PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061729

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061729

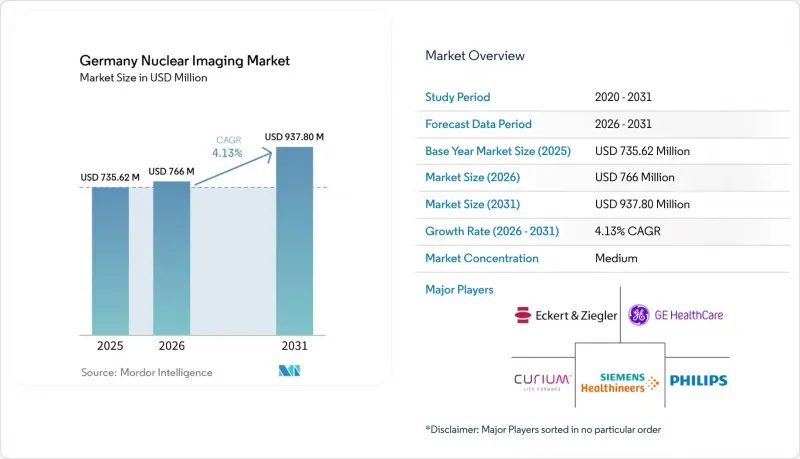

Germany Nuclear Imaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany nuclear imaging market size was valued at USD 735.62 million in 2025 and is estimated to grow from USD 766 million in 2026 to reach USD 937.80 million by 2031, at a CAGR of 4.13% during the forecast period (2026-2031).

This report is Segmented by Equipment (PET Scanners, SPECT Scanners), Modality (SPECT Cameras, PET/CT Scanners, PET/MRI Scanners, Hybrid SPECT/CT), Radio-Isotope (99mTc, 18F, 68ga, 177lu, Others), Application (Oncology, Cardiology, Neurology, Endocrinology, Others). The Market Forecasts are Provided in Terms of Value (USD).

Germany Nuclear Imaging Market Trends and Insights

Cancer & CVD Prevalence Surge

Growing incidence of oncology and cardiac disease keeps scan volumes on an upward trajectory. Broader reimbursement for PET/MRI in neurology and cardiology is unlocking pent-up demand while technetium-99m myocardial perfusion SPECT maintains dominance for ischemia work-ups. Novel tracers such as fluorine-18-florbetaben for cardiac amyloidosis and PSMA agents for prostate cancer further widen clinical utility, underpinning sustained growth across modalities through 2031. Aging demographics ensure a continuous flow of complex cases that require follow-up imaging, embedding multiphase PET protocols into routine care. As guideline updates recommend earlier PET staging, scan frequency per patient continues to rise, reinforcing recurring revenue for equipment vendors and isotope suppliers.

Federal PET/CT-CapEx Grants (German Cancer Aid)

Targeted grants are narrowing the technology gap between university and regional hospitals. Recipients must install digital PET/CT with dose-tracking software and convene multidisciplinary tumor boards, structurally embedding PET scans into care pathways. Digital detectors deliver up to 40% dose reduction, enabling pediatric protocols while supporting higher patient throughput that improves return on investment. The grant mechanism also stipulates public reporting of utilization metrics, increasing transparency and spurring peer adoption. With Germany's National Cancer Plan prioritizing precision oncology, additional rounds of funding are anticipated, keeping the capital pipeline flowing for the Germany nuclear imaging market.

High Equipment CAPEX & Maintenance Costs

List prices of USD 2-3.5 million for digital PET/CT and more than USD 4 million for PET/MRI strain hospital budgets, while service contracts add 8-10% of purchase value annually. Retrofitting legacy facilities to comply with new shielding rules can exceed USD 1 million. These economics concentrate capacity at university centers and large private chains, curbing geographic penetration of the Germany nuclear imaging market. Pay-per-scan leasing offers relief yet demands guaranteed volumes that small clinics struggle to achieve.

Other drivers and restraints analyzed in the detailed report include:

- On-Site Cyclotron Expansions Improve Tracer Supply

- Theranostic Lu-177-PSMA Adoption Boosts Imaging Volumes

- Tc-99m & Ga-68 Supply Interruptions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PET platforms delivered 55.55% of the Germany nuclear imaging market share in 2025, anchored by oncology staging and follow-up. Transitioning to digital silicon photomultipliers pushes time-of-flight resolution below 200 ps, slicing dose 30-40% without losing contrast. The Germany nuclear imaging market size for digital PET scanners is forecast to widen further as total-body models amortize faster by doubling throughput. SPECT systems currently trail yet are projected to outpace PET growth at a 5.85% CAGR through 2031 as quantitative platforms like xSPECT Quant provide dosimetry for lutetium-177 therapy.

