construction Investment JSC

- SOL E&C Investment Construction JSC

- PCC1 - Power Construction JSC No.1

- Hai Long Construction JSC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid urbanization and housing demand

- 4.2.2 Government infrastructure and PPP pipeline

- 4.2.3 Rising FDI-led industrial construction

- 4.2.4 Expansion of renewable-energy projects

- 4.2.5 Digital e-permitting accelerating approvals

- 4.2.6 Modular construction uptake by local conglomerates

- 4.3 Market Restraints

- 4.3.1 Skilled-labor shortage and aging workforce

- 4.3.2 Construction-material price volatility

- 4.3.3 Fragmented land-acquisition processes

- 4.3.4 High risk-premium on long-term project finance

- 4.4 Value / Supply-Chain Analysis

- 4.4.1 Overview

- 4.4.2 Real Estate Developers and Contractors - Key Quantitative and Qualitative Insights

- 4.4.3 Architectural and Engineering Companies - Key Quantitative and Qualitative Insights

- 4.4.4 Building Material and Equipment Companies - Key Quantitative and Qualitative Insights

- 4.5 Government Initiatives & Vision

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Industry Attractiveness - Porter's Five Force Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Consumers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing (Construction Materials) and Construction Cost (Materials, Labour, Equipment) Analysis

- 4.10 Comparison of Key Industry Metrics of the Vietnam with Other Countries

- 4.11 Key Upcoming/Ongoing Projects (with a focus on Mega Projects)

5 Market Size & Growth Forecasts

- 5.1 By Sector

- 5.1.1 Residential

- 5.1.1.1 Apartments/Condominiums

- 5.1.1.2 Villas/Landed Houses

- 5.1.2 Commercial

- 5.1.2.1 Office

- 5.1.2.2 Retail

- 5.1.2.3 Industrial and Logistics

- 5.1.2.4 Others

- 5.1.3 Infrastructure

- 5.1.3.1 Transportation Infrastructure (Roadways, Railways, Airways, others)

- 5.1.3.2 Energy & Utilities

- 5.1.3.3 Others

- 5.1.1 Residential

- 5.2 By Construction Type

- 5.2.1 New Construction

- 5.2.2 Renovation

- 5.3 By Construction Method

- 5.3.1 Conventional On-Site

- 5.3.2 Modern Methods of Construction (Prefabricated, Modular, etc)

- 5.4 By Investment Source

- 5.4.1 Public

- 5.4.2 Private

- 5.5 By Geography

- 5.5.1 Ho Chi Minh City

- 5.5.2 Hanoi

- 5.5.3 Da Nang

- 5.5.4 Rest of Vietnam

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Coteccons Construction JSC

- 6.4.2 Hoa Binh Construction Group JSC

- 6.4.3 Central Construction JSC (Central Cons)

- 6.4.4 Delta Construction Group

- 6.4.5 Vinaconex JSC

- 6.4.6 Unicons Investment Construction Co., Ltd.

- 6.4.7 Ricons Construction Investment Group JSC

- 6.4.8 Newtecons JSC

- 6.4.9 Ecoba Vietnam JSC

- 6.4.10 Fecon Corp JSC

- 6.4.11 Licogi 16 JSC

- 6.4.12 CIENCO4 Group JSC

- 6.4.13 Deo Ca Group JSC

- 6.4.14 An Phong Construction JSC

- 6.4.15 Phuc Hung Holdings JSC

- 6.4.16 CJSC - Construction Application & Transfer of Technologies JSC

- 6.4.17 Viteccons Construction Investment JSC

- 6.4.18 SOL E&C Investment Construction JSC

- 6.4.19 PCC1 - Power Construction JSC No.1

- 6.4.20 Hai Long Construction JSC

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment