PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072557

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2072557

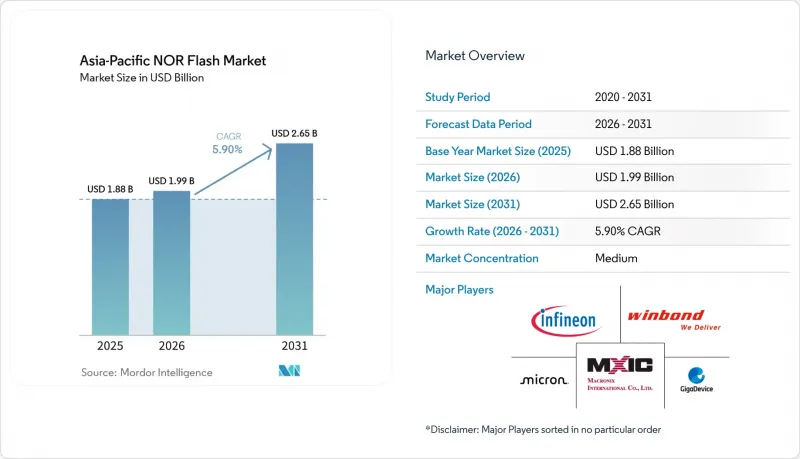

Asia-Pacific NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific NOR flash market size is expected to grow from USD 1.88 billion in 2025 to USD 1.99 billion in 2026 and is forecast to reach USD 2.65 billion by 2031 at a 5.9% CAGR over 2026-2031.

This report is Segmented by Type (Serial NOR Flash, and More), Interface (Quad SPI, and More), Density (2 Megabit and Less, and More), Voltage (3 V Class, and More), End-User Application (Consumer Electronics, and More), Process Technology Node (45 Nm, 55 Nm, and More), Packaging Type (WLCSP/CSP, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Asia-Pacific NOR Flash Market Trends and Insights

Booming ADAS and Infotainment Memory Demand in China-Japan Automotive Electronics

Automotive systems in China and Japan increasingly rely on redundant NOR arrays for safe-boot and fail-operational functions, pushing average vehicle content from 32 megabits in 2024 to a projected 128 Megabits by 2028. Japanese Tier-1 suppliers embed dual-channel NOR to achieve ISO 26262 ASIL-D compliance. Infineon's SEMPER devices qualified with Renesas R-CAR Gen4 in 2025, evidencing the two-to-three-year design-win horizon common in this market. ADAS alone already represents more than half of automotive NOR revenue in the region. With China delivering 27 million vehicles in 2025 and electrification rising, the segment anchors long-term demand.

Shift To Octal and HyperBus NOR Architectures Across Asia-Pacific Design Houses

Octal and xSPI interfaces delivered only 15-18% of 2025 volumes yet are scaling fast on the back of bandwidth needs above 400 MB/s in edge-AI and automotive gateway controllers. Infineon introduced an LPDDR-compatible NOR in March 2026, doubling read throughput to 800 MB/s and simplifying routing. GigaDevice's 1.2 V Octal parts serve battery-powered IoT nodes, cutting active current by up to 40%. As Taiwanese and Korean design houses migrate edge-AI accelerators to xSPI, suppliers secure multi-year, higher-margin contracts that offset consumer-electronic price pressure.

Export-Control Curbs on EUV and DUV Tools Into Mainland China

Expanded Foreign Direct Product Rule measures implemented in October 2024 bar advanced lithography shipments to Chinese memory fabs, limiting mainland processes to 40-nanometer and older for the foreseeable future. Automotive-grade NOR at 28 nanometers promises 30-40% power savings, so the restriction hampers mainland suppliers seeking vehicle design wins. Japan's alignment with U.S. policy cut access to Tokyo Electron etch systems, reinforcing the technology split: Taiwan and South Korea advance to 22 nanometers while China remains at mature nodes.

Other drivers and restraints analyzed in the detailed report include:

- Chip-Self-Sufficiency Incentives in China and India

- OLED-Centric Smartphone Designs Pushing High-Density Serial NOR

- 12-Inch Foundry Tightness in Taiwan Driving Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial NOR retained 71.8% of the Asia-Pacific NOR Flash market share in 2025, as SPI and Quad SPI interfaces satisfy most consumer and IoT boot-code needs. Parallel NOR, although only 28.2% of revenue, benefits from a 7.3% CAGR driven by deterministic-latency requirements in industrial control and safety-critical automotive modules. Parallel devices remain embedded in airbags and ABS, where sub-50 ns access cannot be compromised.

In response, serial suppliers add hardware root-of-trust and redundancy to challenge parallel incumbents, foreshadowing tighter competition in the next platform refresh. Serial architectures are also creeping upward in density and reliability. Macronix's ArmorBoot MX76 brings 1 Gigabit secure-boot capability, showing that execute-in-place and security, once exclusive to parallel NOR, can migrate to serial designs. Suppliers that fail to offer these enhancements risk confinement to cost-sensitive consumer devices, where price wars with Chinese entrants squeeze margins.

SPI Single/Dual dominated the market with a 47.6% share in 2025. However, its bandwidth ceilings, capped at approximately 80 MB/s, restrict its application in data-intensive systems. Despite this limitation, it remains a preferred choice for cost-sensitive applications where high-speed performance is not critical. Quad SPI, holding around 35% of the market share, is at a pivotal stage, catering to mid-range smartphones and industrial gateways that require faster firmware updates. Meanwhile, Octal and xSPI interfaces, though accounting for less than 20% of total units, are experiencing significant growth. These advanced interfaces are growing at a 9.6% CAGR, driven by increasing demand for automotive Ethernet gateways and edge-AI accelerators that require read performance of up to 800 MB/s.

Interface fragmentation is playing a critical role in shaping supplier roadmaps. Taiwanese design houses are quickly adopting xSPI interfaces and securing multiyear commitments from automotive clients, helping stabilize their revenue streams. Manufacturers of legacy appliances and white goods continue to rely on SPI Single/Dual interfaces. This choice is primarily driven by the need to minimize controller pin counts and ensure cost efficiency. As a result, mature interfaces like SPI Single/Dual maintain a long revenue tail, supported by their relevance in applications where advanced performance is not a priority.

Devices at 64 megabits or below accounted for 27.2% of the Asia-Pacific NOR Flash market in 2025, driven by the widespread use of low-cost microcontrollers across various applications. These devices remain popular due to their affordability and compatibility with legacy systems. However, densities above 256 megabits are growing rapidly, with a CAGR of 10.9%, as OLED smartphones, ADAS controllers, and edge-AI modules increasingly require larger firmware storage. Macronix's 1 Gigabit ArmorBoot technology supports isolated secure partitions for over-the-air updates, encouraging flagship smartphones to adopt half-gigabit NOR footprints. This trend highlights the growing demand for higher-density NOR Flash in advanced applications.

Mid-tier densities, ranging from 128 to 256 megabits, strike a balance between cost and capacity, making them ideal for automotive infotainment systems and industrial human-machine interfaces (HMIs). These densities cater to applications that require moderate storage without significantly increasing costs. 2-8 Megabit parts continue to find use in ultra-low-cost sensors, where minimal storage is sufficient. However, these lower-density parts are gradually losing market share each year to embedded flash solutions integrated within system-on-chips, which offer better performance and efficiency for modern applications.

Complete Report Scope:

- By Type (Value, Volume)

- Serial NOR Flash

- Parallel NOR Flash

- By Interface (Value)

- SPI Single / Dual

- Quad SPI

- Octal and xSPI

- By Density (Value)

- 2 Megabit and Less NOR

- 4 Megabit and Less (greater than 2 MB) NOR

- 8 Megabit and Less (greater than 4 MB) NOR

- 16 Megabit and Less (greater than 8 MB) NOR

- 32 Megabit and Less (greater than 16 MB) NOR

- 64 Megabit and Less (greater than 32 MB) NOR

- 128 Megabit and Less (greater than 64 MB) NOR

- 256 Megabit and Less (greater than 128 MB) NOR

- Greater than 256 Megabit

- By Voltage (Value)

- 3 V Class

- 1.8 V Class

- Wide-Voltage (1.65 V - 3.6 V)

- Others - 1.2 V Class (and similar sub-1.8 V: 2.5 V, 5 V)

- By End-User Application (Value, Volume)

- Consumer Electronics

- Communication

- Automotive

- Industrial

- Other End-User Applications

- By Process Technology Node (Value)

- 90 nm and Older

- 65 nm

- 55 nm (including 58 nm)

- 45 nm

- 28 nm and Below

- By Packaging Type (Value)

- WLCSP / CSP

- QFN / SOIC

- BGA / FBGA

- Other Packaging Types

- By Geography

- China

- Japan

- South Korea

- Taiwan

- India

- Rest of Asia-Pacific

List of Companies Covered in this Report:

- Winbond Electronics Corp.

- GigaDevice Semiconductor Inc.

- Macronix International Co., Ltd.

- Micron Technology Inc.

- Infineon Technologies AG

- Renesas Electronics Corp.

- Microchip Technology Inc.

- Elite Semiconductor Memory Tech (ESMT)

- Puya Semiconductor (Shanghai) Co.

- Wuhan XMC

- Integrated Silicon Solution Inc. (ISSI)

- Samsung Electronics Co. Ltd.

- STMicroelectronics NV

- Alliance Memory, Inc.

- SK hynix Inc.

- AMIC Technology Corp.

- NXP Semiconductors N.V.

- Powerchip Semiconductor Manufacturing Corp.

- Adesto Technologies (renesas)

- BOYA Microelectronics Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming ADAS and Infotainment Memory Demand in China-Japan Automotive Electronics

- 4.2.2 OLED-Centric Smartphone Designs Pushing High-Density Serial NOR in China and Korea

- 4.2.3 Chip-Self-Sufficiency Incentives (China, India PLI) Accelerate Regional NOR Fabs

- 4.2.4 IoT Manufacturing Clusters in ASEAN Requiring Low-Power Code Storage

- 4.2.5 Industry 4.0 Upgrades in Taiwan and South Korea Industrial Automation

- 4.2.6 Shift to Octal/HyperBus NOR Architectures Across Asia-Pacific Design Houses

- 4.3 Market Restraints

- 4.3.1 Low-Cost NAND and ReRAM Cannibalization in Shenzhen Design Wins

- 4.3.2 12-Inch Foundry Tightness in Taiwan Driving Price Volatility

- 4.3.3 Escalating 28 nm and 22 nm NOR R&D Capex vs. Mainstream Logic Lines

- 4.3.4 Export-Control Curbs on EUV / DUV Tools into Mainland China

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing Analysis

- 4.10 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By Type (Value, Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less NOR

- 5.3.2 4 Megabit and Less (greater than 2 MB) NOR

- 5.3.3 8 Megabit and Less (greater than 4 MB) NOR

- 5.3.4 16 Megabit and Less (greater than 8 MB) NOR

- 5.3.5 32 Megabit and Less (greater than 16 MB) NOR

- 5.3.6 64 Megabit and Less (greater than 32 MB) NOR

- 5.3.7 128 Megabit and Less (greater than 64 MB) NOR

- 5.3.8 256 Megabit and Less (greater than 128 MB) NOR

- 5.3.9 Greater than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V - 3.6 V)

- 5.4.4 Others - 1.2 V Class (and similar sub-1.8 V: 2.5 V, 5 V)

- 5.5 By End-User Application (Value, Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Other End-User Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and Older

- 5.6.2 65 nm

- 5.6.3 55 nm (including 58 nm)

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Other Packaging Types

- 5.8 By Geography

- 5.8.1 China

- 5.8.2 Japan

- 5.8.3 South Korea

- 5.8.4 Taiwan

- 5.8.5 India

- 5.8.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Winbond Electronics Corp.

- 6.4.2 GigaDevice Semiconductor Inc.

- 6.4.3 Macronix International Co., Ltd.

- 6.4.4 Micron Technology Inc.

- 6.4.5 Infineon Technologies AG

- 6.4.6 Renesas Electronics Corp.

- 6.4.7 Microchip Technology Inc.

- 6.4.8 Elite Semiconductor Memory Tech (ESMT)

- 6.4.9 Puya Semiconductor (Shanghai) Co.

- 6.4.10 Wuhan XMC

- 6.4.11 Integrated Silicon Solution Inc. (ISSI)

- 6.4.12 Samsung Electronics Co. Ltd.

- 6.4.13 STMicroelectronics NV

- 6.4.14 Alliance Memory, Inc.

- 6.4.15 SK hynix Inc.

- 6.4.16 AMIC Technology Corp.

- 6.4.17 NXP Semiconductors N.V.

- 6.4.18 Powerchip Semiconductor Manufacturing Corp.

- 6.4.19 Adesto Technologies (renesas)

- 6.4.20 BOYA Microelectronics Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Analysis