Hybrid SPECT/CT is now the de-facto specification, displacing standalone cameras. GE's StarGuide integrates deep-learning reconstruction that halves acquisition time while improving lesion conspicuity. Regulatory insistence on automated dose tracking tips buyer preference toward premium vendors, consolidating share among Siemens, GE and Philips. These trends pivot capital budgets toward systems that support theranostic workflows, reinforcing revenue momentum across the Germany nuclear imaging market.

PET/CT dominated with 60.53% of modality revenue in 2025, yet PET/MRI is set to grow 6.75% CAGR as simultaneous anatomical-functional acquisition avoids CT dose-vital for pediatrics and neurology. Reimbursement gaps persist, but advocacy could unlock wider uptake by 2028. The Germany nuclear imaging market size attributable to PET/MRI remains modest, but expanding neurology protocols and prostate workflows indicate accelerating penetration.

Hybrid SPECT/CT maintains a stable cardiology and bone-scan niche. Rising cardiac amyloidosis awareness may reinvigorate SPECT growth via iodine-123-MIBG studies, while PET/CT challengers from Canon and United Imaging compete on price and service, appealing to regional hospitals. Survey data show 92% of new German installs since 2023 are hybrid, signaling an irreversible market shift toward multimodal scanners that future-proof clinical versatility.

List of Companies Covered in this Report:

- ABX advanced biochemical compounds

- Advanced Accelerator Applications (Novartis)

- Canon

- Curium Pharma

- Eckert & Ziegler AG

- GE Healthcare

- GEOMEDIS GmbH

- Hermes Medical Solutions

- ITM Isotope Technologies Munich SE

- Mediso Medical Imaging

- Oncovision

- Koninklijke Philips

- Siemens Healthineers

- Spectrum Dynamics Medical

- United Imaging Healthcare

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cancer & CVD prevalence surge

- 4.2.2 Federal PET/CT-CapEx grants (German Cancer Aid)

- 4.2.3 On-site cyclotron expansions improve tracer supply

- 4.2.4 Theranostic Lu-177-PSMA adoption boosts imaging volumes

- 4.2.5 Roll-out of total-body PET + AI workflow optimisation

- 4.2.6 DRG 39301 outpatient reimbursement uplift

- 4.3 Market Restraints

- 4.3.1 High equipment CAPEX & maintenance costs

- 4.3.2 Tc-99m & Ga-68 supply interruptions

- 4.3.3 Stricter 2024 Radiation Protection Act licensing

- 4.3.4 Workforce shortage in rural nuclear-imaging sites

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Equipment

- 5.1.1 PET Scanners

- 5.1.2 SPECT Scanners

- 5.2 By Modality

- 5.2.1 SPECT Cameras

- 5.2.2 PET/CT Scanners

- 5.2.3 PET/MRI Scanners

- 5.2.4 Hybrid SPECT/CT

- 5.3 By Radio-isotope

- 5.3.1 99mTc

- 5.3.2 18F

- 5.3.3 68Ga

- 5.3.4 177Lu

- 5.3.5 Others (64Cu, 89Zr, etc.)

- 5.4 By Application

- 5.4.1 Oncology

- 5.4.2 Cardiology

- 5.4.3 Neurology

- 5.4.4 Endocrinology

- 5.4.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 ABX advanced biochemical compounds

- 6.3.2 Advanced Accelerator Applications (Novartis)

- 6.3.3 Canon Medical Systems

- 6.3.4 Curium Pharma

- 6.3.5 Eckert & Ziegler AG

- 6.3.6 GE Healthcare

- 6.3.7 GEOMEDIS GmbH

- 6.3.8 Hermes Medical Solutions

- 6.3.9 ITM Isotope Technologies Munich SE

- 6.3.10 Mediso Medical Imaging

- 6.3.11 Oncovision

- 6.3.12 Philips

- 6.3.13 Siemens Healthineers

- 6.3.14 Spectrum Dynamics Medical

- 6.3.15 United Imaging Healthcare

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment