PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063806

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063806

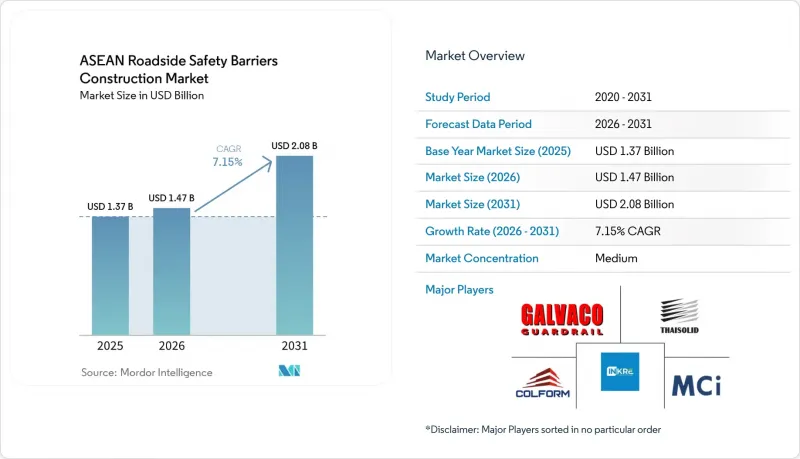

ASEAN Roadside Safety Barriers Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the aSEAN roadside safety barriers construction market size is projected to be USD 1.37 billion in 2025 and is estimated to be USD 1.47 billion in 2026, and expected to reach USD 2.08 billion by 2031, growing at a CAGR of 7.15% from 2026 to 2031.

This report is Segmented by Product Type (Metal Guardrails, Concrete Barriers, and More), by Material (Steel, and More), by Application (Highways & Expressways, Urban Roads & Streets, and More), by Installation Type (New Installation, Renovation/Retrofit/Repair), and by Geography (Indonesia, Vietnam, and More). Market Forecasts are Provided in Terms of Value (USD).

ASEAN Roadside Safety Barriers Construction Market Trends and Insights

Growing ASEAN highway connectivity and cross-border corridor upgrades are accelerating roadside safety barrier installation.

Multi-country corridors, such as the Greater Mekong Sub-region Highway and the India-Myanmar-Thailand Trilateral Highway, require harmonized safety hardware that surpasses outdated national minimum standards. Thailand's proposed Southern Economic Corridor, with an estimated value of THB 990 billion (USD 27.5 billion), is expected to add hundreds of kilometers of guardrails along landslide-prone coastal areas. Similarly, Vietnam's USD 3.2 billion Ha Tien-Rach Gia-Bac Lieu Expressway and Indonesia's Bogor-Serpong toll road will drive significant demand for W-beam and cable-barrier systems. As major corridors implement modern safety barriers, provincial agencies are under public pressure to retrofit adjacent feeder roads, thereby expanding the ASEAN roadside safety barriers construction market. Suppliers capable of meeting both AASHTO M180 and local certification standards are well-positioned to capitalize on this growing demand.

Regional road safety action plans are driving the adoption of median and edge protection systems.

ASEAN governments have allocated barrier spending in their 2026-2030 budgets as part of the United Nations Decade of Action for Road Safety. Projects such as Cambodia's National Road 4 upgrade and the Philippines' Maharlika Highway rehabilitation include guardrails as key deliverables linked to multilateral loan disbursements. Thailand's Toyota TRUST project uses data analytics to identify high-risk areas and implement rapid barrier installations, demonstrating how public-private collaboration enhances crash hotspot mitigation. These initiatives increasingly emphasize motorcycle-friendly barrier designs, creating a niche market for smooth-surfaced, low-beam products. This collective effort positions barrier procurement as a fundamental safety investment rather than an optional expense..

Budget constraints in lower-income ASEAN markets are delaying large-scale roadside safety upgrades.

Fiscal space has tightened following an 82% decline in international project finance to ASEAN, dropping to USD 17 billion in 2024. In the absence of concessional loans, provinces are compelled to make difficult decisions between maintaining fiscal guardrails and addressing urgent needs such as flood-control measures or school construction projects. The rise in steel prices to USD 515 per ton in 2026 has further reduced fixed-price tender margins, leading some fabricators to withdraw from bids and delaying projects to the next fiscal year. These deferred procurements result in kilometer-long backlogs, increasing crash exposure. While donor-co-financed road safety components address part of the issue, they only mitigate a small portion of the gap. As a result, near-term growth in the ASEAN roadside safety barriers construction market remains below potential, particularly in Cambodia and Myanmar.

Other drivers and restraints analyzed in the detailed report include:

- High accident exposure on intercity and mountainous roads is increasing the demand for crash barriers.

- Expansion of freight corridors and logistics routes is boosting the need for barriers on strategic highways.

- Uneven road safety enforcement across member countries is limiting consistent barrier adoption.

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal guardrails accounted for 51.3% of the ASEAN roadside safety barriers construction market share in 2025. W-beam rails are predominantly used on rural expressways, meeting Test Level-3 containment standards, while Thrie-beam profiles are preferred for freight corridors that accommodate heavier trucks. Cable barriers, although representing a smaller market share, are projected to grow at a CAGR of 7.98%, the fastest within the category. Agencies report up to a 90% reduction in fatal crashes on divided highways where cable barriers are implemented. In Malaysia, products like ArmorWire and Muar Cathay's Ezy-Guard series, both certified to MASH TL-3 standards, illustrate the increasing adoption of tensioned systems for narrow medians. Concrete Jersey and F-shape barriers maintain niche applications on bridges, toll plazas, and urban work zones, where permanent high-containment solutions are critical. Companies like WIKA Beton leverage their fourteen Indonesian plants to secure rapid-turnaround supply contracts in these areas.

Cable barriers also offer advantages in terms of easier and faster repairs after high-speed collisions, reducing lane-closure times by half compared to concrete alternatives. Crash cushions and impact attenuators occupy a premium segment, primarily used for protecting bridge piers and gore points. For instance, Safe Direction's TAU-M units in Singapore demonstrate a willingness to invest in controlled-deformation technology, particularly in areas with limited land availability. The "others" segment includes hybrid steel-concrete barriers and motorcycle-specific rails, where innovation is advancing faster than volume growth. Collectively, these trends indicate that the ASEAN roadside safety barriers construction market is diversifying beyond the traditional dominance of W-beam barriers over the forecast period.

In 2025, steel accounted for 67.8% of the total material demand in the ASEAN roadside safety barriers construction market. Locally produced coils from mills in Indonesia and Vietnam help maintain competitive pricing. Galvaco's integrated roll-form-plus-galvanizing line consistently exceeds AASHTO M180 coating standards, providing a 20-year corrosion resistance even in humid climates. High-strength grades like HR700F enable the use of thinner-gauge guardrails without compromising crash energy absorption, reducing freight costs on routes such as those in Sulawesi. Concrete ranks as the second most used material, primarily for parapets and medians on elevated expressways. Precast concrete units from Samwoh's Singapore plant have been specified for projects like the USD 387 million Changi viaduct, demonstrating their performance under seismic and typhoon conditions.

Composites, while currently holding a single-digit market share, are experiencing the fastest growth with a CAGR of 8.07%. Glass-fiber reinforced polyethylene rails from Boplan and GFRP-reinforced parapets, which are undergoing laboratory trials in Malaysia, offer advantages such as lighter weight and zero corrosion. These materials are particularly favored by toll operators for flood-prone areas where maintenance access is challenging. Recycled-plastic blends are also gaining traction, aligning with emerging circular-economy regulations in Thailand and Vietnam. Additionally, aluminum rails, though more expensive, are in demand for weight-restricted viaducts in the Mekong Delta. The diversification of materials positions suppliers with multi-substrate portfolios to outperform competitors relying on single-metal solutions as the ASEAN roadside safety barriers construction market continues to evolve.

List of Companies Covered in this Report:

- Galvaco Industries Sdn Bhd

- Thai Solid Co., Ltd.

- Colform Group Berhad (RoadMaster)

- PT Inter Nusa Kreasindo

- Muar Cathay Industries Sdn Bhd

- Siam Traffic Co., Ltd.

- DML Group of Company

- Pattarawit Traffic (Thailand) Co., Ltd.

- B Power Factory & Construction Co., Ltd.

- LeKise Co., Ltd.

- PT Wika Beton Tbk

- PT Pipa Baja Armco Indonesia

- Astro Holdings Sdn Bhd

- Samwoh Corporation Pte Ltd.

- Webforge Philippines Inc.

- Ingal Malaysia Sdn Bhd (Valmont)

- HuaAn Traffic Facilities Co., Ltd.

- Shandong Safebuild Traffic Facilities Co., Ltd.

- Safe Barriers Pty Ltd.

- DG Road Safety Pvt Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing ASEAN highway connectivity and cross-border corridor upgrades are accelerating the installation of roadside safety barriers

- 4.2.2 Regional road safety action plans are driving the adoption of median and edge protection systems

- 4.2.3 High accident exposure on intercity and mountainous roads is increasing the demand for crash barriers

- 4.2.4 Expansion of freight corridors and logistics routes is boosting the need for barriers on key strategic highways

- 4.2.5 Rising policy support for motorcycle-specific protection systems is encouraging targeted barrier deployment

- 4.3 Market Restraints

- 4.3.1 Uneven road safety enforcement across member countries is limiting consistent barrier adoption

- 4.3.2 Budget constraints in lower-income ASEAN markets are delaying large-scale roadside safety upgrades

- 4.3.3 Variations in standards and procurement practices are slowing the regional deployment of barrier systems

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Metal Guardrails (W-beam, Thrie-beam)

- 5.1.2 Concrete Barriers (Jersey, F-shape)

- 5.1.3 Cable Barrier Systems

- 5.1.4 Crash Cushions & Impact Attenuators

- 5.1.5 Others (Motorcyclist protection, hybrid, emerging)

- 5.2 By Material

- 5.2.1 Steel

- 5.2.2 Concrete

- 5.2.3 Plastic & Composite

- 5.2.4 Others (Aluminum, rubber, recycled blends)

- 5.3 By Application

- 5.3.1 Highways & Expressways

- 5.3.2 Urban Roads & Streets

- 5.3.3 Bridges & Flyovers

- 5.3.4 Others (Rural, industrial/private, parking, tunnels, temp zones)

- 5.4 By Installation Type

- 5.4.1 New Installation

- 5.4.2 Renovation / Retrofit / Repair

- 5.5 By Country

- 5.5.1 Indonesia

- 5.5.2 Vietnam

- 5.5.3 Thailand

- 5.5.4 Philippines

- 5.5.5 Malaysia

- 5.5.6 Singapore

- 5.5.7 Rest of ASEAN

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Galvaco Industries Sdn Bhd

- 6.4.2 Thai Solid Co., Ltd.

- 6.4.3 Colform Group Berhad (RoadMaster)

- 6.4.4 PT Inter Nusa Kreasindo

- 6.4.5 Muar Cathay Industries Sdn Bhd

- 6.4.6 Siam Traffic Co., Ltd.

- 6.4.7 DML Group of Company

- 6.4.8 Pattarawit Traffic (Thailand) Co., Ltd.

- 6.4.9 B Power Factory & Construction Co., Ltd.

- 6.4.10 LeKise Co., Ltd.

- 6.4.11 PT Wika Beton Tbk

- 6.4.12 PT Pipa Baja Armco Indonesia

- 6.4.13 Astro Holdings Sdn Bhd

- 6.4.14 Samwoh Corporation Pte Ltd.

- 6.4.15 Webforge Philippines Inc.

- 6.4.16 Ingal Malaysia Sdn Bhd (Valmont)

- 6.4.17 HuaAn Traffic Facilities Co., Ltd.

- 6.4.18 Shandong Safebuild Traffic Facilities Co., Ltd.

- 6.4.19 Safe Barriers Pty Ltd.

- 6.4.20 DG Road Safety Pvt Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment