PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061797

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061797

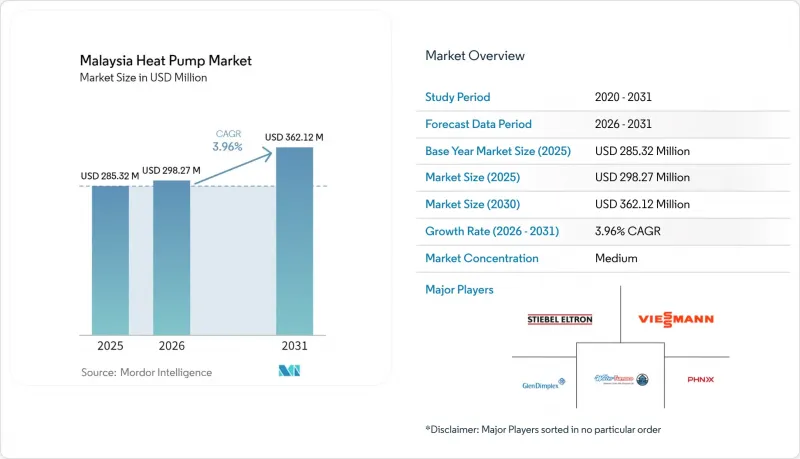

Malaysia Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the malaysia heat pump market size is projected to expand from USD 285.32 million in 2025 and USD 298.27 million in 2026 to USD 362.12 million by 2031, registering a CAGR of 3.96% between 2026 to 2031.

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Industrial and Process Heating, and More), End User (Residential, Commercial, and More), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Malaysia Heat Pump Market Trends and Insights

Surging Adoption of Heat Pump Water Heaters in Tropical Climates

High ambient temperatures above 26 °C enable air-source heat-pump water heaters to deliver coefficients of performance exceeding 4.0, translating into 60-75% electricity savings compared with resistance heaters. Field trials showed Rheem's RHP-5207C at 4.2 COP and Summer A-TEC's R290 model at 4.45 COP, demonstrating a clear efficiency edge for natural-refrigerant units. Hotels and hospitals, which devote 15-20% of operating budgets to hot water, are accelerating retrofits, as evidenced by Carrier Malaysia's five-year agreement with Pelaburan Hartanah Berhad to upgrade 24 buildings nationwide. Residential uptake remains price sensitive, but a USD 15 million federal rebate pool and planned 2026 appliance efficiency standards shorten payback periods to below 4 years, widening the addressable base for landed homes.

Implementation of Green Technology Financing Scheme 3.0

Green Technology Financing Scheme 3.0 offers a 2% interest subsidy and a 60% federal guarantee on loans up to MLR 100 million (USD 24 million), trimming capital costs for large commercial heat-pump projects. Penang extended the concept with a state-level Climate Mitigation Fund in October 2025, unlocking blended finance that improves project internal rates of return by 150-200 basis points. Longer loan tenors of 10-12 years now align amortization schedules with equipment lifecycles, encouraging ground-source and high-capacity installations. The funding framework is accelerating rollout of centralized chiller-heat-pump plants in manufacturing, hospitality, and healthcare complexes, making Malaysia heat pump market adoption less dependent on developer balance-sheet strength.

High Upfront Capital Expenditure for Ground-Source Systems

Ground-source installations cost MLR 150,000-400,000 (USD 36,000-97,000) for a 50 kW system, more than double an equivalent air-source setup. Tropical soils have thermal conductivity around 1.1 W*m-1*°C-1, 30-40% below temperate benchmarks, forcing oversized borehole arrays that inflate costs and extend payback to 10-15 years. Year-round cooling loads raise ground temperatures, eroding long-term efficiency unless hybrid rejection fields are added, which further boosts capital outlay. As a result, only institutional campuses and grant-backed pilot projects currently opt for ground-source designs, limiting this slice of Malaysia heat pump market growth.

Other drivers and restraints analyzed in the detailed report include:

- Rising Electricity Tariffs Driving Shift to High-Efficiency HVAC

- Mandated Phase-Out of R22 Refrigerant in 2027

- Limited Skilled Installers Outside Klang Valley

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air-source units captured 47.83% of Malaysia heat pump market share in 2025, reflecting the segment's lower capital intensity, small physical footprint, and ability to slot into split-system infrastructure in dense urban buildings. Hybrid configurations that marry air-source evaporators with ground- or water-loop heat rejection are projected to grow at a 4.82% CAGR through 2031, driven by industrial operators and hyperscale data-center builders that need to stabilize coefficients of performance during monsoon humidity spikes. The hybrid approach also cuts defrost-cycle energy penalties, extends compressor life, and eases grid-demand peaks, a trio of benefits that resonates with owners now facing time-of-use tariffs.

System integrators increasingly bundle modular chillers, liquid coolers, and supervisory controls so facility managers can toggle between air and ground loops in real time. Data-center designers in Johor specify dual-path cooling trains so that maintenance on outdoor coils never jeopardizes rack uptime. Industrial estates in Penang replicate the template by tapping shared bore-fields to trim plant steam bills while retaining air-source redundancy for shutdown periods. As grid regulators publish stricter seasonal-efficiency indices, the hybrid cohort is expected to chip away at the dominant air-source position, broadening Malaysia heat pump market penetration across process-critical facilities.

Air-to-air technology accounted for 40.31% of Malaysia heat pump market size in 2025 because residential and light-commercial buyers prize easy installation and ductless flexibility. Ground-to-water systems are forecast to advance at a 4.39% CAGR to 2031 as manufacturers retrofit closed-loop heat exchangers that pre-heat boiler feedwater or supply low-grade process heat. Natural-refrigerant units using R290 or R32 help industrial users hedge against the 2027 R22 ban while unlocking Scope-1 emission cuts.

Industrial parks now rough-in bore-fields during site grading, spreading drilling costs across multiple tenants and shortening project payback windows. Early adopters in palm-oil refining use ground-to-water modules to lift condensate from 50 °C to 80 °C, trimming natural-gas use without re-engineering existing steam headers. Hotel chains, meanwhile, lean on air-to-water packages to meet hot-water loads at COPs above 4.0, replacing electric resistance heaters that once soaked up 15-20% of operating budgets. As local production of compressors and plate heat exchangers expands, technology choice will hinge less on import lead times and more on plant-specific thermal profiles, cementing ground-to-water as a mainstream option.

List of Companies Covered in this Report:

- Stiebel Eltron GmbH & Co. KG

- Vaillant Group

- Viessmann Climate Solutions SE

- NIBE Industrier AB (NIBE Climate Solutions)

- Glen Dimplex Group

- Daikin Industries Ltd. (Heat Pump Division)

- Panasonic Corporation (Heating and Ventilation A/C Malaysia Sdn Bhd)

- Mitsubishi Electric Corporation (Malaysia Branch)

- PHNIX Eco-Energy Solution Ltd.

- Midea Group Co., Ltd. (Malaysia)

- Carrier Global Corporation

- LG Electronics Inc.

- Sanden Holdings Corp. (Heat Pump Div.)

- WaterFurnace International Inc.

- Aermec S.p.A.

- Clivet SpA

- Alpha Innotec GmbH

- Ochsner Warmepumpen GmbH

- Heliotherm Warmepumpentechnik GmbH

- MasterTherm CZ s.r.o.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption of Heat Pump Water Heaters in Tropical Climates

- 4.2.2 Implementation of the Green Technology Financing Scheme 3.0

- 4.2.3 Rising Electricity Tariffs Driving Shift to High-Efficiency HVAC

- 4.2.4 Mandated Phase-Out of R22 Refrigerant in 2027

- 4.2.5 Growing Demand from Data Centers for Precision Cooling

- 4.2.6 Increase in Net-Zero Building Certifications

- 4.3 Market Restraints

- 4.3.1 High Upfront Capital Expenditure for Ground-Source Systems

- 4.3.2 Limited Skilled Installers Outside Klang Valley

- 4.3.3 Intermittent Policy Enforcement Reducing Investor Confidence

- 4.3.4 Low Awareness Among Residential Consumers of Lifecycle Savings

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Stiebel Eltron GmbH & Co. KG

- 6.4.2 Vaillant Group

- 6.4.3 Viessmann Climate Solutions SE

- 6.4.4 NIBE Industrier AB (NIBE Climate Solutions)

- 6.4.5 Glen Dimplex Group

- 6.4.6 Daikin Industries Ltd. (Heat Pump Division)

- 6.4.7 Panasonic Corporation (Heating and Ventilation A/C Malaysia Sdn Bhd)

- 6.4.8 Mitsubishi Electric Corporation (Malaysia Branch)

- 6.4.9 PHNIX Eco-Energy Solution Ltd.

- 6.4.10 Midea Group Co., Ltd. (Malaysia)

- 6.4.11 Carrier Global Corporation

- 6.4.12 LG Electronics Inc.

- 6.4.13 Sanden Holdings Corp. (Heat Pump Div.)

- 6.4.14 WaterFurnace International Inc.

- 6.4.15 Aermec S.p.A.

- 6.4.16 Clivet SpA

- 6.4.17 Alpha Innotec GmbH

- 6.4.18 Ochsner Warmepumpen GmbH

- 6.4.19 Heliotherm Warmepumpentechnik GmbH

- 6.4.20 MasterTherm CZ s.r.o.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment