PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065731

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2065731

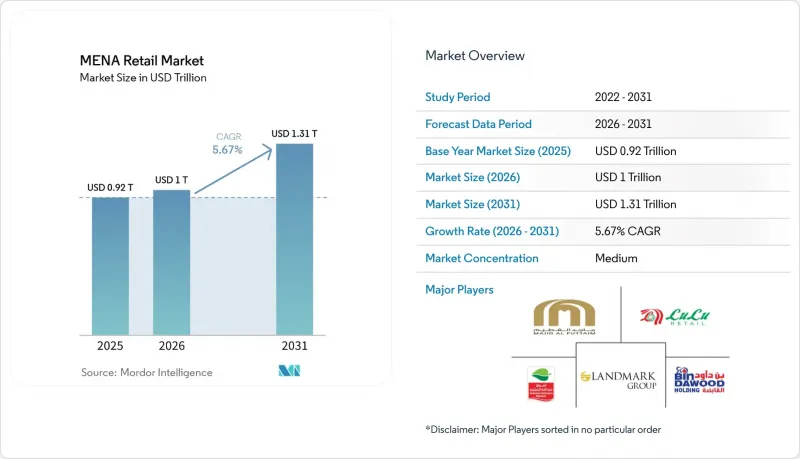

MENA Retail - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the mENA retail market size is projected to expand from USD 0.92 trillion in 2025 and USD 1 trillion in 2026 to USD 1.31 trillion by 2031, registering a CAGR of 5.67% between 2026 to 2031.

This report is Segmented by Product Category (Food & Grocery, Apparel; Beauty & Healthcare, Electronics, Home Care & Decor, and Toys & Leisure), by Store Type (Hypermarkets, Convenience, Specialty, Department, and More), by Channel (Offline, Brand E-Commerce, Marketplace, Social Commerce, and Quick Commerce), and by Geography (GCC, and North Africa). The Market Forecasts are Provided in Terms of Value (USD).

MENA Retail Market Trends and Insights

Organized Modern Trade Expansion

Organized trade expansion remains one of the clearest structural supports for the MENA retail market, because scale operators continue to gain from better sourcing, stronger compliance capacity, and broader format coverage. In Saudi Arabia, the food retail market exceeded USD 50 billion in 2024, and hypermarkets and supermarkets continued to strengthen their position as consumers shifted toward packaged food, larger assortments, and more dependable retail environments. The same report shows that major chains such as Panda, Othaim, Tamimi, BinDawood, LuLu, and Carrefour already operate extensive store networks, which gives them a wider base for expansion than smaller traditional outlets. Across the MENA retail market, this matters because modern trade is not only adding square footage but also raising standards in merchandising, inventory control, and supply consistency. That shift is improving the economics of branded retail, private label development, and fresh-food execution in the more formal parts of the region. It is also pushing the competitive center of gravity toward operators that can manage both store density and operating discipline across multiple urban clusters.

Omnichannel and E-commerce Acceleration

Omnichannel adoption is becoming a core growth lever for the MENA retail market, as digital commerce is no longer a side channel for only a few categories. LuLu Retail reported that its e-commerce sales grew 38.6% in FY2025. At the same time, half of its estate was e-commerce-enabled by year-end, indicating that large regional retailers are embedding online fulfillment within their physical networks rather than treating it as a separate business. Majid Al Futtaim reported 20% growth in e-commerce revenue and 38% growth in quick commerce in FY2025, indicating a similar pattern of digital acceleration within established retail platforms. In the MENA retail market, that combination is important because shoppers increasingly move between mobile discovery, store pickup, home delivery, and app-based replenishment within the same brand relationship. Omnichannel execution is therefore becoming less about adding a website and more about redesigning assortment, pricing, fulfillment, and loyalty around a blended shopping journey. Retailers that get this right are likely to defend their share more effectively as digital traffic keeps rising in the GCC and gradually deepens in North Africa.

Red Sea Logistics Shocks and Import Dependence

Logistics disruptions in and around Red Sea routes remain a significant restraint on the MENA retail market, as a large part of the region's retail assortment still depends on imported goods. The supplied draft notes that Asia-to-MENA transit times have been extended by 10 to 15 days during rerouting periods, putting pressure on working capital, replenishment timing, and seasonal merchandise planning. USDA also notes that Saudi Arabia relies on imports for up to 80% of its food consumption, which illustrates how exposed major regional retail systems remain to freight costs, trade frictions, and external supply volatility. In the MENA retail market, that exposure hits time-sensitive and lower-margin categories the hardest, especially fresh food, fashion, and electronics. Retailers with better local sourcing, stronger planning systems, or private label control are therefore in a better position to defend margins when shipping conditions tighten. The restraint is structural rather than temporary, because even short disruption periods can affect landed costs, inventory availability, and promotional timing across several retail categories at once.

Other drivers and restraints analyzed in the detailed report include:

- Youth-Led Premiumization and Discretionary Spend

- Ramadan and Religious-Tourism Demand Spikes

- Informal Trade and Uneven Last-Mile Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Food, Beverage, and Grocery accounted for 34.81% of the MENA retail market share in 2025, confirming that staples still anchor volume and traffic across the region. This leading position reflects the non-discretionary nature of food demand, the role of seasonal purchasing during Ramadan, and the continued spread of supermarkets and hypermarkets in both GCC and North African cities. In the MENA retail industry, grocery also benefits from repeat purchase frequency, which makes it the base category around which retailers build loyalty, cross-selling, and neighborhood relevance. Consumer Electronics and Household Appliances continue to hold a stable role in the MENA retail market, supported by housing expansion, household formation, and ongoing demand from expatriate populations in the Gulf. Apparel and Footwear also remain important because youth-heavy demographics, occasion-led spending, and mall traffic still support category turnover in major urban centers. Even when digital channels grow faster, grocery remains the category that most often links store visits, delivery demand, and basket-building behavior across the wider MENA retail market.

Beauty, Personal Care, and Healthcare is projected to grow at a 6.73% CAGR through 2031, the fastest pace among the MENA retail market's product categories. This reflects rising demand for wellness-linked spending, stronger female workforce participation, and a broader shift toward health, self-care, and convenience. Nahdi's 2024 annual report showed that private-label sales exceeded SAR 1.2 billion, online revenue grew 40%, and healthcare-related service activity expanded sharply, highlighting how healthcare retail is becoming a more integrated commercial platform rather than a narrow pharmacy format. In the MENA retail industry, that shift matters because it pulls spending into higher-value categories that combine products, advice, digital services, and repeat customer relationships. Home Care, Home Decor, and Furniture continue to benefit from residential development and urban household formation. At the same time, Toys, Hobbies, and Leisure Goods remain smaller but more relevant as family entertainment spending broadens. The less visible category shift is the growing role of retailer-controlled brands, as private label can improve margins and customer stickiness simultaneously.

List of Companies Covered in this Report:

- Majid Al Futtaim

- Alshaya Group

- Landmark Group

- LuLu Retail Holdings

- Al-Futtaim Retail

- Savola Group (Panda Retail Company)

- BinDawood Holding

- Abdullah Al Othaim Markets

- Cenomi Retail

- Jarir Marketing Company

- Nahdi Medical Company

- Spinneys

- Union Coop

- AZADEA Group

- Chalhoub Group

- Apparel Group

- Al Tayer Group

- Marjane Group

- BIM Maroc

- Kazyon

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Organized modern trade expansion

- 4.2.2 Omnichannel and e-commerce acceleration

- 4.2.3 Youth-led premiumization and discretionary spend

- 4.2.4 Ramadan and religious-tourism demand spikes

- 4.2.5 Offline BNPL and local-payment enablement

- 4.2.6 Rapid expansion of quick commerce platforms

- 4.3 Market Restraints

- 4.3.1 Red Sea logistics shocks and import dependence

- 4.3.2 Informal trade and uneven last-mile infrastructure

- 4.3.3 Belief-driven boycotts and localization costs

- 4.3.4 Retail margin pressure from discounting trends

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Consumer Behavior and Seasonal Demand Patterns

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Category

- 5.1.1 Food, Beverage, and Grocery

- 5.1.2 Apparel and Footwear

- 5.1.3 Beauty, Personal Care, and Healthcare

- 5.1.4 Consumer Electronics and Household Appliances

- 5.1.5 Home Care, Home Decor, and Furniture

- 5.1.6 Toys, Hobbies, and Leisure Goods

- 5.2 By Store Type

- 5.2.1 Hypermarkets and Supermarkets

- 5.2.2 Convenience Stores

- 5.2.3 Specialty Stores

- 5.2.4 Department Stores

- 5.2.5 Discount Stores and Cash-and-Carry

- 5.2.6 E-commerce and Online Retail

- 5.3 By Channel

- 5.3.1 Offline / Brick-and-Mortar

- 5.3.2 Brand-owned E-commerce

- 5.3.3 Marketplace-led E-commerce

- 5.3.4 Social Commerce

- 5.3.5 Quick Commerce

- 5.4 By Geography

- 5.4.1 GCC

- 5.4.1.1 Saudi Arabia

- 5.4.1.2 United Arab Emirates

- 5.4.1.3 Qatar

- 5.4.1.4 Kuwait

- 5.4.1.5 Oman

- 5.4.1.6 Bahrain

- 5.4.2 North Africa

- 5.4.1 GCC

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Majid Al Futtaim

- 6.4.2 Alshaya Group

- 6.4.3 Landmark Group

- 6.4.4 LuLu Retail Holdings

- 6.4.5 Al-Futtaim Retail

- 6.4.6 Savola Group (Panda Retail Company)

- 6.4.7 BinDawood Holding

- 6.4.8 Abdullah Al Othaim Markets

- 6.4.9 Cenomi Retail

- 6.4.10 Jarir Marketing Company

- 6.4.11 Nahdi Medical Company

- 6.4.12 Spinneys

- 6.4.13 Union Coop

- 6.4.14 AZADEA Group

- 6.4.15 Chalhoub Group

- 6.4.16 Apparel Group

- 6.4.17 Al Tayer Group

- 6.4.18 Marjane Group

- 6.4.19 BIM Maroc

- 6.4.20 Kazyon

7 Market Opportunities & Future Outlook

- 7.1 White-space and unmet-need assessment

- 7.2 Expansion of AI-driven personalized retail experiences

- 7.3 Growth of cross-border e-commerce and marketplace retail