PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063779

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063779

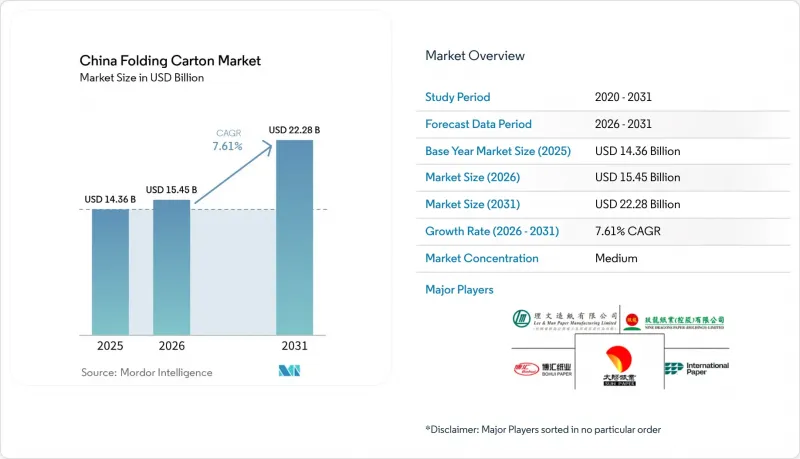

China Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the china folding carton market size is expected to be USD 14.36 billion in 2025, USD 15.45 billion in 2026, and reach USD 22.28 billion by 2031, growing at a CAGR of 7.61% from 2026 to 2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, Digital, Gravure, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More). The Market Forecasts are Provided in Terms of Value (USD).

China Folding Carton Market Trends and Insights

Growing Demand for Recyclable Fiber-Based Packaging

Parcel volumes surpassed 120 billion in 2025, and the express delivery packaging green transition plan now requires 95% of materials to be recyclable, steering shippers toward folding carton. Brands embrace Kraft aesthetics that cut ink coverage and simplify recycling, while integrated mills such as Nine Dragons expanded bleached boxboard capacity to 1.2 million t per year to secure a certified supply. Pilot reuse programs exist, yet hygiene and reverse-logistics hurdles keep single-use carton dominant.

E-Commerce Acceleration Driving Small-Run Carton Volumes

China's folding carton market orders placed through online channels reached an estimated 55% share in 2025, driven by flash sales and influencer-driven SKUs. Digital presses from HP Indigo and EFI enable profitable runs of 500 units with 97% PANTONE accuracy and embedded QR codes. Electronics brands in Shenzhen demand anti-static liners and custom die-cuts, pushing converters to invest in inline coating that integrates with digital workflows to achieve seven-day lead times.

Volatility in Pulp and Energy Prices

Softwood pulp fell 11.98% in 2025 to CNY 5,633 (USD 790) per tonne and is forecast to dip another 8.81% in 2026. Converters welcome cheaper inputs, but integrated mills such as Shandong Bohui financed sizable pulp expansions that now face compressed returns. Energy can represent 70% of drying costs in papermaking, and fluctuating natural gas tariffs in coastal provinces further destabilize margins

Other drivers and restraints analyzed in the detailed report include:

- Rising Premiumization in Cosmetics and Personal Care

- Government Plastic-Reduction Mandates Boosting Paperboard

- Competition from Flexible Plastic Packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding Boxboard captured 37.21% of the Chinese folding carton market share in 2025, supported by its smooth surface and consistent stiffness, which enable high-speed folder-gluers for snack, dairy, and pharmaceutical packaging. The segment benefits from integrated mills adding virgin fiber lines that ensure compliance with GB 4806 limits on heavy-metal migration. Coated Unbleached Kraft is forecast to outgrow the China folding carton market size at an 8.23% CAGR, propelled by organic food and craft beverage labels that showcase natural brown tones as an authenticity cue. Solid Bleached Sulfate remains the substrate of choice for prestige cosmetics where bright whiteness, embossability, and foil adhesion justify premium pricing, yet constrained hardwood pulp supply limits share gains. White Line Chipboard fills value tiers for detergents and dry goods, though its recycled content caps print fidelity and moisture resistance, limiting uptake in frozen and chilled foods.

Rising investor interest in virgin-fiber capacity is evident in Nine Dragons' Dongguan upgrade, which will replace two legacy machines with a 620,000 tonne-per-year kraft liner line, signaling a pivot toward food-safe grades. Specialty boards fortified with nanocellulose are emerging, with pilot trials documenting 15% weight reductions that can lower logistics costs for multichannel e-commerce distribution. Mills that embed in-house labs to verify GB 4806 compliance increasingly partner with global brand owners that demand transparent sourcing, giving scaled producers a margin edge over spot-market traders in the China folding carton market.

List of Companies Covered in this Report:

- Nine Dragons Paper Holdings Limited

- Lee & Man Paper Manufacturing Limited

- Shandong Sun Paper Industry Joint Stock Co., Ltd.

- Shandong Bohui Paper Industry Co., Ltd.

- International Paper Company

- Graphic Packaging International, LLC

- Huhtamaki Oyj

- Stora Enso Oyj

- Mayr-Melnhof Karton AG

- Mondi plc

- Rengo Co., Ltd.

- Oji Holdings Corporation

- Zhejiang Jingxing Paper Joint Stock Co., Ltd.

- Ningbo Zhonghua Paper Co., Ltd.

- Shanghai DE Printed Box

- Hangzhou Gerson Paper Co., Ltd.

- ITC Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Recyclable Fiber-Based Packaging

- 4.2.2 E-Commerce Acceleration Driving Small-Run Carton Volumes

- 4.2.3 Rising Premiumization in Cosmetics and Personal Care

- 4.2.4 Government Plastic-Reduction Mandates Boosting Paperboard

- 4.2.5 Automation Investments Lowering Conversion Costs

- 4.2.6 Digital Printing Adoption Enabling Mass Personalization

- 4.3 Market Restraints

- 4.3.1 Volatility in Pulp and Energy Prices

- 4.3.2 Competition from Flexible Plastic Packaging

- 4.3.3 Supply Gluts from Rapid Mill Capacity Expansions

- 4.3.4 Stringent Food-Contact Compliance Costs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-Commerce and Retail-Ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nine Dragons Paper Holdings Limited

- 6.4.2 Lee & Man Paper Manufacturing Limited

- 6.4.3 Shandong Sun Paper Industry Joint Stock Co., Ltd.

- 6.4.4 Shandong Bohui Paper Industry Co., Ltd.

- 6.4.5 International Paper Company

- 6.4.6 Graphic Packaging International, LLC

- 6.4.7 Huhtamaki Oyj

- 6.4.8 Stora Enso Oyj

- 6.4.9 Mayr-Melnhof Karton AG

- 6.4.10 Mondi plc

- 6.4.11 Rengo Co., Ltd.

- 6.4.12 Oji Holdings Corporation

- 6.4.13 Zhejiang Jingxing Paper Joint Stock Co., Ltd.

- 6.4.14 Ningbo Zhonghua Paper Co., Ltd.

- 6.4.15 Shanghai DE Printed Box

- 6.4.16 Hangzhou Gerson Paper Co., Ltd.

- 6.4.17 ITC Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment