PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063712

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063712

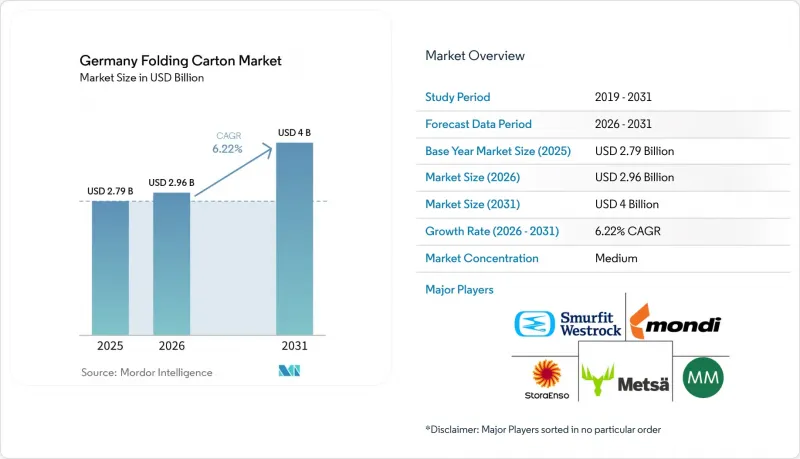

Germany Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the germany folding carton market size is expected to increase from USD 2.79 billion in 2025 to USD 2.96 billion in 2026 and reach USD 4.00 billion by 2031, growing at a CAGR of 6.22% over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, Digital, Gravure, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Folding Carton Market Trends and Insights

Growing Demand For Sustainable Packaging In Food And Beverage

Food and beverage producers are accelerating the switch from multilayer films to fiber-based carton to satisfy retailer sustainability scorecards and consumer expectations for readily recyclable packaging. Verified lifecycle-assessment data shows an 8% drop in fossil CO2 equivalent per tonne of carton between 2021 and 2024, reinforcing procurement decisions that link packaging to Scope 3 decarbonization commitments. German dairies and bakery brands highlight these gains in annual ESG reports, translating carton adoption into marketable climate credentials. The sector's 87% European recycling rate already surpasses the VerpackG target and is moving toward 90%, giving carton an end-of-life infrastructure advantage over flexible plastics. Converters capable of issuing third-party-audited chain-of-custody documents now win volume even in cost-sensitive private-label channels because retailers view transparent data as insurance against future greenwashing fines.

Government Regulations Encouraging Recyclable Materials

Extended producer-responsibility fees under the German Packaging Act rise sharply for formats deemed hard to recycle, tilting total system costs in favor of mono-material folding carton. The August 2026 EU ban on PFAS in food-contact packaging removes a critical barrier performance edge that fluoropolymer-coated films held, compelling converters to adopt water-based or bio-polymer coatings that preserve oil resistance without fluorinated chemistry. Early movers who partnered with chemical suppliers for PFAS-free solutions now control approved capacity and command premium pricing. On top of national rules, the EU Packaging and Packaging Waste Regulation will require every package on the market to be recyclable by 2030, effectively sidelining most multilayer flexible structures unless chemical recycling scales up. German converters' early compliance secures long-term contracts from multinational quick-service restaurants aiming to avoid costly mid-decade package transitions.

Volatility In Recycled Fiber Prices

Recovered-paper prices spiked by EUR 20-30 (USD 22-33) per tonne in April 2025 when export demand collided with a domestic collection dip, cutting converters' margins on recycled-content grades. Because folding boxboard and white-line chipboard carry contract ceilings on price pass-through, mid-tier converters absorbed temporary losses, which curbed discretionary capital spending. Spot-market swings also destabilized forecast accuracy for supply-chain planners, leading brand owners to hedge their exposure by splitting volumes between virgin and recycled substrates. Larger integrated groups blunted volatility through captive pulp lines, but independent German converters faced procurement risk that complicated long-term capacity planning. Continuing fiber price sensitivity remains the most unpredictable constraint on the German folding carton market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of E-Commerce Sector

- Advancements In Digital Printing Customization

- Competition From Flexible Plastic Packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Coated Unbleached Kraft's share acceleration reflects quick-service restaurants and industrial suppliers embracing natural-brown fibers as visual shorthand for sustainability. The format's 7.18% forecast CAGR positions it as the growth engine of the German folding carton market size for materials. Lightweighting advances from suppliers such as Stora Enso push grammage into the 205-310 g/m2 range, translating into logistics savings without sacrificing stiffness. In contrast, Solid Bleached Sulfate holds premium ground in luxury chocolate and fragrance gift sets, but its uptick slows as brand owners reconcile glossy whiteness with decarbonization pledges. White Line Chipboard, though price-competitive, faces margin pressure when recovered-paper indices surge, underscoring the volatility restraint already noted. Folding Boxboard remains the anchor at 34.91% market share, straddling printability and cost but facing incremental loss to kraft, where natural-look trays meet functional needs. The German folding carton market share for specialty metalized boards remains niche, serving frozen entrees and household blade cartridges that demand dual-side barrier yet accept higher unit prices.

Second-generation coating lines now integrate water-based oil- and grease-resistance directly into kraft substrates, eliminating an extra laminating pass and shortening cycle time. Mayr-Melnhof's lifecycle audit quantifies 16-30% carbon savings compared with average European production, arming converters with data for brand-owner RFP scoring. As carbon accounting tightens, the German folding carton market gravitates toward grades that offer verified cradle-to-gate transparency and end-of-life recyclability.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- Mondi plc

- Mayr-Melnhof Karton AG

- Stora Enso Oyj

- Metsa Board Corporation

- Graphic Packaging Holding Company

- Klingele Paper & Packaging Group

- Edelmann Group

- Thimm Group

- Schumacher Packaging GmbH

- Faller Packaging GmbH

- Model AG

- Rondo Ganahl AG

- All4Labels Group GmbH

- Christiansen Print GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Sustainable Packaging in Food and Beverage

- 4.2.2 Government Regulations Encouraging Recyclable Materials

- 4.2.3 Expansion of E-commerce Sector

- 4.2.4 Advancements in Digital Printing Customization

- 4.2.5 Rising Brand Owner Focus on Premiumization

- 4.2.6 Shift Toward Lightweighting for Logistics Efficiency

- 4.3 Market Restraints

- 4.3.1 Volatility in Recycled Fiber Prices

- 4.3.2 Competition from Flexible Plastic Packaging

- 4.3.3 High Capital Expenditure for Advanced Printing Presses

- 4.3.4 Supply-Chain Disruptions for Specialty Coatings

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Mondi plc

- 6.4.3 Mayr-Melnhof Karton AG

- 6.4.4 Stora Enso Oyj

- 6.4.5 Metsa Board Corporation

- 6.4.6 Graphic Packaging Holding Company

- 6.4.7 Klingele Paper & Packaging Group

- 6.4.8 Edelmann Group

- 6.4.9 Thimm Group

- 6.4.10 Schumacher Packaging GmbH

- 6.4.11 Faller Packaging GmbH

- 6.4.12 Model AG

- 6.4.13 Rondo Ganahl AG

- 6.4.14 All4Labels Group GmbH

- 6.4.15 Christiansen Print GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment