PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063710

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063710

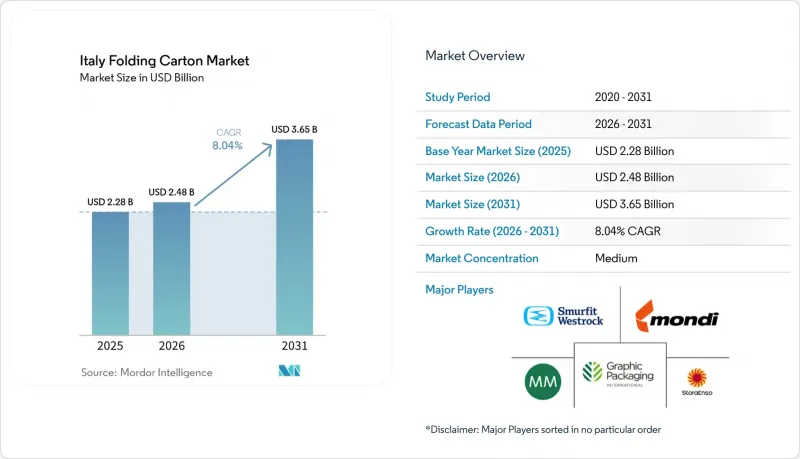

Italy Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the italy folding carton market size is expected to increase from USD 2.28 billion in 2025 to USD 2.48 billion in 2026 and reach USD 3.65 billion by 2031, growing at a CAGR of 8.04% over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, and More), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Italy Folding Carton Market Trends and Insights

Increasing Preference for Recyclable Packaging

Extended Producer Responsibility fees imposed by CONAI penalize non-recyclable structures, so brand owners are rapidly substituting laminated plastics with mono-material cartons that qualify for lower tariffs. Consumer polling shows that 77% of Italians factor packaging sustainability into their purchase decisions, prompting retailers to favor SKUs with clear disposal labels. Fedrigoni's 2025 investment in Papkot demonstrates how converters are commercializing PFAS-free coatings that pass recyclability guidelines while retaining grease resistance. The national recovery plan earmarks EUR 1.5 billion (USD 1.70 billion) for reuse centers and digital traceability, which will raise post-consumer fiber availability once projects come online. These factors are expected to underpin above-trend substrate demand through at least 2031.

Growth of Premium-Positioned FMCG Products

Premium food, beverage, and cosmetics lines increasingly specify solid bleached sulfate or metalized boards that tolerate hot-foil stamping, embossing, and soft-touch varnishes. Ready-to-eat meal kits valued at EUR 2.5 billion (USD 2.83 billion) require grease-resistant, microwave-safe cartons that command double-digit price premiums over commodity grades. Retail private-label penetration reached 32% in 2024, yet supermarkets differentiate premium tiers through upgraded pack aesthetics. Converters that add inline spectrophotometers and automated inspection, such as Bobst QualiTronic systems, achieve the tighter color tolerances demanded by luxury brands. As discretionary spending recovers, volumes in high-decor segments are expected to outpace the overall Italy folding carton market.

Volatility in Virgin Fiber Pulp Prices

Kraftliner rose more than 20% in 2024, while northern bleached softwood pulp climbed 17.6%, compressing converter margins because pass-through clauses lag spot prices by up to 90 days. Recycled-content mandates intensify competition for recovered paper, which averaged EUR 120-150 (USD 136-170) per tonne in Northern Italy during 2025. Southern regions' lower collection rates force mills to truck bales north-to-south, adding logistics premiums. Vertically integrated groups like RDM and Burgo hedge volatility through captive pulp and deinking capacity, but most SMEs remain price takers, dampening investment appetite.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce Boom and Small-Batch Custom Runs

- Brand Owner Migration from Plastics to Paperboard

- Capital-Intensive Nature of High-End Digital Presses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding boxboard accounted for 38.56% of the Italian folding carton market size in 2025, favored for balanced stiffness, printability, and cost in mainstream food applications. Solid bleached sulfate is forecast to post a 9.21% CAGR as cosmetics and pharma brands demand high-brightness surfaces compatible with hot-foil, emboss, and barrier coatings. White line chipboard, produced from recycled fibers, is gaining traction in electronics and household goods where surface aesthetics are secondary. RDM's Vincicoat PLUS, launched in 2026, incorporates 85% recycled fibers yet delivers 15-20% greater strength, illustrating the innovation trajectory toward lightweight, circular substrates.

Producers recasting mills for higher recycled-content output are pre-positioning for the PPWR's 30% post-consumer target, a shift expected to realign procurement toward mills offering validated closed-loop fibers. Competitive emphasis is moving to coatings that preserve recyclability, with Papkot's nanostructured liner replacing PFAS while maintaining grease resistance. Substrates with non-cellulosic layers below 5% qualify for CONAI's lowest fee bracket, nudging buyers toward dispersion-coated or bio-based alternatives. As brand owners publish carbon footprints, mills offering cradle-to-gate emissions data gain sourcing preference, reinforcing a virtuous cycle that favors high-recycled-content grades within the Italy folding carton market.

List of Companies Covered in this Report:

- Smurfit WestRock plc

- Mayr-Melnhof Karton AG

- Graphic Packaging International LLC

- International Paper Company

- RDM Group

- GPack Group

- Lucaprint Group

- Box Marche SpA

- Pozzoli SpA

- Burgo Group S.p.A.

- Metsa Board Corporation

- Schur Pack Italy Srl

- Stora Enso Oyj

- Fedrigoni Group

- Seda International Packaging Group SpA

- Artigrafiche Reggiane & Lai SpA

- Italpack Cartons Srl

- Mondi plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Preference for Recyclable Packaging

- 4.2.2 Growth of Premium-Positioned FMCG Products

- 4.2.3 E-commerce Boom and Small-Batch Custom Runs

- 4.2.4 Brand Owner Migration From Plastics to Paperboard

- 4.2.5 Expansion of Italy's Ready-to-Eat Meal Segment

- 4.2.6 Retailer Demand for Shelf-Ready Multipacks

- 4.3 Market Restraints

- 4.3.1 Volatility in Virgin Fiber Pulp Prices

- 4.3.2 Capital-Intensive Nature of High-End Digital Presses

- 4.3.3 Limited Folding Carton Recycling Infrastructure in Southern Italy

- 4.3.4 Stringent Food-Contact Compliance Costs for SMEs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit WestRock plc

- 6.4.2 Mayr-Melnhof Karton AG

- 6.4.3 Graphic Packaging International LLC

- 6.4.4 International Paper Company

- 6.4.5 RDM Group

- 6.4.6 GPack Group

- 6.4.7 Lucaprint Group

- 6.4.8 Box Marche SpA

- 6.4.9 Pozzoli SpA

- 6.4.10 Burgo Group S.p.A.

- 6.4.11 Metsa Board Corporation

- 6.4.12 Schur Pack Italy Srl

- 6.4.13 Stora Enso Oyj

- 6.4.14 Fedrigoni Group

- 6.4.15 Seda International Packaging Group SpA

- 6.4.16 Artigrafiche Reggiane & Lai SpA

- 6.4.17 Italpack Cartons Srl

- 6.4.18 Mondi plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment