PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061563

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061563

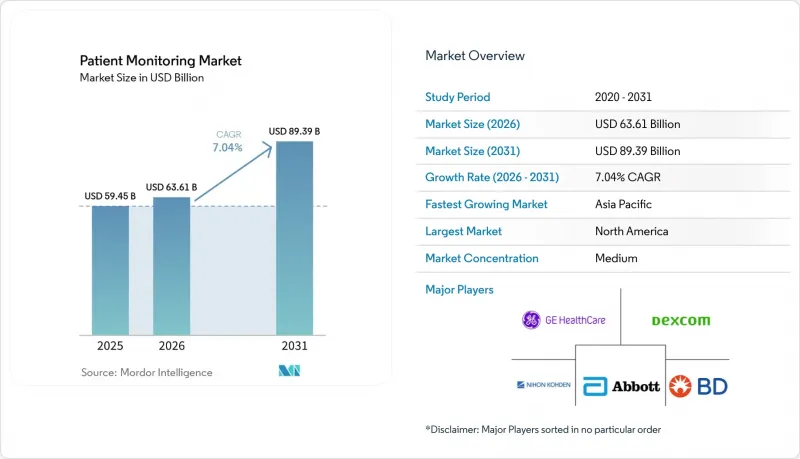

Patient Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the patient monitoring market size was valued at USD 59.45 billion in 2025 and is estimated to grow from USD 63.61 billion in 2026 to reach USD 89.39 billion by 2031, at a CAGR of 7.04% during the forecast period (2026-2031).

This report is Segmented by Type (Device [Cardiac Monitoring Devices, and More], Services [Training & Education, and More]), Application (Cardiology, Respiratory, Neurology, and More), End-User (Hospitals, Specialty & Single-Specialty Clinics, Ambulatory Surgical Centers, Home-Healthcare Providers, and More), and Geography (North America and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Patient Monitoring Market Trends and Insights

Rise in Chronic-Disease Prevalence & Comorbidity Clusters

Cardiovascular diseases caused 17.9 million deaths in 2021, and the International Diabetes Federation projects 783 million adults living with diabetes by 2045, a 46% surge that will overwhelm episodic clinic care . Multiparameter hubs that simultaneously track glucose, blood pressure, and weight are therefore gaining favor over single-parameter devices. The CDC reported in 2024 that 6 in 10 U.S. adults have at least one chronic condition and 4 in 10 have two or more, underscoring demand for continuous surveillance outside hospitals. Value-based contracts penalizing readmissions are pushing providers to deploy post-discharge monitoring that flags decompensation early. As interoperability improves, integrated platforms are expected to crowd out legacy stand-alone monitors within the patient monitoring market.

Accelerating Shift to Hospital-at-Home & Virtual Wards

CMS transitioned its Acute Hospital Care at Home waiver into a permanent pathway in 2025, covering 290 hospitals across 37 states. The United Kingdom scaled virtual wards to more than 10,000 beds by mid-2024, freeing acute-care capacity. Hospital-at-home models require rugged, patient-operated devices that can transmit vitals via cellular or satellite gateways without onsite clinicians. Philips and GE HealthCare now bundle monitors, connectivity, and managed triage into per-patient subscriptions, converting capital expenditure to operating expense. As reimbursement converges across payers, adoption is widening among mid-size community hospitals, thereby broadening the patient monitoring market footprint

Escalating Cybersecurity Insurance Premiums for Connected Devices

FDA Section 524B rules, effective June 2025, now demand software bills of materials and threat-modeling for every networked device, increasing compliance spend and driving insurance carriers to hike healthcare cyber-premiums 15-25%. For a 500-bed hospital, annual coverage can reach USD 300,000, exceeding amortized hardware costs over a seven-year cycle. Smaller hospitals, lacking full-time security staff, either delay purchases or accept higher risk, curbing near-term orders in the market and slowing patient monitoring market size expansion.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Early-Warning Systems Lowering Adverse-Event Costs

- Reimbursement Expansion for Remote Physiologic Monitoring (RPM)

- High Total-Cost-of-Ownership in Low-Resource Settings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Devices retained 83.1% of the patient monitoring market share in 2025, supported by large ICU and step-down installed bases. However, services revenue spanning installation, data integration, analytics, and managed triage is forecast to grow 9.53% from 2026 to 2031, outpacing the overall patient monitoring market by 2.5 percentage points. Hospital executives prefer subscription bundles that convert capital outlays into predictable operating costs, and vendors such as GE HealthCare and Philips now tie monthly fees to active-patient counts rather than hardware units.

Wearable and patch-based monitors are expanding fastest within hardware, propelled by over-the-counter CGMs like Dexcom Stelo and Abbott Libre Rio that address wellness and prediabetes segments. Remote hubs face commoditization as smartphones offer built-in Bluetooth and LTE, pushing value toward cloud analytics. Consequently, the patient monitoring market size for device-only contracts is expected to plateau, while as-a-service models capture incremental spend.

Geography Analysis

North America generated 41.2% of 2025 revenue, buoyed by CMS RPM reforms, Section 524B cybersecurity mandates, and a robust hospital-at-home infrastructure. The region's high average selling prices and payer willingness to reimburse managed services underpin its outsized contribution to the patient monitoring market size.

Europe holds significant share, supported by Germany's DiGA reimbursement pathway and the United Kingdom's virtual-ward expansion. EU Medical Device Regulation enforcement raised compliance costs but improved post-market surveillance, reinforcing trust among clinicians. Despite macroeconomic pressures, statutory insurers continue to fund connected-care pilots, stabilizing demand.

Asia-Pacific is the growth engine, forecast to post a 10.99% CAGR from 2026 to 2031. China's NMPA approved more than 50 AI-enabled monitors in 2024-2025, while India liberalized telemedicine and Japan expanded coverage for remote COPD and heart-failure monitoring. These policy shifts, coupled with aging demographics, enlarge the patient monitoring market across populous economies. Middle East and Africa remain early-stage, yet Gulf Cooperation Council investments in smart hospitals are expected to seed future demand. South America shows selective uptake, led by private payers in Brazil.

- Abbott Laboratories

- Baxter

- Beckton Dickinson

- BIOTRONIK

- Contec Medical Systems

- Dexcom

- Dragerwerk

- Garmin

- GE HealthCare Technologies Inc.

- Honeywell International

- iRhythm Technologies

- Koninklijke Philips

- Masimo

- Medtronic

- Nihon Kohden

- OMRON

- Resmed

- Schiller

- Mindray

- Spire Health

- VitalConnect Inc.

- Zoll Medical Corporation (Asahi Kasei Group)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise In Chronic-Disease Prevalence & Comorbidity Clusters

- 4.2.2 Accelerating Shift to Hospital-At-Home & Virtual Wards

- 4.2.3 AI-Enabled Early-Warning Systems Lowering Adverse-Event Costs

- 4.2.4 Reimbursement Expansion for Remote Physiologic Monitoring (RPM)

- 4.2.5 Edge-Computing Wearables Reducing Data-Latency Below 20 Ms

- 4.2.6 Satellite-IoT Backhaul Unlocking Monitoring In Connectivity Blackspots

- 4.3 Market Restraints

- 4.3.1 Escalating Cybersecurity Insurance Premiums for Connected Devices

- 4.3.2 High Total-Cost-Of-Ownership in Low-Resource Settings

- 4.3.3 Fragmented Device-Data Standards Hindering Interoperability

- 4.3.4 Lithium-Supply Volatility Inflating Wearable-Battery Costs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, in USD)

- 5.1 By Type

- 5.1.1 Device

- 5.1.1.1 Multiparameter Vital-Signs Monitors

- 5.1.1.2 Cardiac Monitoring Devices

- 5.1.1.3 Respiratory Monitoring Devices

- 5.1.1.4 Neuro-Monitoring Devices

- 5.1.1.5 Fetal & Neonatal Monitoring Devices

- 5.1.1.6 Hemodynamic & Pressure Monitors

- 5.1.1.7 Wearable & Patch-Based Monitors

- 5.1.1.8 Remote Patient Monitoring Hubs & Gateways

- 5.1.1.9 AI-Driven Predictive Analytics Modules

- 5.1.2 Services

- 5.1.2.1 Installation & Maintenance

- 5.1.2.2 Training & Education

- 5.1.2.3 RPM & Telehealth Services

- 5.1.2.4 Data Integration & Interoperability

- 5.1.2.5 Analytics & Reporting

- 5.1.2.6 Managed Monitoring & Triage Operations

- 5.1.1 Device

- 5.2 By Application

- 5.2.1 Cardiology

- 5.2.2 Respiratory

- 5.2.3 Neurology

- 5.2.4 Diabetes & Metabolic

- 5.2.5 Maternal & Neonatal

- 5.2.6 Critical Care Surveillance

- 5.2.7 Others

- 5.3 By End-User

- 5.3.1 Hospitals

- 5.3.2 Specialty & Single-Specialty Clinics

- 5.3.3 Ambulatory Surgical Centers

- 5.3.4 Home-Healthcare Providers

- 5.3.5 Long-Term Care & Assisted-Living Facilities

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Baxter International Inc.

- 6.3.3 Becton Dickinson & Company

- 6.3.4 Biotronik SE & Co. KG

- 6.3.5 Contec Medical Systems Co., Ltd.

- 6.3.6 Dexcom, Inc.

- 6.3.7 Dragerwerk AG & Co. KGaA

- 6.3.8 Garmin Ltd.

- 6.3.9 GE HealthCare Technologies Inc.

- 6.3.10 Honeywell International Inc.

- 6.3.11 iRhythm Technologies, Inc.

- 6.3.12 Koninklijke Philips N.V.

- 6.3.13 Masimo Corporation

- 6.3.14 Medtronic plc

- 6.3.15 Nihon Kohden Corporation

- 6.3.16 OMRON Corporation

- 6.3.17 ResMed Inc.

- 6.3.18 Schiller AG

- 6.3.19 Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- 6.3.20 Spire Health

- 6.3.21 VitalConnect Inc.

- 6.3.22 Zoll Medical Corporation (Asahi Kasei Group)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment