PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063807

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2063807

North America Roadside Safety Barriers Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

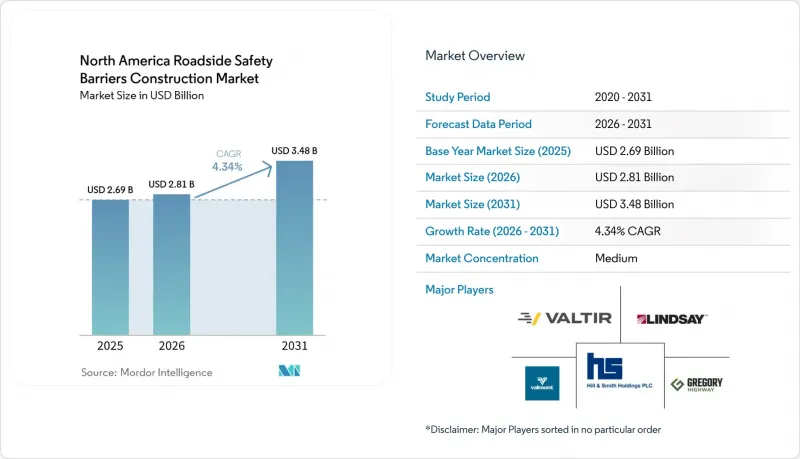

According to Mordor Intelligence, the north america roadside safety barriers construction market size is expected to increase from USD 2.69 billion in 2025 to USD 2.81 billion in 2026 and reach USD 3.48 billion by 2031, growing at a CAGR of 4.34% over 2026-2031.

This report is Segmented by Product Type (Metal Guardrails, Concrete Barriers, and More), by Material (Steel, and More), by Application (Highways & Expressways, Urban Roads & Streets, and More), by Installation Type (New Installation, Renovation/Retrofit/Repair), and by Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Roadside Safety Barriers Construction Market Trends and Insights

IIJA-Funded Highway Programs Accelerating Guardrail, Median Barrier, and Bridge Parapet Installations

Record federal expenditures serve as the primary driver for the North America roadside safety barriers construction market. The Highway Safety Improvement Program budget is set to increase to USD 3.49 billion in fiscal 2026, while the Bridge Formula Program contributes USD 5.5 billion annually, supporting projects that previously lacked state funding. Notable progress is evident in California, where a USD 33.2 million barrier upgrade on State Route 49 was completed in January 2026, and 28 miles of cable median barriers were installed on Interstate 80 in 2025. Pennsylvania's USD 259 million Interstate 80/Interstate 99 interchange project, primarily funded through Bipartisan Infrastructure Law formula grants, incorporates higher-containment MASH Test Level 4 systems, demonstrating how federal funding influences product standards. Similar funding allocations are directed toward Utah's US-6 and various Midwest corridors, ensuring sustained workloads for fabricators and installers over multiple years..

Mandatory MASH Compliance Deadlines Driving Large-Scale Replacement of Legacy Roadside Hardware

The transition from the National Cooperative Highway Research Program 350 standard to MASH 2016 is requiring Departments of Transportation (DOTs) to replace or retrofit hardware that no longer meets updated crash-test standards. The compliance deadline for most states is December 31, 2026, creating tighter project timelines. For instance, Caltrans has prohibited the use of legacy Type K portable barriers on projects advertised after this date. High-tension cable systems highlight the challenges of certification, as by late 2025, only one supplier had achieved full MASH 16 Test Level 4 approval for both flat ground and 4:1 slopes. Consequently, contractors are facing difficulties in securing compliant inventory, while rental fleets are retiring thousands of linear feet of outdated stock, driving near-term demand significantly above historical levels..

Lengthy State DOT Approvals and Certification Processes Delay Barrier System Deployment

Each new barrier model undergoes extensive evaluations, including crash tests, independent laboratory assessments, and state engineering reviews, which can take 12 to 18 months to complete. With individual states imposing additional specifications, manufacturers incur high costs for repeated testing and documentation, delaying market entry. The cable-barrier segment highlights these challenges: by 2025, only four approved suppliers were active in the market, each navigating distinct requirements for materials, splices, or post-spacing across various jurisdictions. Contractors securing bids before obtaining local product approval often face expensive delays, while Departments of Transportation (DOTs) experience budgetary backlogs as they wait for compliant hardware to become available.

Other drivers and restraints analyzed in the detailed report include:

- State DOT Safety Programs Prioritizing High-Crash Corridors Increasing Barrier Deployment Volumes

- Ongoing Interstate Rehabilitation and Widening Projects Expanding Median and Roadside Barrier Demand

- High Steel Prices and Installation Costs Increasing Total Project Budgets for Barrier Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metal guardrails accounted for 48.3% of the North America roadside safety barriers construction market share in 2025. These guardrails are predominantly used on rural highways where the right-of-way width is limited. However, cable systems are gaining traction rapidly. Cable systems, which provide a dynamic deflection of 6-8 feet, are projected to grow at a compound annual growth rate (CAGR) of 4.91% through 2031. For instance, Gibraltar installed 432,960 feet of cable in Alberta within 45 days, demonstrating the appeal of swift deployment for agencies managing increasing traffic volumes. Concrete, the second-largest product category, is primarily used for bridge parapets and urban medians where minimal deflection is essential. Crash cushions and attenuators, though niche products, are increasingly incorporating modular and reusable designs to reduce life-cycle costs.

The North America roadside safety barriers construction market for cable systems is expected to grow as Departments of Transportation (DOTs) replicate successful outcomes observed in states like Louisiana and Indiana. These states reported up to a 100% reduction in fatal crossover incidents following the installation of cable systems. Additionally, portable steel barriers, such as HighwayGuard(TM), are blurring the distinction between permanent and temporary products, further expanding the cable and hybrid category. Future growth could accelerate if more states align their specifications, facilitating large-scale production and faster MASH certification.

Steel accounted for 57.6% of the material market share in 2025, reinforcing its dominance in W-beam, Thrie-beam, and cable applications. However, composite and recycled-plastic alternatives, which are still in the early stages of adoption, are projected to grow at a compound annual growth rate (CAGR) of 5.10% through 2031, outpacing the overall market growth rate. Field trials indicate that fiber-reinforced polymer posts offer corrosion resistance and reduce routine maintenance costs. Additionally, an Internet-of-Things-enabled expanded polystyrene concrete hybrid, which is 30% lighter than standard concrete, provides real-time impact alerts to maintenance crews, reducing the need for frequent inspections.

Rising steel prices and zinc-galvanizing surcharges have shifted attention to total ownership costs. Research from UC Davis indicates that concrete barriers achieve cost parity with steel options after approximately 15 years when maintenance expenses are factored in. If composite systems can achieve cost competitiveness within a shorter timeframe, they may redefine industry specifications. Increasing patent activity, such as high-density polyethylene (HDPE) tube crash cushions with adjustable energy absorption, highlights ongoing research and development efforts that could drive a shift away from metal-based solutions over the forecast period.

List of Companies Covered in this Report:

- Valtir, LLC

- Valmont Industries

- Lindsay Corporation (Barrier Systems)

- Hill & Smith Inc.

- Gregory Highway (Gregory Industries)

- Nucor (Marion Steel/rail)

- Gibraltar Industries

- Road Systems Inc.

- TrafFix Devices Inc.

- RoadSafe Traffic Systems

- Hubbell Power Systems

- RS Technologies Inc.

- Barrier1 Systems

- Highway Baricades and Services, LLC.

- Highway Care USA

- San Bar Construction Corp.

- OSCO Safety

- Ramudden-Stinson

- Transpo Industries

- 48 Barriers

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Insights and Dynamics

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 IIJA-funded highway programs accelerating guardrail, median barrier, and bridge parapet installations

- 4.2.2 Mandatory MASH compliance deadlines driving large-scale replacement of legacy roadside hardware

- 4.2.3 State DOT safety programs prioritizing high-crash corridors increasing barrier deployment volumes

- 4.2.4 Ongoing interstate rehabilitation and widening projects expanding median and roadside barrier demand

- 4.2.5 Work-zone safety regulations across US and Canada sustaining temporary barrier usage in roadworks

- 4.3 Market Restraints

- 4.3.1 Lengthy state DOT approvals and certification processes delaying barrier system deployment

- 4.3.2 High steel prices and installation costs increasing total project budgets for barrier systems

- 4.3.3 Logistics and contractor capacity constraints slowing execution of large-scale replacement programs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Government Initiatives & Road Safety Programs

- 4.6 Regulatory Landscape

- 4.7 Technological Developments

- 4.8 Porter's Five Forces

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing Analysis

- 4.10 Supply-Demand Gap Analysis

- 4.10.1 Overview of Local Supply (Production and Key Players)

- 4.10.2 Overview of Market Demand (Projects and Usage)

- 4.10.3 Role of Imports in Meeting Demand

- 4.10.4 Overall Supply-Demand Gap Assessment

- 4.11 Key Projects & Infrastructure Pipeline

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Metal Guardrails (W-beam, Thrie-beam)

- 5.1.2 Concrete Barriers (Jersey, F-shape)

- 5.1.3 Cable Barrier Systems

- 5.1.4 Crash Cushions & Impact Attenuators

- 5.1.5 Others (Motorcyclist protection systems, hybrid/specialty barriers, emerging safety solutions)

- 5.2 By Material

- 5.2.1 Steel

- 5.2.2 Concrete

- 5.2.3 Plastic & Composite

- 5.2.4 Others (Aluminum, rubber-based materials, composite blends, recycled materials)

- 5.3 By Application

- 5.3.1 Highways & Expressways

- 5.3.2 Urban Roads & Streets

- 5.3.3 Bridges & Flyovers

- 5.3.4 Others (Rural roads, industrial/private roads, parking areas, tunnels, temporary traffic zones)

- 5.4 By Installation Type

- 5.4.1 New Installation

- 5.4.2 Renovation / Retrofit / Repair

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.3.1 Valtir, LLC

- 6.3.2 Valmont Industries

- 6.3.3 Lindsay Corporation (Barrier Systems)

- 6.3.4 Hill & Smith Inc.

- 6.3.5 Gregory Highway (Gregory Industries)

- 6.3.6 Nucor (Marion Steel/rail)

- 6.3.7 Gibraltar Industries

- 6.3.8 Road Systems Inc.

- 6.3.9 TrafFix Devices Inc.

- 6.3.10 RoadSafe Traffic Systems

- 6.3.11 Hubbell Power Systems

- 6.3.12 RS Technologies Inc.

- 6.3.13 Barrier1 Systems

- 6.3.14 Highway Baricades and Services, LLC.

- 6.3.15 Highway Care USA

- 6.3.16 San Bar Construction Corp.

- 6.3.17 OSCO Safety

- 6.3.18 Ramudden-Stinson

- 6.3.19 Transpo Industries

- 6.3.20 48 Barriers

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment