PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063682

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063682

Italy Nuclear Imaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

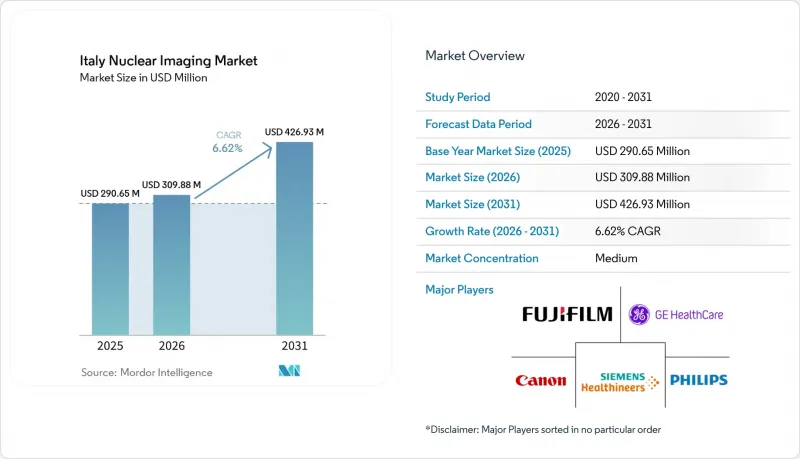

According to Mordor Intelligence, the italy nuclear imaging market size is projected to expand from USD 290.65 million in 2025 and USD 309.88 million in 2026 to USD 426.93 million by 2031, registering a CAGR of 6.62% between 2026 to 2031.

This report is Segmented by Product (Equipment, Radioisotopes [SPECT Radioisotopes {Technetium-99m (Tc-99m) and More} and PET Radioisotopes]), Application (Cardiology, Neurology, Thyroid, Oncology, and Other Applications), End User (Hospitals, Diagnostic Imaging Centres, and Academic & Research Institutes). The Market Forecasts are Provided in Terms of Value (USD).

Italy Nuclear Imaging Market Trends and Insights

Rising Incidence of Cancer & CVD

New cancer diagnoses in Italy climbed to 390,700 in 2022, up 14,100 from 2020, with breast, colorectal, and lung cancers topping incidence charts. Mortality projections for 2025 signal a 3.5% national decline, yet aging cohorts continue to push demand for precise staging and therapy monitoring through PET/CT imaging. Hybrid modalities now influence treatment decisions in more than 42% of differentiated thyroid carcinoma cases, highlighting clinical reliance on molecular imaging. Cardiovascular disease persists as the primary mortality cause, and Tc-99m SPECT remains routine for perfusion assessment, reinforcing baseline procedure volumes.

Growing Adoption of Hybrid PET/CT & SPECT/CT

Italian participation in Europe-wide multimodality imaging surveys shows steady acceleration of PET/CT rollouts, with 18F-FDG dominating tracer use. University of Padua researchers recorded 100% sensitivity and 96% accuracy for [18F]FDG PET/MRI in hepatocellular carcinoma surveillance after liver transplantation, outperforming conventional protocols. A 502-patient multicenter trial demonstrated that segmental PET/CT lowers radiation dose without diagnostic compromise in solitary pulmonary nodules, supporting guideline updates. Northern centers advance niche tracers such as 64CuCl2 for bladder cancer staging, reinforcing regional leadership.

High Equipment Capital & Maintenance Costs

PET/CT platforms cost EUR 4 million (USD 4.68 million) and frequently require bunker upgrades, straining hospital budgets that already allocate nearly 77.45% of operational spending to facility management. Aging buildings, 70% surpassing their designed 50-year lifecycle, magnify retrofit expenses, especially in Southern provinces with fewer tertiary centers. Maintenance contracts with multinational OEMs add long-term overhead, prompting some regions to defer scanner refresh cycles and rely on referral flows to Northern hubs.

Other drivers and restraints analyzed in the detailed report include:

- Favorable Reimbursement Framework

- Increase in Public-Private Investment for Nuclear-Medicine Suites

- Mo-99/Tc-99m Supply Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Equipment retained 63.55% Italy nuclear imaging market share in 2025 as hospitals prioritized PET/CT and SPECT/CT replacements to meet hybrid-imaging demand. Lombardy, Veneto, and Emilia-Romagna collectively host the densest scanner fleets, benefiting from consistent SSN reimbursements and regional budget surpluses. The radioisotope segment advances at a 6.75% CAGR, buoyed by expanding Ga-68 and Lu-177 pipelines that support theranostic protocols. Cyclotron-based production shortens supply chains and elevates the Italy nuclear imaging market size for isotopes, particularly as LARAMED scales multi-curie outputs. Northern laboratories integrate artificial-intelligence-driven QC systems to optimize batch scheduling and reduce waste, a practice expected to cascade nationwide.

Adoption of energy-efficient digital scanners tempers hospital utility overhead and aligns with EU Green Deal directives, strengthening capital-expenditure cases. Vendor service-as-a-subscription models further mitigate upfront cost, encouraging smaller Southern facilities to enter the modality mix, albeit at slower cadence. Continuous performance upgrades, such as extended axial field-of-view detectors, are forecast to keep equipment leading Italy nuclear imaging market revenues through 2031.

List of Companies Covered in this Report:

- Alliance Medical (Life Healthcare Group)

- Bracco Imaging S.p.A.

- Cardinal Health

- Curium Pharma

- GE Healthcare

- Koninklijke Philips

- NTP Radioisotopes

- Siemens Healthineers

- Telix Pharmaceuticals Ltd.

- Canon

- FUJIFILM

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising incidence of cancer & CVD

- 4.2.2 Growing adoption of hybrid PET/CT & SPECT/CT

- 4.2.3 Favorable reimbursement framework (SSN tariffs)

- 4.2.4 Increase in public-private investment for nuclear-medicine suites

- 4.2.5 Expansion of theranostic radioisotope production in Northern Italy

- 4.2.6 Adoption of cyclotron-based Ga-68 generators in regional radiopharmacies

- 4.3 Market Restraints

- 4.3.1 High equipment capital & maintenance costs

- 4.3.2 Mo-99 / Tc-99m supply bottlenecks

- 4.3.3 Radiation-dose safety & regulatory scrutiny

- 4.3.4 Emerging photon-counting CT substitution risk

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Equipment

- 5.1.2 Radioisotopes

- 5.1.2.1 SPECT Radioisotopes

- 5.1.2.1.1 Technetium-99m (Tc-99m)

- 5.1.2.1.2 Thallium-201 (Tl-201)

- 5.1.2.1.3 Gallium-67 (Ga-67)

- 5.1.2.1.4 Iodine-123 (I-123)

- 5.1.2.1.5 Other SPECT Isotopes

- 5.1.2.2 PET Radioisotopes

- 5.1.2.2.1 Fluorine-18 (F-18)

- 5.1.2.2.2 Rubidium-82 (Rb-82)

- 5.1.2.2.3 Other PET Isotopes

- 5.1.2.1 SPECT Radioisotopes

- 5.2 By Application

- 5.2.1 Cardiology

- 5.2.2 Neurology

- 5.2.3 Thyroid

- 5.2.4 Oncology

- 5.2.5 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Diagnostic Imaging Centres

- 5.3.3 Academic & Research Institutes

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Alliance Medical (Life Healthcare Group)

- 6.3.2 Bracco Imaging S.p.A.

- 6.3.3 Cardinal Health Inc.

- 6.3.4 Curium Pharma

- 6.3.5 GE HealthCare

- 6.3.6 Koninklijke Philips N.V.

- 6.3.7 NTP Radioisotopes

- 6.3.8 Siemens Healthineers

- 6.3.9 Telix Pharmaceuticals Ltd.

- 6.3.10 Canon Medical Systems Corporation

- 6.3.11 Fujifilm Holdings Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment