PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061798

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061798

Philippines Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

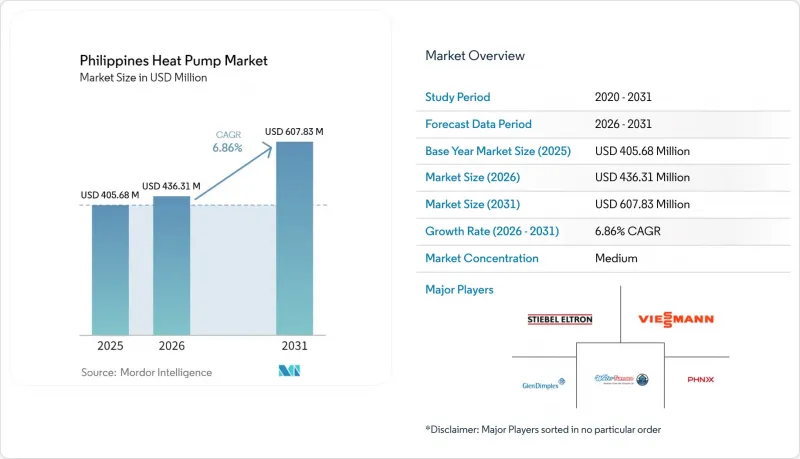

According to Mordor Intelligence, the philippines heat pump market size is projected to expand from USD 405.68 million in 2025 and USD 436.31 million in 2026 to USD 607.83 million by 2031, registering a CAGR of 6.86% between 2026 to 2031.

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Industrial and Process Heating, and More), End User (Residential, Commercial, and More), Installation (New Installation, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Philippines Heat Pump Market Trends and Insights

Growing Use of Heat Pumps Beyond Traditional Heating, Ventilation, and Air Conditioning Applications

Large cold-chain facilities are specifying industrial-scale heat pumps to maintain temperatures that range from -25 °C for ice cream to 13 °C for banana ripening, underpinning diversification away from comfort cooling. The 11,728-pallet Mindanao warehouse commissioned in March 2026 integrates renewable power through the Green Energy Option Program, proving out the technology in energy-intensive logistics operations. Hospitality properties such as Park Inn Clark realized 240,000 kWh in annual savings after adopting centralized systems, which validates the operating-expense upside for hotels. Developers of turnkey factory shells inside special economic zones now embed heat pumps as standard utility infrastructure to lure export manufacturers. This widening usage spectrum positions the Philippines heat pump market as a cross-sector solution rather than a single-application product line.

Implementation of Government Incentives for Renewable Heating

The memorandum of understanding on Sustainable Green Industrial Parks grants tax holidays and duty exemptions when factories install energy-efficient equipment, immediately tilting capital-spending decisions toward heat pumps. The Department of Energy consultation on stricter minimum energy performance standards, started in 2025, signals that residential and commercial water heaters will soon face mandatory efficiency floors. Although direct consumer rebates are absent, the Green Energy Option Program lowers the delivered cost of power for high-load users, narrowing the price gap with liquefied petroleum gas heaters. The Philippine Green Building Council is lobbying for a revised National Building Code that will require centralized heat pump water heaters in mid-rise projects above 10 floors, effectively mandating the technology for most future condominiums. Taken together, the policy stack offers predictable demand visibility that benefits both local distributors and multinational manufacturers in the Philippines heat pump market.

High Up-Front Installation Cost and Limited Financing

Residential heat pump water heaters range from PHP 55,000 (USD 0.98 million per 1,000 units) to PHP 232,500 (USD 4.13 million per 1,000 units), equal to three to twelve months of median household income and thus out of reach for most families without credit support. Stiebel Eltron units sell at 30-40% above local brands, confining them to upper-income buyers. Banks rarely issue green-technology loans to homeowners, so cash purchases dominate, slowing velocity in the Philippines heat pump market. Commercial and industrial buyers offset costs through tax breaks, widening the affordability gap between segments. Until concessional lending or rebate schemes emerge, residential adoption will underperform the headline market growth.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Urbanization and Mid-Rise Residential Boom

- Nationwide Phase-Out of High Global Warming Potential Refrigerants

- Shortage of Certified Heat Pump Technicians

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid systems captured a marginal share in 2025 but are forecast to grow at 7.61% annually through 2031, outperforming the Philippines heat pump market by 75 basis points as island resorts and agro-industrial parks seek resilience against tariffs of PHP 16-25 (USD 0.29-0.45) per kWh. Air source platforms provide 47.36% of 2025 demand by leveraging lower first cost and compatibility with Metro Manila electrical infrastructure. Water source solutions serve coastal resorts where inlet temperatures stabilize efficiency above a 4.0 coefficient of performance, though permitting hurdles lengthen project cycles. Ground source adoption concentrates in institutional flagship projects like the December 2025 900 kW geothermal tie-in at Capitol University Medical Center.

Manufacturers now roll out modular lines that toggle between air-source and solar-thermal modes based on spot-market power pricing, optimizing lifetime energy spend. LG's Multi V Water 5 unit, demonstrated in Cebu, features a wide 20-150 Hz inverter range, widening partial-load efficiency. Air source heat pumps dominate the residential slice of the Philippines heat pump market size equation but face diminishing returns during peak-temperature months. Hybrid and water-based systems fill that performance gap, although higher engineering complexity restricts uptake to projects with sound technical oversight.

Air-to-water units held 40.14% of the Philippines heat pump market share in 2025, mainly due to condominium developers favoring centralized domestic hot water risers. Ground-to-water technology will advance by 7.38% a year, tapping Luzon's geothermal belt where First Gen operates 1,870 MW of capacity. Air-to-air models play in the residential split-type upgrade cycle, commanding 15-20% price premiums in cooler upland cities. Water-to-water remains confined to industrial process loops requiring tight temperature control.

Daikin's MARUTTO platform integrates variable refrigerant flow, water heating and building management to recycle data-center waste heat into adjacent residences. Installation cost for bore-hole loops ranges from PHP 8,000-12,000 (USD 143-214) per kW and elongates project timelines, but 20-25% higher seasonal efficiency offsets capex in 15-year asset plans. Air-to-water designs therefore dominate new builds, while ground-to-water wins in owner-occupied facilities committing to long-range operating savings.

List of Companies Covered in this Report:

- Mitsubishi Electric Corp.

- Daikin Industries Ltd.

- Panasonic Holdings Corp.

- LG Electronics Inc.

- Samsung Electronics Co. Ltd.

- Stiebel Eltron GmbH & Co. KG

- Vaillant Group

- Viessmann Climate Solutions SE

- NIBE Industrier AB

- Glen Dimplex Group

- PHNIX Eco-Energy Solution Ltd.

- Haier Group

- Enertech Global LLC

- Ecoforest Geotermia S.L.

- Alpha Innotec GmbH

- TCL Corporation

- Grundfos Holding A/S

- MasterTherm CZ s.r.o.

- Clade Engineering Systems Ltd.

- Calorex Heat Pumps Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Use of Heat Pumps Beyond Traditional HVAC Applications

- 4.2.2 Implementation of Government Incentives for Renewable Heating

- 4.2.3 Rapid Urbanization and Mid-Rise Residential Boom

- 4.2.4 Nationwide Phase-Out of High-GWP Refrigerants

- 4.2.5 Electrification of Industrial Process Heating in SEZs

- 4.2.6 Surge in Off-Grid Tourism Resorts Adopting Heat Pump Systems

- 4.3 Market Restraints

- 4.3.1 High Up-Front Installation Cost and Limited Financing

- 4.3.2 Shortage of Certified Heat-Pump Technicians

- 4.3.3 Grid Instability in Rural Islands

- 4.3.4 Fragmented After-Sales Service Ecosystem

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Mitsubishi Electric Corp.

- 6.4.2 Daikin Industries Ltd.

- 6.4.3 Panasonic Holdings Corp.

- 6.4.4 LG Electronics Inc.

- 6.4.5 Samsung Electronics Co. Ltd.

- 6.4.6 Stiebel Eltron GmbH & Co. KG

- 6.4.7 Vaillant Group

- 6.4.8 Viessmann Climate Solutions SE

- 6.4.9 NIBE Industrier AB

- 6.4.10 Glen Dimplex Group

- 6.4.11 PHNIX Eco-Energy Solution Ltd.

- 6.4.12 Haier Group

- 6.4.13 Enertech Global LLC

- 6.4.14 Ecoforest Geotermia S.L.

- 6.4.15 Alpha Innotec GmbH

- 6.4.16 TCL Corporation

- 6.4.17 Grundfos Holding A/S

- 6.4.18 MasterTherm CZ s.r.o.

- 6.4.19 Clade Engineering Systems Ltd.

- 6.4.20 Calorex Heat Pumps Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment