PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063713

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063713

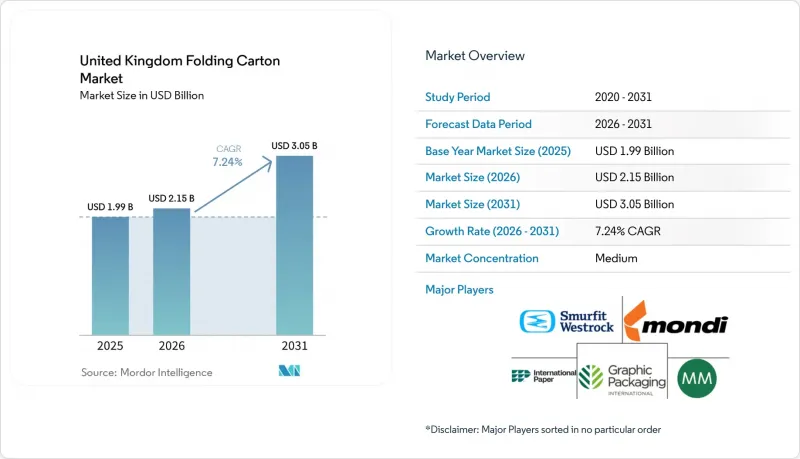

United Kingdom Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the united kingdom folding carton market size was valued at USD 1.99 billion in 2025 and is estimated to grow from USD 2.15 billion in 2026 to reach USD 3.05 billion by 2031, at a CAGR of 7.24% during the forecast period (2026-2031).

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, Digital, Gravure, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More). The Market Forecasts are Provided in Terms of Value (USD).

United Kingdom Folding Carton Market Trends and Insights

Accelerated Phase-Out of Single-Use Plastics Under the UK Plastic Packaging Tax

The April 2026 tax hike to GBP 228.82 (USD 291) per tonne on packaging containing less than 30% recycled plastic has raised immediate compliance costs for hybrid carton with plastic windows or barrier films, prompting brand owners to redesign packs in favor of mono-material board solutions. From April 2027, a mass-balance allowance for chemically recycled plastic will provide relief, but the additional auditing burden is likely to keep the momentum of fiber substitution intact. Categories such as frozen vegetables and confectionery have begun migrating from plastic pouches to dispersion-coated carton that meet moisture and grease barriers without compromising recycling yields. HM Revenue and Customs expects the policy mix to lift recycled plastic use in UK packaging by roughly 40%, saving nearly 200,000 t of CO2 annually. Converters that can certify near-zero plastic inputs are therefore winning incremental shelf space in supermarkets and on direct-to-consumer platforms.

E-Commerce Growth Fueling Demand for Lightweight Letterbox-Friendly Carton

Secondary packaging volumes for European e-commerce are projected to climb 45% between 2023 and 2030, outpacing overall packaging demand by a factor of four. Letterbox-compatible formats under 25 mm in height reduce delivery failures and curb logistics emissions, but still need to balance cushioning with material minimization. Right-sizing automation and dynamic pack-dimensioning have become standard investments at UK fulfillment centers, enabling converters to deliver custom carton blanks in 24 hours. Upcoming EU rules capping empty space to 50% for grouped and e-commerce packs add cross-border urgency for UK sellers, reinforcing the adoption of lightweight folding cartonboard that delivers both structural integrity and recyclability.

Volatility in Virgin Pulp Prices Squeezing Converter Margins

Cartonboard prices stayed under downward pressure through early 2026, even as energy and transport costs climbed, reflecting soft demand and discount imports from Asia. Graphic Packaging's FY 2025 results showed EBITDA margins slipping to 16.2% on weaker pricing and deliberate production curtailments. Unless converters secure long-term pulp contracts or integrate backward, margin squeeze risks delaying capex on digital presses and barrier-coating lines.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Digital Printing for Short Runs and SKU Proliferation

- Brand Premiumization Raising Demand for High-Quality Graphic Carton

- Investments in Recyclable Barrier Coatings Enabling Carton Replacement of Plastic Laminates

- Government Incentives for Domestic Recycling Capacity Boosting Supply of Recycled Fiber

- Competition From Flexible Plastic Pouches for Food Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solid Bleached Sulfate captured 38.41% of the United Kingdom folding carton market in 2025, thanks to its high whiteness and pharmaceutical-grade purity, which meet stringent regulatory and branding requirements. Coated Unbleached Kraft is on track for a 6.80% CAGR to 2031 as organic and craft food brands embrace its natural brown hue and food-contact compliance. The United Kingdom folding carton market benefits from brands seeking visible sustainability cues, and kraft substrates deliver that message without secondary labeling. In addition, lighter grammages enabled by FiberLight Tec technology in grades such as Performa Nova trim material inputs while maintaining box compression strength.

Consumer willingness to pay for premium, eco-friendly packaging is fueling trials of unbleached liners in frozen meals and chocolate assortments, although printability trade-offs still favor SBS for intricate graphics. Recycled White Line Chipboard remains a price fighter in household goods, yet limited stiffness bars it from premium shelves. Overall, Kraft's advance signals that visible fiber identity is now a marketing feature, not a defect, positioning unbleached grades to lift unit share within the UK folding carton market.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- Graphic Packaging International, LLC

- Mayr-Melnhof Karton AG

- Mondi plc

- International Paper Company

- Stora Enso Oyj

- Saica Group

- Coveris Holdings S.A.

- Qualvis Print & Packaging Ltd

- Glossop Cartons Ltd

- Curtis Print & Packaging Ltd

- The Alexir Partnership Ltd

- Benson Box Holdings Ltd

- Multi Packaging Solutions International Ltd

- Cepac Ltd

- BoxMart Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Phase-Out of Single-Use Plastics Under the UK Plastic Packaging Tax

- 4.2.2 E-Commerce Growth Fueling Demand for Lightweight Letterbox-Friendly Carton

- 4.2.3 Adoption of Digital Printing for Short Runs and SKU Proliferation

- 4.2.4 Brand Premiumization Raising Demand for High-Quality Graphic Carton

- 4.2.5 Investments in Recyclable Barrier Coatings Enabling Carton Replacement of Plastic Laminates

- 4.2.6 Government Incentives for Domestic Recycling Capacity Boosting Supply of Recycled Fiber

- 4.3 Market Restraints

- 4.3.1 Volatility in Virgin Pulp Prices Squeezing Converter Margins

- 4.3.2 Competition From Flexible Plastic Pouches for Food Products

- 4.3.3 Capacity Constraints in UK White-Fiber Recycling Infrastructure

- 4.3.4 Skill Shortages in Print and Converting Labor Limiting Scaling of Digital Carton Production

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-Commerce and Retail-Ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Graphic Packaging International, LLC

- 6.4.3 Mayr-Melnhof Karton AG

- 6.4.4 Mondi plc

- 6.4.5 International Paper Company

- 6.4.6 Stora Enso Oyj

- 6.4.7 Saica Group

- 6.4.8 Coveris Holdings S.A.

- 6.4.9 Qualvis Print & Packaging Ltd

- 6.4.10 Glossop Cartons Ltd

- 6.4.11 Curtis Print & Packaging Ltd

- 6.4.12 The Alexir Partnership Ltd

- 6.4.13 Benson Box Holdings Ltd

- 6.4.14 Multi Packaging Solutions International Ltd

- 6.4.15 Cepac Ltd

- 6.4.16 BoxMart Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment