PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061568

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061568

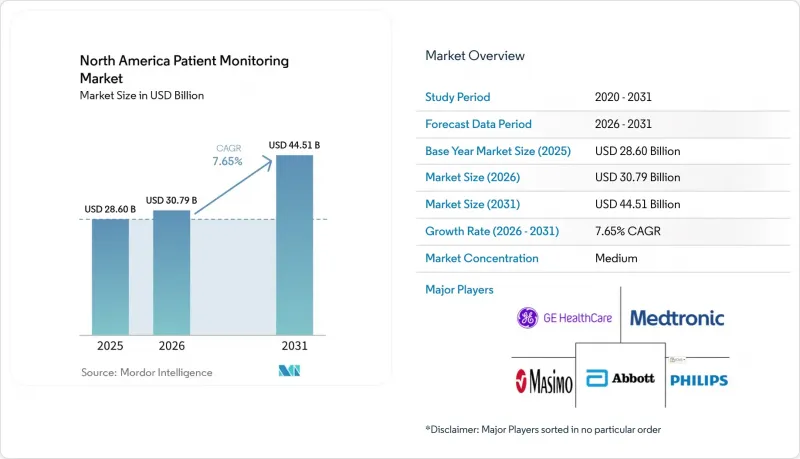

North America Patient Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the north america patient monitoring market size was valued at USD 28.60 billion in 2025 and is estimated to grow from USD 30.79 billion in 2026 to reach USD 44.51 billion by 2031, at a CAGR of 7.65% during the forecast period (2026-2031).

This report is Segmented by Type (Device [Hemodynamic, Neuromonitoring, Cardiac, Multi-Parameter, and More] Service [Installation & Maintenance, Training & Education, and More), Application (Cardiology, Neurology, Respiratory, and More), End User (Hospitals & Clinics, Home Healthcare, Ambulatory & Specialty Centers), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America Patient Monitoring Market Trends and Insights

Incidence of Chronic & Lifestyle Diseases Surging

More than 133 million U.S. adults live with chronic illness, and 6 in 10 manage at least one condition, driving sustained demand for round-the-clock monitoring. Prevalence climbs further in the 85-plus cohort, where multi-morbidity reached 12.3% in 2024, intensifying care complexity. Continuous glucose monitors illustrate the trend: Dexcom's Stelo sensor broadened eligibility beyond insulin users, contributing to a 21.6% revenue jump to USD 1.21 billion in Q3 2025. Abbott's Libre Rio and Lingo followed, pushing adoption into the 37 million U.S. Type 2 population. Each new chronic-care enrollee expands the North America patient monitoring market, because payers now reimburse multi-condition oversight under bundled RPM codes.

Ageing Population & Reimbursement Expansion

Seniors will form 21.6% of North America's population by 2030, and they consume triple the monitoring resources of younger adults. CMS lifted CPT 99457 to USD 64.41 and added CPT 99458 at USD 51.52 for every extra 20 minutes of review, letting clinics bill for layered comorbidity tracking. Canada's Connected Care Act mirrors the move, while Ontario earmarks CAD 832 million (USD 615 million) annually for digital care. TELUS Health's province-wide RPM program already enrolls thousands, demonstrating how reimbursement certainty converts pilots into mainstream workflows.

Provider Workflow Resistance & Training Burden

Alarm overload erodes trust: a UPMC audit logged 65.6 million alerts across wards, 88% technical rather than physiologic, fueling burnout in 40-50% of staff. Every platform introduces new dashboards, thresholds, and escalation drills, requiring months of coaching. Emory Healthcare's 2025 virtual-nursing project came with a six-month curriculum and extra staffing. Small hospitals lack volume to justify centralized command centers, limiting adoption and tempering short-run gains in the North America patient monitoring market.

Other drivers and restraints analyzed in the detailed report include:

- Post-COVID Preference for Home & Remote Monitoring

- AI-Enabled Early-Warning Analytics

- High Capital & Integration Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware generated 80.18% of 2025 revenue, yet service lines are forecast to deliver an 8.22% CAGR, the quickest in the North America patient monitoring market. Hoag Memorial's decade-long lease with Philips shows why: hospitals spread payments, lock in upgrades, and secure analytics without large upfront checks. Managed monitoring, middleware development, and triage outsourcing now command premium pricing, turning services into a strategic hedge against hardware commoditization. The North America patient monitoring market size for services is projected to expand faster than devices as more systems convert capex to opex.

Analytics and command-center operations deepen stickiness. West Tennessee Healthcare added 12 intensivists to staff its eICU in 2025, giving rural affiliates 24/7 oversight. Middleware spending, USD 25 million at Parrish Healthcare, shows that interoperability remains a bottleneck. As proprietary data standards fade, vendors able to bundle cloud hosting, cybersecurity, and AI analytics win renewals, reinforcing vendor lock-in across the North America patient monitoring market.

List of Companies Covered in this Report:

- Abbott Laboratories

- Baxter

- Beckton Dickinson

- BIOTRONIK

- Boston Scientific

- Dexcom

- Edward Lifesciences

- GE HealthCare Technologies Inc.

- Honeywell International

- iRhythm Technologies

- Johnson & Johnson

- Koninklijke Philips

- Masimo

- Medtronic

- Nihon Kohden

- Omron Healthcare Co. Ltd.

- Resmed

- Siemens Healthineers

- Teladoc Health

- VitalConnect Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Incidence of Chronic & Lifestyle Diseases Surging

- 4.2.2 Ageing Population & Reimbursement Expansion

- 4.2.3 Post-COVID Preference for Home & Remote Monitoring

- 4.2.4 Ai-Enabled Early-Warning Analytics

- 4.2.5 Shift Toward Single-Use Sensors

- 4.2.6 Federal RPM Code Revisions

- 4.3 Market Restraints

- 4.3.1 Provider Workflow Resistance & Training Burden

- 4.3.2 High Capital & Integration Costs

- 4.3.3 Cyber-Insurance & Section-524B Compliance

- 4.3.4 Clinician Alert-Fatigue

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter?s Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 By Device

- 5.1.1.1 Hemodynamic Monitoring Devices

- 5.1.1.2 Neuromonitoring Devices

- 5.1.1.3 Cardiac Monitoring Devices

- 5.1.1.4 Multi-Parameter Monitors

- 5.1.1.5 Respiratory Monitoring Devices

- 5.1.1.6 Remote Patient Monitoring Devices

- 5.1.1.7 Other Devices

- 5.1.2 By Service

- 5.1.2.1 Installation & Maintenance Services

- 5.1.2.2 Training & Education Services

- 5.1.2.3 Remote Monitoring & Telehealth Services

- 5.1.2.4 Data Integration & Interoperability Services

- 5.1.2.5 Analytics & Reporting Services

- 5.1.2.6 Managed Monitoring Operations & Triage Services

- 5.1.1 By Device

- 5.2 By Application

- 5.2.1 Cardiology

- 5.2.2 Neurology

- 5.2.3 Respiratory

- 5.2.4 Diabetes Management

- 5.2.5 Fetal & Neonatal

- 5.2.6 Weight-Management & Fitness

- 5.2.7 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Home Healthcare

- 5.3.3 Ambulatory & Specialty Centers

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Baxter International Inc.

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Biotronik SE & Co. KG

- 6.3.5 Boston Scientific Corporation

- 6.3.6 Dexcom Inc.

- 6.3.7 Edwards Lifesciences Corporation

- 6.3.8 GE HealthCare Technologies Inc.

- 6.3.9 Honeywell International Inc.

- 6.3.10 iRhythm Technologies Inc.

- 6.3.11 Johnson & Johnson

- 6.3.12 Koninklijke Philips N.V.

- 6.3.13 Masimo Corporation

- 6.3.14 Medtronic plc

- 6.3.15 Nihon Kohden Corporation

- 6.3.16 Omron Healthcare Co. Ltd.

- 6.3.17 ResMed Inc.

- 6.3.18 Siemens Healthineers GmbH

- 6.3.19 Teladoc Health Inc.

- 6.3.20 VitalConnect Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment