PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063762

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063762

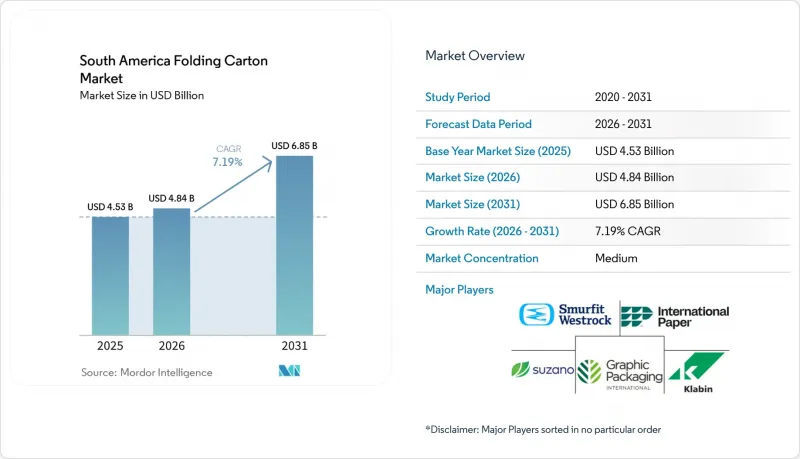

South America Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the south america folding cartons market size is expected to increase from USD 4.53 billion in 2025 to USD 4.84 billion in 2026 and reach USD 6.85 billion by 2031, growing at a CAGR of 7.19% over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, Digital, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

South America Folding Carton Market Trends and Insights

Accelerated Growth of Regional E-commerce Fulfillment Networks

Urban fulfillment hubs in Sao Paulo, Bogota, and Santiago are prompting brand owners to specify lighter, retail-ready cartons that minimize dimensional-weight charges and support next-day delivery. New sites such as Klabin's 240,000 tonnes-per-year Piracicaba II facility supply crash-bottom and straight-tuck styles optimized for automated pick-and-pack lines. Subscription commerce and direct-to-consumer launches demand graphics refreshes every few weeks, a requirement now met by digital presses that eliminate plate lead times. The sustained build-out of last-mile networks is expected to add 1.8 percentage points to the overall CAGR as converters lock in multi-year commitments with third-party logistics providers.

Brand Owner Shift Toward Monomaterial Recyclable Solutions

Multinationals, including Unilever, Danone, and Nestle, are redesigning South American SKUs around fiber-based monomaterials that align with global recyclability pledges. Klabin's Advance line, produced on Paper Machine 28, blends long pine and short eucalyptus fibers to deliver stiffness and premium print surfaces while remaining fully recyclable in curbside paper streams. Extended-producer-responsibility fees tied to multi-layer laminates further tilt economics toward folding cartons. This driver will lift market expansion by roughly 1.5 percentage points over the medium term as retailers increasingly favor on-shelf claims of 100% recyclable packaging.

Chronic Containerboard Supply-Demand Imbalance

Sharp demand spikes in 2025 left Argentine and Chilean converters scrambling for white-top kraftliner, driving spot prices up and elongating lead times. Although Klabin's new machines are easing tightness, specialty grades still face bottlenecks that erode converter margins and delay product launches. Short-term impacts shave 0.9 percentage points off growth until fresh capacity stabilizes regional inventories.

Other drivers and restraints analyzed in the detailed report include:

- Government-Led Plastics Reduction Mandates in MERCOSUR

- Rise in Near-sourcing of Consumer Goods to South America

- Currency Volatility Impact on Imported Pulp Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding boxboard captured 38.16% of the South America folding cartons market share in 2025, thanks to its versatility across cereals, snacks, and household cleaners. The grade's light basis weight keeps unit costs low and supports high-speed filling on legacy lines. Yet solid bleached sulfate is projected to grow at an 8.89% CAGR, contributing disproportionately to the South America folding cartons market as pharmaceutical and cosmetic brands specify brighter white surfaces and odor-neutral fibers.

Converters are repositioning portfolios accordingly. Klabin's Advance Print variant delivers tight color registration needed for over-the-counter drug cartons, while Advance Cup and Advance Tray grades target foodservice and thermoformable uses. Coated unbleached kraft remains the go-to for rugged packs that flaunt a natural aesthetic, and recycled-content chipboard protects margin in price-sensitive SKUs. As brand owners tighten supplier rosters, mills able to tailor fiber blends for regulatory compliance and luxury appeal will capture outsized share gains over the forecast horizon.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- International Paper Company

- Graphic Packaging Holding Company

- Klabin S.A.

- Suzano S.A.

- Papeles y Cartones de Europa S.A. (Saica)

- Mondi plc

- Rengo Co., Ltd.

- Cartones America S.A.

- Gerresheimer AG

- Tetra Laval International S.A.

- Visy Industries Holdings Pty Ltd

- Amcor plc

- AR Packaging Group AB (part of Graphic Packaging)

- Oji Holdings Corporation

- Orora Limited

- Stora Enso Oyj

- Cascades Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Growth of Regional E-commerce Fulfillment Networks

- 4.2.2 Brand Owner Shift Toward Monomaterial Recyclable Solutions

- 4.2.3 Government-Led Plastics Reduction Mandates in MERCOSUR

- 4.2.4 Rise in Near-sourcing of Consumer Goods to South America

- 4.2.5 Advances in Water-based Barrier Coatings for Food Contact

- 4.2.6 Private-Label Expansion in Modern Retail Channels

- 4.3 Market Restraints

- 4.3.1 Chronic Containerboard Supply-Demand Imbalance

- 4.3.2 Currency Volatility Impact on Imported Pulp Prices

- 4.3.3 Limited Skilled Labor for High-end Litho Printing

- 4.3.4 Slow Standardization of Recycling Infrastructure

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

- 5.4 By Country

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Chile

- 5.4.4 Colombia

- 5.4.5 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 International Paper Company

- 6.4.3 Graphic Packaging Holding Company

- 6.4.4 Klabin S.A.

- 6.4.5 Suzano S.A.

- 6.4.6 Papeles y Cartones de Europa S.A. (Saica)

- 6.4.7 Mondi plc

- 6.4.8 Rengo Co., Ltd.

- 6.4.9 Cartones America S.A.

- 6.4.10 Gerresheimer AG

- 6.4.11 Tetra Laval International S.A.

- 6.4.12 Visy Industries Holdings Pty Ltd

- 6.4.13 Amcor plc

- 6.4.14 AR Packaging Group AB (part of Graphic Packaging)

- 6.4.15 Oji Holdings Corporation

- 6.4.16 Orora Limited

- 6.4.17 Stora Enso Oyj

- 6.4.18 Cascades Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment