PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063343

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063343

Asia-Pacific Third-Party Logistics (3PL) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

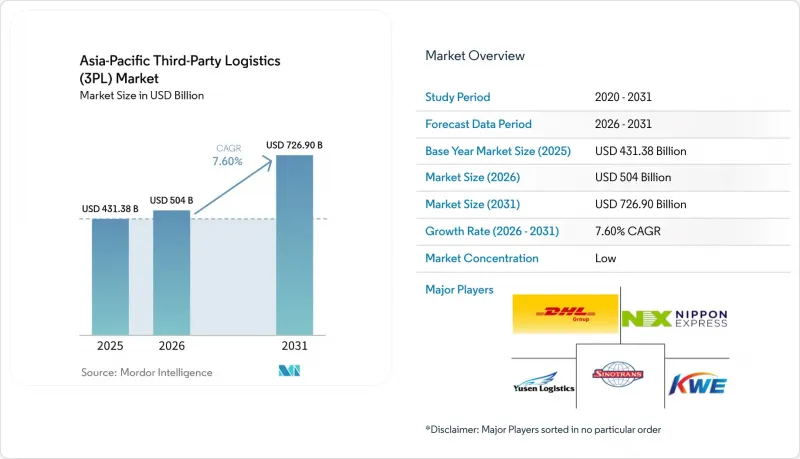

According to Mordor Intelligence, the asia-Pacific third-Party logistics market size is projected to expand from USD 431.38 billion in 2025 and USD 504 billion in 2026 to USD 726.90 billion by 2031, registering a CAGR of 7.60% between 2026 to 2031.

This report is Segmented by Service (Domestic Transportation Management, International Transportation Management, Value-Added Warehousing and Distribution), End-User Industry (Automotive, Energy and Utilities, Manufacturing, and More), Logistics Model (Asset-Light, Asset-Heavy, Hybrid), and Geography (China, India, Japan, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Third-Party Logistics (3PL) Market Trends and Insights

E-commerce boom fuelling same-day and last-mile fulfilment

Rising online order density is shifting 3PL activity from bulk movements to high-frequency fulfillment that relies on automated nodes. JD Logistics reported operating more than 20 automated LangzuTech warehouses across nearly 20 cities by late 2025, which signals how large shippers are leaning on advanced facilities to support delivery speed and order accuracy as volumes increase. The Asia-Pacific third-party logistics market uses such assets to absorb seasonal spikes that would overwhelm traditional networks. Automated sorting and goods-to-person systems compress cycle times for small parcels, which improves customer experience and expands the serviceable market for time-sensitive categories. The Asia-Pacific third-party logistics market is also shaped by platform-backed investments that raise the floor for fulfillment standards across major urban hubs. Providers that align automation with dense last-mile routing are better placed to hold margins as price transparency increases.

Regional Trade Agreement Implementation

RCEP continues to lower friction across a trade zone spanning 15 economies, which encourages shippers to consolidate cross-border logistics under fewer partners. China's recorded goods trade with RCEP members reached RMB 9.63 trillion by Q3 2024, with year-over-year growth, and the China-Laos Railway has moved 11.58 million tons of cross-border cargo since late 2021, which underpins new multimodal solutions that 3PLs can package across borders. The Asia-Pacific third-party logistics market is already building combined road-rail-air offerings around these corridors. Document flow standardization through initiatives like the ASEAN Single Window has reduced paperwork time for participating members, which supports end-to-end visibility and more reliable transit planning. The Asia-Pacific third-party logistics market sees stronger appeal for cross-border trucking and rail alternatives when tariffs and procedures align. Providers with customs brokerage depth and origin-destination compliance teams gain an edge as tariff schedules phase down and certificates of origin integrate into digital workflows.

Infrastructure Gaps in Emerging Markets

Transport networks in several economies remain road-heavy and underdeveloped relative to OECD benchmarks, which limits route flexibility and raises cost-to-serve for long inland moves. Asian Transport Observatory data shows regional infrastructure density and road-to-rail mix lagging developed norms, which constrains modal shift options during disruptions. In Thailand, agricultural freight remains predominantly road-based with minor rail share, which pushes costs above global medians and compresses margins for bulk and FMCG shippers. The Asia-Pacific third-party logistics market can route around bottlenecks with selective use of rail and coastal feeder services where they exist, but dense corridors still face peak congestion. Climate risk adds exposure for roads and rail assets across the region with high precipitation volatility and typhoon frequency, which increases downtime and recovery costs for operators. The Asia-Pacific third-party logistics market will likely bifurcate strategies between premium corridors with planned upgrades and secondary routes where road dependence persists, which affects achievable service levels.

Other drivers and restraints analyzed in the detailed report include:

- Digital Logistics Platform Proliferation

- Cold Chain Infrastructure Development

- Geopolitical Tensions and Trade Uncertainties

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Domestic Transportation Management accounted for 46.12% in 2025, which reflected the scale of intra-regional trade and the reliance on trucking for the first and last mile across dense city clusters. That share underlined how route tendering and dynamic capacity brokerage are core capabilities as the Asia-Pacific third-party logistics market diversifies load profiles across short-haul and regional lanes. Value-Added Warehousing and Distribution is the fastest-growing service at a 7.84% CAGR in the period to 2031 as shippers shift inventory closer to consumption and expand cold-ready storage for pharmaceuticals and premium foods. The Asia-Pacific third-party logistics market integrates near-customer storage with micro-fulfillment and controlled-temperature handling to raise throughput and preserve product integrity. Providers that offer calibrated environments and validated processes can sustain higher yields relative to ambient storage. Select integrators are pairing VAWD sites with contract logistics for managed replenishment and vendor-managed inventory to stabilize turns and improve working capital. The Asia-Pacific third-party logistics market is also using automated storage and retrieval, high-bay racking, and robot-assisted picking to manage multi-SKU complexity without expanding footprints.

International Transport Management is diversifying across ocean, air, and rail-led intermodal as cost and reliability cycles shift. Red Sea disruptions pushed carriers and shippers to extend routings, which increased cycle times and raised premiums for time-definite freight, a trend 3PLs addressed with refined air allocation and temperature-controlled buffers for sensitive products. On select corridors, rail segments are now linked more seamlessly to trucking and air uplift to meet delivery windows that the ocean could not meet during volatility, which strengthens the role of corridor-specialist 3PLs that orchestrate multimodal schedules. CEVA highlights the role of engineered transport and customs digitization in reducing dwell time and increasing speed to market on cross-border routes, which expands the use cases for intermodal even as ocean schedules normalize. The Asia-Pacific third-party logistics market increasingly prices services on outcomes that blend mode choice, risk buffers, and compliance rather than on single-lane tariffs alone. Domestic and international services are converging around unified control towers that reconcile bookings, visibility, and exceptions across modes and zones.

In this service mix, Domestic Transportation Management accounted for 46.12% of the Asia-Pacific third-party logistics market share in 2025. Value-Added Warehousing and Distribution within the Asia-Pacific third-party logistics market size is projected to grow at 7.84% through 2031 as multi-temperature capacity scales for time-critical loads.

List of Companies Covered in this Report:

- DHL Supply Chain and Global Forwarding

- Sinotrans Ltd.

- Kintetsu World Express

- Nippon Express Holdings

- Yusen Logistics (NYK)

- Kuehne + Nagel International AG

- DSV A/S

- CEVA Logistics (CMA CGM)

- GEODIS

- Kerry Logistics Network

- LOGISTEED

- Toll Group

- JD Logistics

- AWOT Global Logistics Group

- CIMC Wetrans Logistics Technology

- Mainfreight

- Linfox

- CJ Logistics

- Hellmann Worldwide Logistics

- Savino Del Bene

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce Boom Across Region

- 4.2.2 Regional Trade Agreement Implementation

- 4.2.3 Cold Chain Infrastructure Development

- 4.2.4 Digital Logistics Platform Proliferation

- 4.2.5 Automotive and Electronics Manufacturing Growth

- 4.2.6 Outsourcing Trend by SMEs

- 4.3 Market Restraints

- 4.3.1 Infrastructure Gaps in Emerging Markets

- 4.3.2 Fragmented Regulatory Environment

- 4.3.3 Shortage of Skilled Workforce

- 4.3.4 Geopolitical Tensions and Trade Uncertainties

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Insights into E-commerce Business

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

- 4.9 Impact of Geopolitical Events on the Market

5 Market Size and Growth Forecasts (Value USD)

- 5.1 By Service

- 5.1.1 Domestic Transportation Management

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Others

- 5.1.2 International Transportation Management

- 5.1.2.1 Road

- 5.1.2.2 Air

- 5.1.2.3 Sea

- 5.1.2.4 Multimodal / Intermodal

- 5.1.3 Value-Added Warehousing and Distribution (VAWD)

- 5.1.1 Domestic Transportation Management

- 5.2 By End-User Industry

- 5.2.1 Automotive

- 5.2.2 Energy and Utilities

- 5.2.3 Manufacturing

- 5.2.4 Life Sciences and Healthcare

- 5.2.5 Technology and Electronics

- 5.2.6 Retail and E-commerce

- 5.2.7 Consumer Goods and FMCG

- 5.2.8 Food and Beverages

- 5.2.9 Others

- 5.3 By Logistics Model

- 5.3.1 Asset-Light (Management-Based)

- 5.3.2 Asset-Heavy (Own Fleet and Warehouses)

- 5.3.3 Hybrid

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Singapore

- 5.4.6 Vietnam

- 5.4.7 Indonesia

- 5.4.8 Australia

- 5.4.9 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Supply Chain and Global Forwarding

- 6.4.2 Sinotrans Ltd.

- 6.4.3 Kintetsu World Express

- 6.4.4 Nippon Express Holdings

- 6.4.5 Yusen Logistics (NYK)

- 6.4.6 Kuehne + Nagel International AG

- 6.4.7 DSV A/S

- 6.4.8 CEVA Logistics (CMA CGM)

- 6.4.9 GEODIS

- 6.4.10 Kerry Logistics Network

- 6.4.11 LOGISTEED

- 6.4.12 Toll Group

- 6.4.13 JD Logistics

- 6.4.14 AWOT Global Logistics Group

- 6.4.15 CIMC Wetrans Logistics Technology

- 6.4.16 Mainfreight

- 6.4.17 Linfox

- 6.4.18 CJ Logistics

- 6.4.19 Hellmann Worldwide Logistics

- 6.4.20 Savino Del Bene

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment