PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063761

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063761

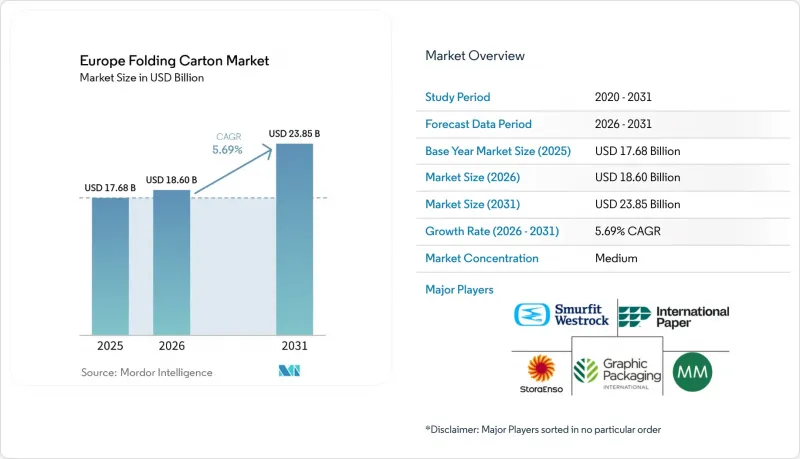

Europe Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the europe folding cartons market size is expected to be USD 17.68 billion in 2025, USD 18.60 billion in 2026, and reach USD 23.85 billion by 2031, growing at a CAGR of 5.69% from 2026 to 2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, Digital, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Folding Carton Market Trends and Insights

Accelerated Shift Toward Recyclable Packaging Among EU FMCG Brands

Major food and personal-care companies are moving faster than regulation to secure fiber supply and cost relief. Groupe Bel committed in 2025 to migrate all cheese-portion packs to folding cartons by 2027, removing 4,200 tonnes of plastic annually. Ferrero met its 2025 goal of sourcing only FSC-certified paperboard, while Mondelez switched to low-migration inks that stay recyclable in standard mills. Early adopters access certified fiber at baseline pricing, whereas late movers could face a 15-25% premium after 2028. National agencies oversee recyclability verification against Joint Research Centre protocols, giving first movers compliance certainty and smoother market access.

E-commerce Boom Driving Demand for Lightweight Protective Cartons

Online retail reached EUR 899 billion (USD 1.01 trillion) in 2025 and is reshaping the design of structures. Cartons between 250-350 gsm now dominate automated fulfillment centers because they reduce shipping weight by 12-18% while resisting crush during last-mile handling. DS Smith upgraded its Grenaa, Denmark, plant in March 2026 with a servo-driven rotary die-cutter that adds 15 million m2 of annual capacity, targeting robotics-compatible die-cuts for fashion and electronics shippers. Amazon and Zalando will require frustration-free, glue-free formats by 2027, accelerating uptake of self-locking structures that cut line changeovers and tape usage.

Volatile Hardwood Pulp Prices Compressing Converter Margins

NBSK pulp bounced between USD 950-1,180 per tonne in 2024-2025, while BEK ranged USD 720-920 per tonne, squeezing converters that operate on 8-12% EBITDA margins. Mayr-Melnhof noted that pulp inflation drove 60% of its COGS hike in 2025, with the pass-through delayed by 3 to 6 months. Smaller converters locked into annual price contracts struggle to recover costs and often accept margin erosion of 200-300 bps. Recycled grades offer only limited relief, as pharmaceutical and cosmetic cartons still require virgin-fiber SBS for migration-safety reasons.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Extended Producer Responsibility Fees Increasing Cost Pressure

- Adoption of High-Barrier Coatings Replacing Plastic Lamination

- Rising Energy Costs Undermining Small Converters' Profitability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solid Bleached Sulfate is projected to outgrow the European folding cartons market average at 6.69% CAGR, reflecting stringent migration limits for medicinal and luxury-cosmetic packs. The European folding cartons market for SBS benefits from Sappi Fusion TopScreen and Stora Enso PerformaBARRIER, both of which cleared CEPI's recyclability protocol in 2025, enabling barrier performance without plastic film. Folding Boxboard maintains the largest base, with 38.12% of the Europe folding cartons market share in 2025, favored for dry grocery and tobacco applications where moderate stiffness suffices.

Coated Unbleached Kraft expands in organic food lines that leverage its natural brown aesthetic, while White Line Chipboard competes in price-sensitive hardware and household goods. Mondi's 2025 buyout of Schumacher Packaging deepened its SBS portfolio and added six-color digital capability with white ink on brown substrates, letting cosmetics brands run short, seasonal promotions without litho plate costs. Virgin-fiber dominance persists in pharmaceutical serializations regulated under EU Directive 2011/62/EU, because print uniformity and emboss depth remain critical for anti-tamper integrity.

List of Companies Covered in this Report:

- Stora Enso Oyj

- Smurfit Westrock plc

- Mayr-Melnhof Karton AG

- Graphic Packaging Holding Company

- International Paper Company

- Mondi plc

- Huhtamaki Oyj

- Sonoco Products Company

- Metsa Board Corporation

- Essentra plc

- Rondo Ganahl AG

- BBP Packaging Ltd.

- Autajon Group

- GPA Global Ltd.

- AR Lithos Carton Ltd.

- Scatolificio del Garda SpA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Shift Toward Recyclable Packaging Among EU FMCG Brands

- 4.2.2 Mandatory Extended Producer Responsibility Fees Increasing Cost Pressure

- 4.2.3 E-commerce Boom Driving Demand for Lightweight Protective Cartons

- 4.2.4 Adoption of High-Barrier Coatings Replacing Plastic Lamination

- 4.2.5 Retailer Demand for Shelf-Ready Packaging Optimizing Logistics

- 4.2.6 AI-Enabled Color Management Systems Reducing Print Waste

- 4.3 Market Restraints

- 4.3.1 Volatile Hardwood Pulp Prices Compressing Converter Margins

- 4.3.2 Rising Energy Costs Undermining Small Converters' Profitability

- 4.3.3 Plastic Lobby Campaigns Delaying Certain Legislative Bans

- 4.3.4 Limited Recovery Infrastructure for Multimaterial Cartons

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Stora Enso Oyj

- 6.4.2 Smurfit Westrock plc

- 6.4.3 Mayr-Melnhof Karton AG

- 6.4.4 Graphic Packaging Holding Company

- 6.4.5 International Paper Company

- 6.4.6 Mondi plc

- 6.4.7 Huhtamaki Oyj

- 6.4.8 Sonoco Products Company

- 6.4.9 Metsa Board Corporation

- 6.4.10 Essentra plc

- 6.4.11 Rondo Ganahl AG

- 6.4.12 BBP Packaging Ltd.

- 6.4.13 Autajon Group

- 6.4.14 GPA Global Ltd.

- 6.4.15 AR Lithos Carton Ltd.

- 6.4.16 Scatolificio del Garda SpA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment