PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061525

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061525

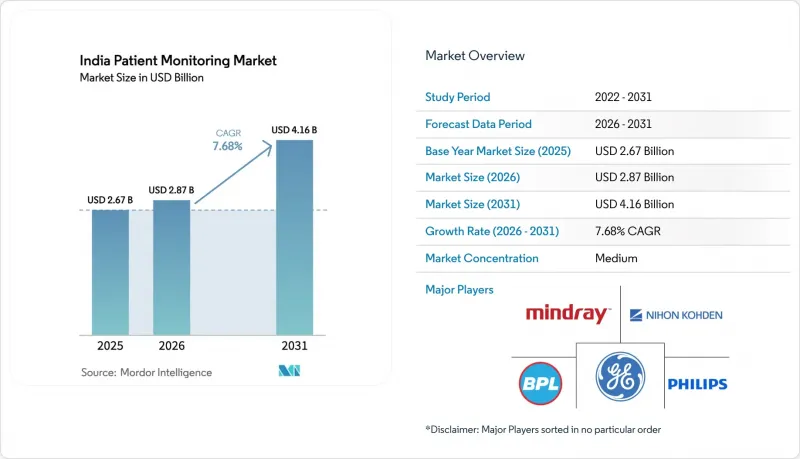

India Patient Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india patient monitoring market size is expected to increase from USD 2.67 billion in 2025 to USD 2.87 billion in 2026 and reach USD 4.16 billion by 2031, growing at a CAGR of 7.68% over 2026-2031.

This report is Segmented by Type (Devices, Services), End-User (Public Tertiary Hospitals, Private Corporate Hospitals, Specialty & Single-Specialty Clinics, Home-Healthcare Providers, Ambulatory Surgical Centers), and Application (Cardiology, Respiratory, Neurology, Critical Care (ICU/CCU), Diabetes & Metabolic, Maternal & Neonatal). The Market Forecasts are Provided in Terms of Value (USD).

India Patient Monitoring Market Trends and Insights

Rising Chronic Disease Burden

India's diabetes and hypertension prevalence is shifting episodic care toward continuous monitoring at home and in hospitals. Over 100 million adults live with diabetes and a very large hypertensive population remains undertreated, which sustains demand for home BP monitors and sensor-based glucose tracking. Cardiovascular disease contributes a significant share of national mortality, prompting tertiary hospitals to upgrade with multiparameter monitors that extend surveillance beyond manual rounds. Private corporate hospitals are deploying connected beds that integrate ECG, pulse oximetry, and scales into dashboards that help teams intervene earlier. Post-discharge cardiology and diabetes pathways increasingly rely on remote patient monitoring kits to flag arrhythmias and glucose excursions in real time. These patterns reinforce an always-on approach that supports the India patient monitoring market as chronic conditions intensify in urban and peri-urban populations.

Expansion of Telehealth Programs and Reimbursement Pilots

The Ayushman Bharat Digital Mission has created digital identities and consent rails at national scale, and several states are piloting RPM reimbursement under public insurance. Karnataka, Telangana, and Maharashtra operate pilots that reimburse virtual visits linked to device-submitted vitals, creating a funding path that did not exist before 2024. The National Health Authority is evaluating bundled chronic-care payments that include Bluetooth-enabled BP cuffs and glucometers for primary-care clinics. Platform companies integrating devices with teleconsultation workflows are offering subscription RPM packages to improve adherence and continuity of care. Although state-by-state fee schedules differ, new payment models are paving the way for wider routine monitoring and boosting the India patient monitoring market over the medium term.

High Import Dependency and Forex Volatility for Electronics/Components

Despite policy support, most monitors still depend on imported semiconductors, sensor modules, and displays, which raises exposure to currency swings and supply risk. The rupee near INR 83 per USD in 2025 raises landed costs of critical components and narrows margins for smaller manufacturers that cannot hedge or secure long-term pricing. Specialty analog front-ends and high-resolution TFT components remain concentrated in East Asian supply chains, keeping domestic makers reliant on external suppliers. Public procurement that prioritizes lowest price complicates pass-through of cost increases, especially for vendors lacking scale to absorb volatility. Plans for local semiconductor capacity are advancing, yet commercial-scale output will take time to stabilize upstream supply for patient monitoring.

Other drivers and restraints analyzed in the detailed report include:

- Government PLI and Med-Tech Clusters Accelerate Local Manufacturing

- Shift to Hospital-At-Home, Virtual ICUs, and Connected Beds in Private Chains

- Fragmented State Procurement and Tendering Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Devices captured 84.92% of revenue in 2025, and services are expanding at 9.21% CAGR through 2031, underscoring a shift toward managed operations and analytics. Multiparameter vital-signs monitors remain the workhorse across ICUs and operating rooms, with replacement cycles favoring connectivity and centralized alarm management. Cardiac monitoring, including Holter and event recorders, is expanding among urban cardiologists for outpatient arrhythmia workups supported by rapid interpretation. Respiratory devices such as pulse oximeters, capnographs, and spirometers maintain elevated use given persistent COPD and asthma burdens and the emphasis on perioperative safety. Fetal and neonatal monitoring continues to build in tertiary maternity centers while neonatal ICU capacity in tier-2 cities increases the installed base. Neuro-monitoring and hemodynamic sensors gain traction in trauma and critical care, while wearable patches and contactless sensors are the fastest-growing form factors as clinical-grade consumer wearables converge with care delivery.

Services are gaining share as hospitals pursue continuous oversight without expanding onsite headcount, and as providers prioritize interoperability, analytics, and uptime. Remote monitoring and telehealth services benefit from reimbursement pilots that package devices and clinician review into per-member payments. Data-integration and interoperability services are critical for bridging device protocols with ABDM-aligned exchanges and hospital HIMS, which requires custom middleware development. Managed-monitoring operations staffed by nurses and respiratory therapists triage alarms across sites to improve response times and standardize workflows. Training services remain underpenetrated, and structured programs for alarm management and artifact recognition could reduce false alerts and improve frontline confidence across the India patient monitoring industry.

List of Companies Covered in this Report:

- Abbott Laboratories

- Baxter International Inc. (Hillrom/Welch Allyn)

- Beckton Dickinson

- BPL

- Dexcom

- Dozee (TurtleShell Technologies)

- Dragerwerk

- Edward Lifesciences

- F. Hoffmann La Roche AG

- GE HealthCare Technologies Inc.

- HealthCube India

- ICU Medical

- Koninklijke Philips

- LifeSigns (Re'bu Health)

- Masimo

- Medtronic

- Mindray Bio Medical Electronics Co., Ltd.

- Nihon Kohden

- Omron Healthcare Co., Ltd. (India)

- Schiller

- Siemens Healthineers

- Skanray Technologies Ltd.

- Spacelabs Healthcare (OSI Systems)

- Stasis Health

- Ten3T Healthcare Pvt. Ltd.

- Tracky (DrStore Healthcare)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Chronic Disease Burden

- 4.2.2 Expansion of Telehealth Programs and Reimbursement Pilots

- 4.2.3 Government PLI And Med-Tech Clusters Accelerate Local Manufacturing

- 4.2.4 Shift to Hospital-At-Home, Virtual ICUs, and Connected Beds in Private Chains

- 4.2.5 Growing Adoption of AI-Powered Analytics in Monitoring Workflows

- 4.2.6 Rapid Penetration of Low-Cost Wearables/India-First Sensors Enabling RPM at Scale

- 4.3 Market Restraints

- 4.3.1 High Import Dependency and Forex Volatility For Electronics/Components

- 4.3.2 Fragmented State Procurement and Tendering Complexity

- 4.3.3 Low Physician Adoption of Home BP/RPM Protocols in Primary Care

- 4.3.4 Data-Privacy and Device-EHR/HIMS Integration Gaps vs ABDM Consent Rails

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, in USD)

- 5.1 By Type

- 5.1.1 Device Type

- 5.1.1.1 Multiparameter Vital-Signs Monitors

- 5.1.1.2 Cardiac Monitoring Devices

- 5.1.1.3 Respiratory Monitoring Devices

- 5.1.1.4 Fetal & Neonatal Monitoring Devices

- 5.1.1.5 Neuro-Monitoring Devices

- 5.1.1.6 Hemodynamic & Pressure Monitoring Devices

- 5.1.1.7 Remote Patient Monitoring Kits

- 5.1.1.8 Wearable Sensors & Patches

- 5.1.2 By Service/Offering

- 5.1.2.1 Installation & Maintenance Services

- 5.1.2.2 Training & Education Services

- 5.1.2.3 Remote Monitoring & Telehealth Services

- 5.1.2.4 Data Integration & Interoperability Services

- 5.1.2.5 Analytics & Reporting Services

- 5.1.2.6 Managed Monitoring Operations & Triage Services

- 5.1.1 Device Type

- 5.2 By End-User

- 5.2.1 Public Tertiary Hospitals

- 5.2.2 Private Corporate Hospitals

- 5.2.3 Specialty & Single-Specialty Clinics

- 5.2.4 Home-Healthcare Providers

- 5.2.5 Ambulatory Surgical Centers

- 5.3 By Application

- 5.3.1 Cardiology

- 5.3.2 Respiratory

- 5.3.3 Neurology

- 5.3.4 Critical Care (ICU/CCU)

- 5.3.5 Diabetes & Metabolic

- 5.3.6 Maternal & Neonatal

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Baxter International Inc. (Hillrom/Welch Allyn)

- 6.3.3 BeatO

- 6.3.4 BPL Medical Technologies

- 6.3.5 Dexcom, Inc.

- 6.3.6 Dozee (TurtleShell Technologies)

- 6.3.7 Dragerwerk AG & Co. KGaA

- 6.3.8 Edwards Lifesciences

- 6.3.9 F. Hoffmann La Roche AG

- 6.3.10 GE HealthCare Technologies Inc.

- 6.3.11 HealthCube India

- 6.3.12 ICU Medical Inc.

- 6.3.13 Koninklijke Philips N.V.

- 6.3.14 LifeSigns (Re'bu Health)

- 6.3.15 Masimo Corporation

- 6.3.16 Medtronic plc

- 6.3.17 Mindray Bio Medical Electronics Co., Ltd.

- 6.3.18 Nihon Kohden Corporation

- 6.3.19 Omron Healthcare Co., Ltd. (India)

- 6.3.20 Schiller AG

- 6.3.21 Siemens Healthineers AG

- 6.3.22 Skanray Technologies Ltd.

- 6.3.23 Spacelabs Healthcare (OSI Systems)

- 6.3.24 Stasis Health

- 6.3.25 Ten3T Healthcare Pvt. Ltd.

- 6.3.26 Tracky (DrStore Healthcare)

7 Market Opportunities & Future Outlook

- 7.1 White?space & Unmet?Need Assessment